B2B companies are worth 5 times more than B2C companies ($20.9 trillion, 70% of GDP globally), and typically with higher margins, more innovative, and faster growth … And yet often seen as the dull, industrial laggards of the business world … So who are the most inspiring B2B players, and how are they reinventing themselves?

B2B companies typically receive less attention than their B2C counterparts, but they possess distinctive “superpowers” that make them exceptionally well-positioned to lead innovation, sustainability, and business transformation.

One of their key strengths lies in the depth of their customer relationships. Unlike B2C companies that typically address large volumes of individual customers, B2B companies work closely with fewer, strategic clients, fostering long-term partnerships that enable co-creation and faster innovation cycles. This collaborative approach allows B2B companies to respond rapidly to evolving needs and develop tailored solutions that create significant value.

Additionally, B2B companies tend to have deep domain expertise in complex technologies or specialized industries, such as industrial automation, biotechnology, or finance. This knowledge enables them to solve critical business problems and become indispensable partners in their ecosystems.

Their position within extensive value chains gives them the power to drive sustainability improvements not only within their own operations but also upstream and downstream, influencing suppliers and customers alike.

B2B offerings are often highly customizable, providing the flexibility needed to adapt quickly to regulatory changes or shifting market demands. Financially, stable, long-term contracts provide predictable revenue streams that support bold investments in innovation and sustainability initiatives without the pressure of constant sales volatility.

Who are the most inspiring B2B companies?

So who are some of the most inspiring B2B companies today? Here are some of my favourites, who particularly showcase how innovation and sustainability are not separate agendas but deeply intertwined drivers of business growth and market leadership. From digital transformation and biotech breakthroughs to renewable energy and carbon removal, these B2B leaders are shaping a resilient, inclusive, and sustainable future on a global scale:

ABB is a global leader in electrification, robotics, and industrial automation, driving innovation in smart grids, electric vehicle infrastructure, and AI-powered solutions. The Swiss company prioritizes sustainability by aiming for carbon neutrality by 2030 and helps industries improve efficiency and reduce emissions. ABB’s digital platforms enable clients to optimise resource use and embrace Industry 4.0, positioning it as a key partner in building resilient, future-ready infrastructure worldwide.

ASML creates the photolithography systems that power the production of the world’s most advanced semiconductors. Its extreme ultraviolet (EUV) lithography machines are essential to creating the tiny, powerful chips that enable AI, cloud computing, and smart devices. Netherlands-based ASML is a future-ready industrial leader, combining nanotechnology, precision engineering, and data-driven manufacturing. It partners closely with customers like TSMC, Intel, and Samsung to push the limits of Moore’s Law.

Biontech is a pioneering biotech firm from Germany best known for developing one of the first effective mRNA COVID-19 vaccines. It focuses on immunotherapies for infectious diseases and cancer, using innovative genetic engineering and personalized medicine. Biontech embraces sustainability by advancing healthcare solutions that reduce treatment burdens and improve global health outcomes. Its agile research and development processes, combined with strategic partnerships, make it a leader in future-ready biotech innovation, accelerating drug discovery and delivery worldwide.

Climeworks develops direct air capture technology that removes CO2 from the atmosphere, addressing climate change at its source. The company’s innovative approach enables scalable carbon removal solutions, partnering with industries and governments to achieve net-zero goals. Swiss-based Climeworks focuses on sustainable impact by advancing carbon capture as a critical tool for climate mitigation. Its commitment to innovation and collaboration positions it at the forefront of the emerging carbon removal industry, helping to shape a cleaner, more sustainable future.

DBS Bank is a leading financial institution in Asia, renowned for its digital transformation and sustainability leadership. DBS integrates technology to enhance customer experience and operational efficiency while embedding ESG principles into its lending and investment decisions. The Singapore-based bank supports green finance, social impact initiatives, and innovation ecosystems, driving inclusive growth. With a forward-looking strategy, DBS is recognized for building resilience and agility in a dynamic financial landscape, enabling businesses and communities to thrive sustainably.

DSM is a global science-based company focused on health, nutrition, and sustainable living. It drives innovation by developing advanced materials, bio-based products, and nutritional solutions that improve human and animal health while reducing environmental impact. DSM integrates circular economy principles and carbon reduction targets into its operations and product development. With strong investments in biotechnology and renewable resources, DSM helps customers across food, pharmaceuticals, and industrial sectors innovate sustainably. Its commitment to purpose-driven innovation and collaboration positions DSM as a future-ready leader addressing global challenges like climate change, food security, and health.

e& (formerly Etisalat Group) is a multinational telecommunications conglomerate based in the UAE, driving digital transformation across the Middle East, Africa, and Asia. e& invests in 5G, cloud computing, AI, and IoT to empower enterprises and consumers with advanced connectivity and smart solutions. The company integrates sustainability by enhancing energy efficiency and promoting digital inclusion. With a strategic focus on innovation and regional development, e& supports economic growth and social progress, positioning itself as a future-ready digital leader in emerging markets.

Eli Lilly is a global pharmaceutical leader dedicated to discovering and delivering innovative medicines that improve patient outcomes. The company focuses on research and development in areas such as oncology, diabetes, immunology, and neuroscience. Eli Lilly embraces sustainability by reducing its environmental footprint and enhancing access to medicines worldwide. With a strong commitment to ethical practices and collaboration, it advances cutting-edge therapies through biotechnology and data-driven approaches. Eli Lilly’s focus on innovation, patient-centric solutions, and corporate responsibility positions it as a future-ready company driving health and societal progress globally.

FedEx is a global logistics and delivery powerhouse, innovating through advanced technology, automation, and sustainable fleet management. The company invests in electric vehicles, alternative fuels, and carbon-reduction programs to achieve carbon-neutral operations by 2040. FedEx uses data analytics and AI to optimize delivery routes, improve customer service, and reduce environmental impact. By integrating sustainability into its core business, FedEx is transforming logistics to be more efficient, resilient, and responsible, aligning growth with societal and environmental goals.

Hilti is a global leader in construction technology, renowned for its power tools, fastening systems, and digital jobsite solutions. Moving beyond products, Hilti delivers integrated services—tool fleet management, predictive maintenance, and on-site engineering—built around customer workflows. Its “tools-as-a-service” model transforms capex into opex, driving customer efficiency and loyalty. Hilti invests heavily in R&D and sustainability, aiming for circularity and carbon neutrality. With a strong focus on culture, learning, and inclusive leadership, Hilti exemplifies how industrial B2B companies can innovate through digitalization, service, and purpose, making construction safer, smarter, and more productive.

Holcim is a global leader in building materials, driving innovation in sustainable construction products and solutions. The company pioneers low-carbon cements, circular economy practices, and digital tools that reduce environmental impact while improving construction efficiency. Holcim’s commitment to decarbonization and resource efficiency supports global infrastructure development aligned with climate goals. Through R&D and strategic partnerships, Holcim is shaping the future of sustainable building, enabling customers to deliver greener, smarter, and more resilient projects worldwide.

Huawei is a major global provider of telecommunications equipment, consumer electronics, and cloud services. The company invests heavily in 5G, AI, and IoT technologies to enable smarter, more connected industries and cities. Huawei focuses on innovation-led growth while addressing sustainability through energy-efficient products and green manufacturing. Despite geopolitical challenges, Huawei continues to push digital transformation in Asia and beyond, empowering businesses with advanced infrastructure and digital capabilities to thrive in a rapidly evolving technological landscape.

Iberdrola is a Spanish multinational energy company and a global leader in renewable energy generation, particularly wind and hydroelectric power. Iberdrola invests heavily in clean energy infrastructure, smart grids, and energy storage technologies to accelerate decarbonization. Its sustainability agenda includes ambitious carbon neutrality targets and community engagement. Iberdrola’s innovation-driven approach combines advanced digital technologies with a commitment to social responsibility, making it a key player in the global energy transition and a model for future-ready utility companies.

Illumina leads the genomics revolution by developing advanced DNA sequencing technologies that accelerate medical research and personalized healthcare. Its innovations enable faster, cheaper, and more accurate genetic analysis, supporting breakthroughs in diagnostics and treatments. Illumina emphasizes sustainability by improving healthcare outcomes and reducing resource-intensive processes in labs. The company’s integration of cutting-edge technology with scalable platforms positions it as a future-ready biotech leader driving transformative impacts across healthcare and life sciences.

JPMorgan Chase is a global financial services leader, advancing innovation through technology, data analytics, and sustainable finance. The firm invests in fintech, blockchain, and AI to enhance customer experiences and operational efficiency. JPMorgan integrates ESG principles into its lending and investment strategies, supporting the transition to a low-carbon economy. The company’s commitment to diversity, inclusion, and community development complements its innovation efforts, enabling it to deliver long-term value for shareholders while addressing social and environmental challenges worldwide.

Lendlease is a global property and infrastructure group renowned for its focus on sustainable urban development. The company integrates environmental, social, and governance (ESG) principles into all aspects of its projects, emphasizing green building, community engagement, and resilient infrastructure. Lendlease leverages innovation and technology to create smart, sustainable cities that improve quality of life while minimizing environmental impact. Its commitment to net-zero carbon targets and circular economy practices positions Lendlease as a future-ready leader in real estate development and infrastructure, delivering long-term value to investors, communities, and stakeholders worldwide.

Microsoft is a technology giant shaping the future through cloud computing, AI, and enterprise software solutions. The company leads in sustainability with ambitious carbon reduction targets, aiming to be carbon negative by 2030. Microsoft’s platforms empower organizations to innovate, scale digital transformation, and improve operational sustainability. By embedding ethical AI and inclusive design, Microsoft promotes responsible innovation. Its ecosystem approach, global reach, and focus on societal impact make it a key driver of future-ready business across sectors.

Nvidia is a global leader in graphics processing units (GPUs) and AI computing. Its technologies power advancements in gaming, data centers, autonomous vehicles, and scientific research. Nvidia’s focus on AI acceleration drives innovation in industries ranging from healthcare to automotive. The company also prioritizes sustainability by improving energy efficiency in its products and data centers. Nvidia’s leadership in cutting-edge hardware and software solutions positions it at the core of the AI-driven digital transformation reshaping business and society.

NextEra Energy is the world’s largest producer of renewable energy from wind and solar. The company invests heavily in clean energy infrastructure and innovative grid technologies to accelerate the transition to a low-carbon economy. NextEra emphasizes sustainability through aggressive emissions reductions and integration of energy storage solutions. Its commitment to innovation and scale enables it to deliver reliable, affordable clean power while generating strong financial returns, positioning NextEra as a leading force in the global energy transformation.

Novozymes specializes in industrial enzymes and microbes that improve sustainability across agriculture, bioenergy, and food industries. By enabling more efficient processes and reducing waste, Novozymes drives circular economy solutions. The company invests in biotechnology innovation and partnerships to tackle global challenges such as climate change and food security. Novozymes’ focus on sustainable biology and scalable solutions positions it as a future-ready leader in industrial biotech, delivering both environmental and commercial value.

OpenAI is an AI research and deployment company committed to ensuring artificial general intelligence benefits all of humanity. OpenAI develops advanced machine learning models that drive innovation across industries including healthcare, education, and energy. The organization emphasizes ethical AI development and broad accessibility. By pioneering foundational AI technologies and collaborating with global partners, OpenAI shapes the future of intelligent systems, helping businesses and society harness AI responsibly for transformative impact.

Orsted is a global leader in offshore wind power and renewable energy solutions. The company transitioned from fossil fuels to focus almost entirely on green energy, driving decarbonization worldwide. Orsted invests in innovative wind farm technology, energy storage, and green hydrogen. Its sustainability strategy integrates environmental stewardship with community engagement. Through scale, technology, and strong governance, Orsted enables a just energy transition, delivering reliable clean power and setting benchmarks for corporate sustainability leadership.

Ping An is a leading Chinese financial services and technology conglomerate known for its digital innovation in insurance, banking, and asset management. Ping An leverages AI, big data, and blockchain to enhance customer experience and operational efficiency. The company integrates ESG principles into its business model, promoting financial inclusion and sustainable investments. With a strong focus on technology-driven transformation, Ping An is a future-ready leader advancing digital finance and social impact across Asia.

Pfizer is a global pharmaceutical leader known for innovative drug development and vaccine breakthroughs, including its COVID-19 vaccine. Pfizer invests heavily in R&D, biotechnology, and precision medicine to address unmet medical needs. The company promotes sustainability through responsible manufacturing, access initiatives, and climate action goals. Pfizer’s focus on scientific innovation and global health equity positions it to deliver transformative medicines and vaccines that improve lives while advancing corporate responsibility.

Schneider Electric is a global energy management and automation leader, enabling digital transformation for sustainability and efficiency. Its EcoStruxure platform integrates IoT, AI, and energy analytics to help clients decarbonize, electrify, and digitize buildings, factories, and infrastructure. Schneider’s solutions span power distribution, smart grids, and industrial automation. Committed to net-zero operations and helping partners reduce emissions, it is widely recognized for ESG leadership. With deep client partnerships, a robust ecosystem approach, and open innovation, Schneider Electric demonstrates how B2B companies can lead in technology, sustainability, and inclusive business transformation.

Shopify is a leading e-commerce platform enabling businesses worldwide to create online stores and scale digital sales. Shopify empowers merchants with tools for marketing, payments, and logistics while fostering innovation through APIs and apps. The company embraces sustainability by supporting small businesses, promoting carbon-neutral shipping, and investing in clean energy. Canada-based Shopify’s scalable platform and entrepreneurial ecosystem make it a future-ready enabler of digital commerce and economic inclusion.

Skanska is a global construction and development company prioritizing sustainable building practices and green infrastructure. Skanska integrates innovative construction technologies, circular economy principles, and energy-efficient designs to reduce environmental impact. The company collaborates with clients and communities to deliver safe, resilient projects that support climate goals. Skanska’s leadership in sustainable construction and digitalization positions it as a key player in building the low-carbon cities and infrastructure of tomorrow.

Stripe is a technology company that builds economic infrastructure for online payments and commerce. Its platform supports businesses of all sizes with seamless payment processing, fraud prevention, and financial tools. Stripe invests in sustainability through carbon-neutral initiatives and funding climate-focused startups. By simplifying complex financial operations, Stripe enables faster innovation and global commerce growth. Its commitment to developer-friendly solutions and sustainability makes it a future-ready leader in fintech.

Tetra Pak is a global leader in food processing and packaging solutions, known for its commitment to innovation, safety, and sustainability. The company pioneered aseptic packaging, enabling safe, long-life food without refrigeration—a breakthrough that revolutionized food distribution. Today, Tetra Pak is leading the way in sustainable packaging with plant-based materials, recyclable cartons, and circular economy initiatives. It integrates digital technologies such as smart packaging and connected supply chains to enhance traceability and efficiency. Partnering with food and beverage producers worldwide, Tetra Pak supports safer, more sustainable food systems, making it a future-ready player at the intersection of health, tech, and the environment.

Ubiquitous Energy develops transparent solar technology that integrates seamlessly into windows and surfaces, enabling buildings to generate clean energy without altering aesthetics. The company’s innovative photovoltaic solutions contribute to building decarbonization and energy efficiency. Ubiquitous Energy focuses on scalable, sustainable products that reduce reliance on fossil fuels and support green building standards. Its pioneering technology positions the company as a future-ready innovator in clean energy and sustainable architecture.

Vestas is a global leader in wind turbine manufacturing and renewable energy solutions. The company drives the clean energy transition by developing highly efficient, reliable wind technologies and service solutions. Vestas emphasizes sustainability throughout its supply chain and operations while investing in digitalization and predictive maintenance. Its global footprint and technology leadership make it a key player in achieving net-zero goals and expanding access to renewable power worldwide.

Waymo is a pioneer in autonomous vehicle technology, developing self-driving systems to transform mobility and transportation. The company leverages AI, machine learning, and sensor technology to improve safety, accessibility, and efficiency. Waymo’s innovations aim to reduce traffic emissions and congestion, contributing to smarter, more sustainable cities. Through strategic partnerships and pilot programs, Waymo is advancing the future of mobility and reshaping urban transportation ecosystems.

How are B2B reinventing themselves for the future?

Though less visible, B2B companies have unique superpowers—from deep customer intimacy and technical expertise to value chain influence and financial stability—that empower them to be fast, effective innovators and sustainability leaders. By embracing digital and sustainable transformation, reimagining business models, and sometimes going direct to end users, they can deliver superior shareholder returns and meaningful positive impact on society and the planet.

- Digitally Enabled Ecosystems: B2B companies have a unique opportunity to build and orchestrate powerful digital ecosystems. Leveraging AI, IoT, cloud platforms, and data integration, they can connect suppliers, customers, and partners in real time. This enables smarter supply chains, predictive maintenance, dynamic pricing, and embedded intelligence across products and services. Digital platforms not only drive efficiency but also open up new value streams and customer engagement models.

- Net Positive Business Models: Sustainability is no longer a compliance issue—it’s a business imperative. B2B firms are ideally positioned to lead in net positive strategies, designing circular systems, offering low-carbon products, and embedding ESG metrics into their value propositions. From regenerative materials to decarbonized logistics and sustainable infrastructure, they can create measurable environmental and social value while generating long-term economic returns.

- Service and Solution Innovation: The shift from product to service is revolutionizing B2B markets. Companies are moving to “outcome-as-a-service” models—such as uptime guarantees, energy efficiency contracts, or subscription-based equipment. This builds recurring revenue, deeper customer loyalty, and competitive advantage. Leaders like Hilti and Schneider Electric exemplify how bundling hardware, software, and service delivers integrated, higher-margin solutions.

- Deep Client Partnerships: B2B companies thrive on long-term relationships. The opportunity now lies in deepening these partnerships through co-innovation, tailored offerings, and integrated services. By embedding themselves in their clients’ operations and strategy, B2B firms can become indispensable problem solvers—advisors, not just vendors. This leads to greater resilience, trust, and joint value creation.

- Global and Niche Market Expansion: Rapid industrial growth in emerging markets, especially in Asia, Africa, and Latin America, creates enormous potential for B2B expansion. At the same time, specialized B2B firms can dominate niche markets with deep expertise and tailored solutions. Whether scaling globally or owning a category, the key is agile models that adapt to regional needs and opportunities.

- Industrial AI and Data Monetization: B2B companies sit on vast, underutilized data. With industrial AI, they can optimize operations, enhance product performance, and offer predictive insights as a value-added service. Leaders like GE and Honeywell are creating entirely new revenue streams by turning operational data into monetizable intelligence—shifting from machines to insights, from assets to outcomes.

- Leadership Transformation: To seize these opportunities, B2B leaders must evolve. Future-ready leadership demands agility, cross-disciplinary thinking, purpose-driven decision-making, and the ability to lead innovation and change. Building cultures of collaboration, entrepreneurship, and digital fluency is essential. Companies that invest in their people and foster empowered, diverse teams will be the ones shaping the future.

These capabilities enable B2B companies to deliver superior returns to shareholders while driving positive societal and environmental impact. By leading with innovation and sustainability, they command pricing power and customer loyalty, reduce risks associated with regulatory or environmental challenges, and create shared value that benefits multiple stakeholders.

Purpose-driven B2B firms also attract top talent and ESG-conscious investors, further accelerating growth and enhancing their reputation. In sum, B2B companies’ unique strengths—such as deep customer intimacy, technical expertise, value chain influence, and financial resilience—empower them to innovate quickly and effectively, reimagine business models, and lead the way toward a sustainable, future-ready economy.

Every industry is being reinvented.

A perfect storm of technological breakthroughs, shifting consumer expectations, environmental imperatives, and economic uncertainty is driving radical transformation across every sector. The boundaries between industries are blurring, value is migrating to new models and ecosystems, and the winners of tomorrow are being shaped today.

From automotive to insurance, banking to retail, energy to healthcare, established players face existential pressure to change. Legacy systems, slow-moving cultures, and risk-averse mindsets are being outpaced by fast, bold innovators—companies that use data, AI, and platform thinking to deliver better, smarter, more sustainable solutions. Tesla isn’t just a car company. Amazon isn’t just a retailer. They’re both operating systems for the future.

Disruptors are emerging from every corner of the globe—scaling faster, experimenting more aggressively, and harnessing the power of technology to solve meaningful problems.

These next generation leaders are obsessed with what’s next. They blend purpose and profit, long-term impact and short-term agility. But incumbents aren’t out of the race. The most forward-looking are reinventing themselves, acquiring new capabilities, and unlocking value from their intangible assets—brand, trust, ecosystems, and intelligence.

The next five years will be decisive. Growth will come not from doing more of the same, but from reimagining what’s possible—through smart automation, regenerative design, AI-powered personalization, and bold new business models. The winners will be those who stretch their vision, embrace uncertainty, and build for the future—not the past.

- The Reinvention Playbook: Lamborghini was a tractor company, Samsung was a grocery store

- Future Junkies: Why the best leaders are obsessed about what’s next

- What will they do next?: Anticipating the progress (and performance) of some of leading companies 2025 to 2030

- Music Reinvented: How an industry was reinvented through ecosystem thinking

- Reinventing Business with AI: the best of tech to radically reinvent organisations, and accelerategrowth

- The Net Positive Playbook. Allbirds to Climeworks, reinventing organisations for sustainable growth

- Pioneers and Transformers. Leading Airbus towards a better future, today and tomorrow

- The “Performer Transformer” Leader. Thriving in a world of relentless change

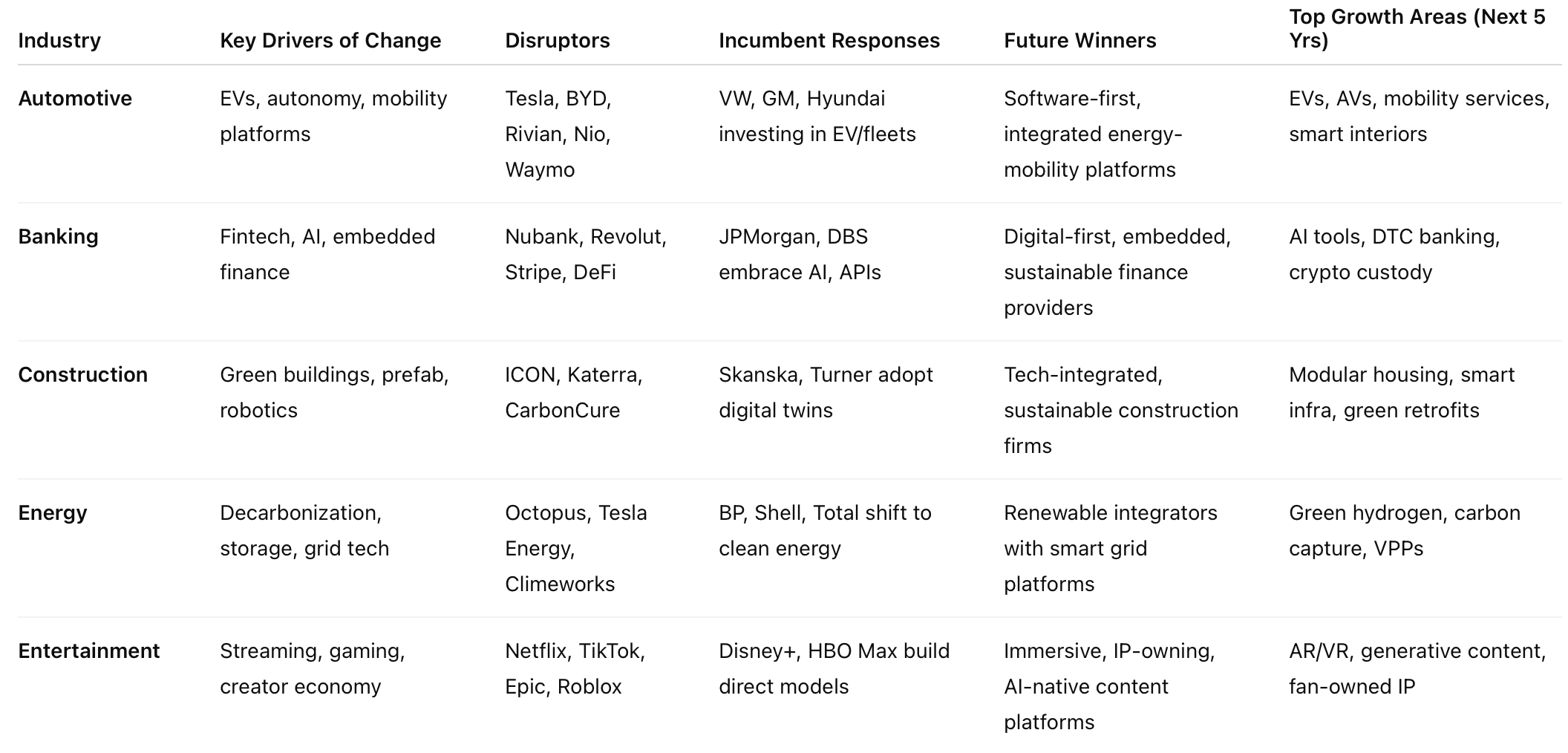

Automotive

When Lei Jun unveiled the SU7 electric supercar from his smartphone maker Xiaomi, with comparable features but over 90% cheaper than a Porsche Taycan, we knew the industry was not just being disrupted, but fundamentally reinvented. No longer just about horsepower and design, the future of cars became about software, autonomy, and energy ecosystems. Disruptors like Tesla, BYD, and Rivian are redefining mobility, while incumbents like GM and VW scramble to catch up. The future belongs to firms that can merge electric drivetrains with data-driven intelligence, build direct customer relationships, and plug into renewable grids.

- Key Drivers: EV revolution, autonomy, mobility-as-a-service

- Disruptors: Tesla, BYD, Rivian, Waymo, Nio, Xiaomi

- Incumbents: VW and Hyundai invest heavily in EVs and batteries; GM pivots toward all-electric by 2035

- Future Winners: Tesla remains dominant due to its integrated energy + mobility model; Chinese EV players like BYD are poised to lead on affordability and scale; Apple and Sony may emerge through software-first approaches

- Growth Areas: EVs, autonomous fleets, in-car software, subscription mobility

- Outlook: $5T transformation underway; platforms and ecosystems will define winners

Banking

In Brazil, David Vélez launched Nubank to free people from bureaucratic, fee-heavy traditional banks. With nothing more than a smartphone and a smile, customers signed up for accounts in minutes. Nubank now serves over 90 million users. Fintechs are rewriting the rules with embedded finance, AI risk models, and crypto rails. Traditional banks must become platforms, not fortresses. Future leaders will be those who turn trust, data, and user experience into intelligent financial ecosystems.

- Key Drivers: Fintech, AI, blockchain, real-time services

- Disruptors: Nubank, Revolut, Stripe, Square, DeFi

- Incumbents: JPMorgan and DBS investing in AI, APIs, and sustainability-linked finance

- Future Winners: Digital-first, customer-centric, embedded finance providers that turn financial services into frictionless tools

- Growth Areas: AI-enabled wealth tools, crypto custody, sustainable lending

- Outlook: Banking becomes invisible, embedded in lifestyle

Construction

Using 3D printing, Icon built a house in 24 hours using a giant robotic arm and a special concrete blend—radically reducing time, cost, and environmental impact. This illustrates the kind of breakthrough needed in a notoriously slow-moving industry. Innovation now means modular, smart, and zero-carbon construction. Giants like Skanska are investing in digital twins and low-carbon cement. Winners will combine automation, green design, and tech-savvy talent to transform how we build the future.

- Key Drivers: Green buildings, modular methods, robotics

- Disruptors: Icon (3D printing), Katerra (prefab), CarbonCure (CO2 tech)

- Incumbents: Skanska, Bouygues, Holcim, and Turner adopting digital twins and zero-carbon materials

- Future Winners: Tech-integrated construction firms that deliver faster, cleaner, cheaper buildings; smart infrastructure providers

- Growth Areas: Smart cities, digital twins, sustainable housing

- Outlook: $1T green retrofit and smart build opportunity

Energy

Octopus Energy is disrupting utilities by putting customers at the heart of a clean energy revolution—offering dynamic pricing, transparency, and rapid green energy switching. In an industry long dominated by giant incumbents, it proved agility can win. The transition to net zero, powered by solar, wind, hydrogen, and AI-managed grids, is accelerating. Winners will not just produce energy, but orchestrate energy flows, storage, and demand across intelligent, decentralised networks.

- Key Drivers: Decarbonization, decentralization, storage

- Disruptors: Tesla Energy, Octopus Energy, Vestas, Climeworks

- Incumbents: Shell, TotalEnergies, and BP redefining themselves as energy transition companies

- Future Winners: Companies that integrate solar, wind, storage, and smart grids into unified platforms

- Growth Areas: Renewables, green hydrogen, carbon capture, virtual power plants

- Outlook: Clean energy to dominate mix by 2030; trillion-dollar opportunity

Entertainment

When Roblox went public, it revealed that kids were spending more time building and playing in virtual worlds than watching TV. Entertainment is no longer passive—it’s immersive, participatory, and social. New models powered by creators, fans, and algorithms are dominating, as traditional studios play catch-up. Netflix disrupted distribution; now AI and generative content are the new frontiers. Winners will build platforms that blend content, community, and co-creation.

- Key Drivers: Streaming, gaming, AI content, creator economy

- Disruptors: Netflix, Epic Games, Roblox, TikTok

- Incumbents: Disney+ reinvention; Warner Bros. bets on streaming + IP

- Future Winners: Firms that merge entertainment, social engagement, and immersive tech; those who own IP and fan relationships

- Growth Areas: AI-generated content, gamified storytelling, AR/VR

- Outlook: Creator platforms to become dominant media forces

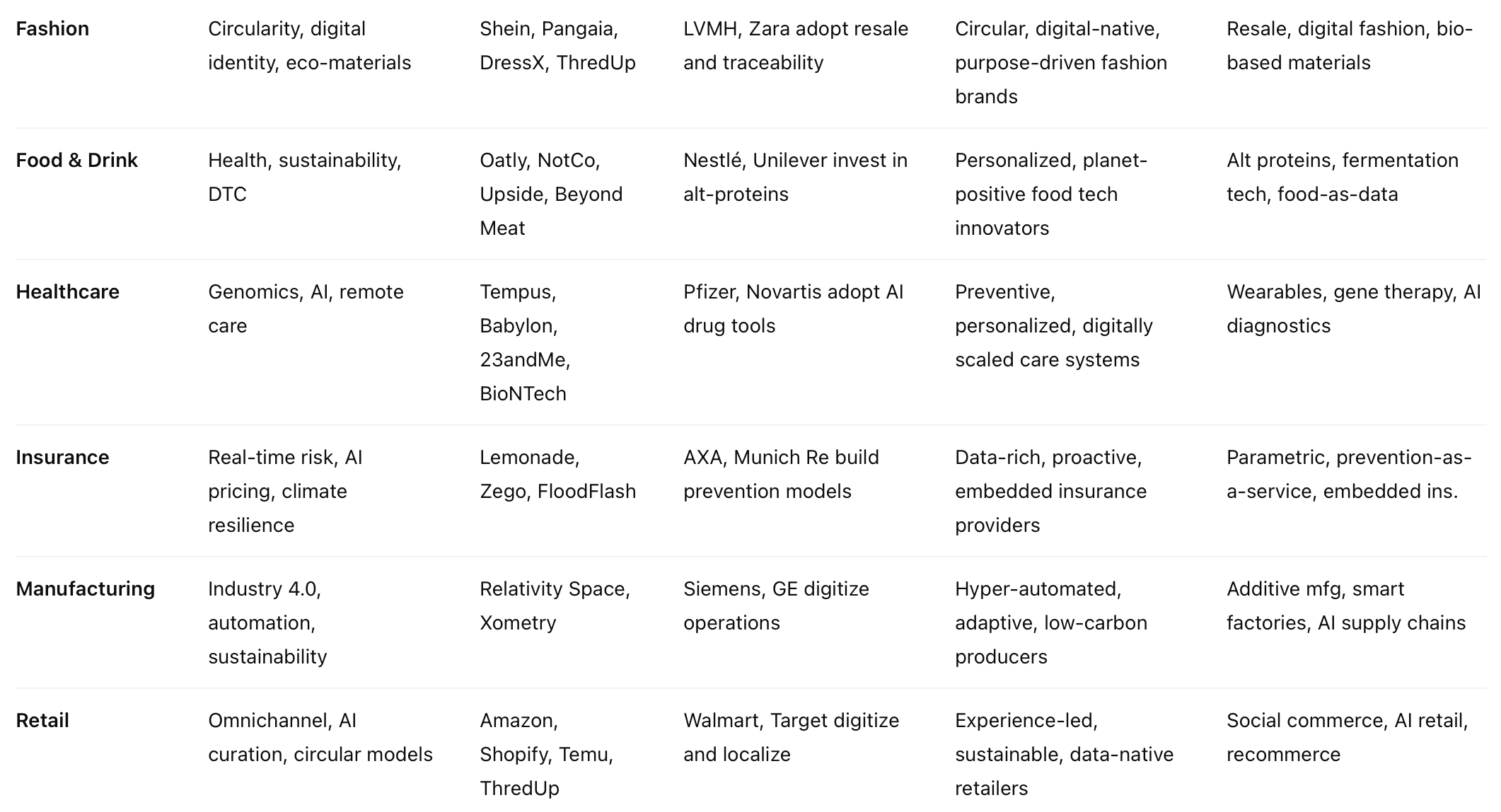

Fashion

Pangaia isn’t just a fashion brand—it’s a material science company using seaweed fibers and bacteria-based dyes to reinvent sustainable clothing. Fashion is being reshaped by digital identities, circular design, and transparent supply chains. Fast fashion disruptors like Shein use real-time data and micro-inventory, while luxury players are experimenting with resale and digital fashion. Future winners will merge purpose with personalization, creating garments that are smart, sustainable, and story-driven.

- Key Drivers: Sustainability, digital fashion, circularity

- Disruptors: Shein, ThredUp, Pangaia, DressX

- Incumbents: LVMH and Zara building closed-loop supply chains and digital experiences

- Future Winners: Brands that mix identity, impact, and innovation; digital-native and circular-first businesses

- Growth Areas: Resale, AI design, bio-materials, virtual clothing

- Outlook: Fashion shifts from volume to value, driven by tech + conscience

Food and Drink

At NotCo, AI named Giuseppe creates plant-based versions of animal products by analyzing molecular similarities. It made mayo, milk, and meat that taste like the real thing—but aren’t. This signals a shift toward food as software: designed, personalized, and planetary. The food revolution is being driven by sustainability, health, and technology. Giants like Nestlé are investing in alt-proteins. Winners will feed the future with science, values, and delicious innovation.

- Key Drivers: Health, sustainability, transparency

- Disruptors: Beyond Meat, Oatly, NotCo, Upside Foods

- Incumbents: Nestlé and Unilever invest in plant-based and direct-to-consumer (DTC) platforms

- Future Winners: Brands that align with planetary and personal health; those who digitize the food chain

- Growth Areas: Alt protein, fermentation tech, personalized nutrition

- Outlook: $300B alt-protein industry by 2030; data becomes the key ingredient

Healthcare

During the COVID-19 pandemic, BioNTech—once a little-known biotech firm—partnered with Pfizer to deliver a vaccine in record time using mRNA technology. It was a moonshot moment. Healthcare is being reinvented through genomics, AI, and patient-centric platforms. Startups like Tempus and Babylon offer predictive care and digital diagnoses, while incumbents digitize clinical pathways. Future leaders will move from treating illness to preventing it—personalized, predictive, and precision-driven.

- Key Drivers: AI, genomics, personalized medicine

- Disruptors: Tempus, BioNTech, 23andMe, Babylon Health

- Incumbents: Pfizer, Novartis and Roche embed AI across drug discovery and diagnostics

- Future Winners: Companies delivering preventive, digital, and personalized care at scale

- Growth Areas: AI drug discovery, wearable diagnostics, gene therapies

- Outlook: From reactive to proactive care; multi-trillion-dollar ecosystem

Insurance

Lemonade turned heads by settling some claims in under 3 seconds, using AI and behavioral economics. It proved insurance doesn’t have to be slow, opaque, or distrusted. Climate volatility and shifting lifestyles demand real-time, proactive coverage. Incumbents like Munich Re are adapting with prevention-as-a-service. The winners will anticipate, not just insure—embedding risk reduction, AI insights, and customer trust into everything.

- Key Drivers: Risk prevention, personalization, AI pricing

- Disruptors: Lemonade, Zego, FloodFlash, Trōv

- Incumbents: AXA and Munich Re building smart risk platforms and climate resilience tools

- Future Winners: Insurers who evolve into risk-reduction partners powered by real-time data

- Growth Areas: Parametric insurance, embedded models, prevention-as-a-service

- Outlook: Reinvention from safety net to proactive value provider

Manufacturing

Relativity Space is using 3D printing to make rockets—95% fewer parts, far faster iterations. It’s a symbol of manufacturing’s new age: flexible, intelligent, and software-defined. Automation, IoT, and AI are transforming everything from design to delivery. Legacy players like Siemens and GE are embracing digital twins. The factories of the future will be smart, sustainable, and continuously learning.

- Key Drivers: Industry 4.0, robotics, sustainability

- Disruptors: Relativity Space, Xometry, Vention

- Incumbents: Siemens, GE, and Bosch digitizing supply chains and factory floors

- Future Winners: Agile, hyper-automated, sustainable manufacturers with digital cores

- Growth Areas: Smart factories, additive manufacturing, nearshoring

- Outlook: $1T+ productivity gains from intelligent manufacturing

Retail

Shopify gave small businesses global reach with a few clicks—and now powers millions of storefronts. Retail is shifting from stores to ecosystems, driven by social commerce, AI curation, and instant fulfillment. Amazon, Temu, and ThredUp are reshaping expectations. Incumbents must combine digital agility with deep human insight. The next winners will create seamless, personalized, and values-based retail experiences.

- Key Drivers: Omnichannel, AI personalization, circularity

- Disruptors: Amazon, Shopify, Temu, ThredUp

- Incumbents: Walmart and Target investing in AI, last-mile, experiential retail

- Future Winners: Ecosystem retailers blending physical, digital, and sustainable offerings

- Growth Areas: Social commerce, live shopping, AI recommendation engines

- Outlook: Retail = technology; brand trust + data + delivery = competitive edge

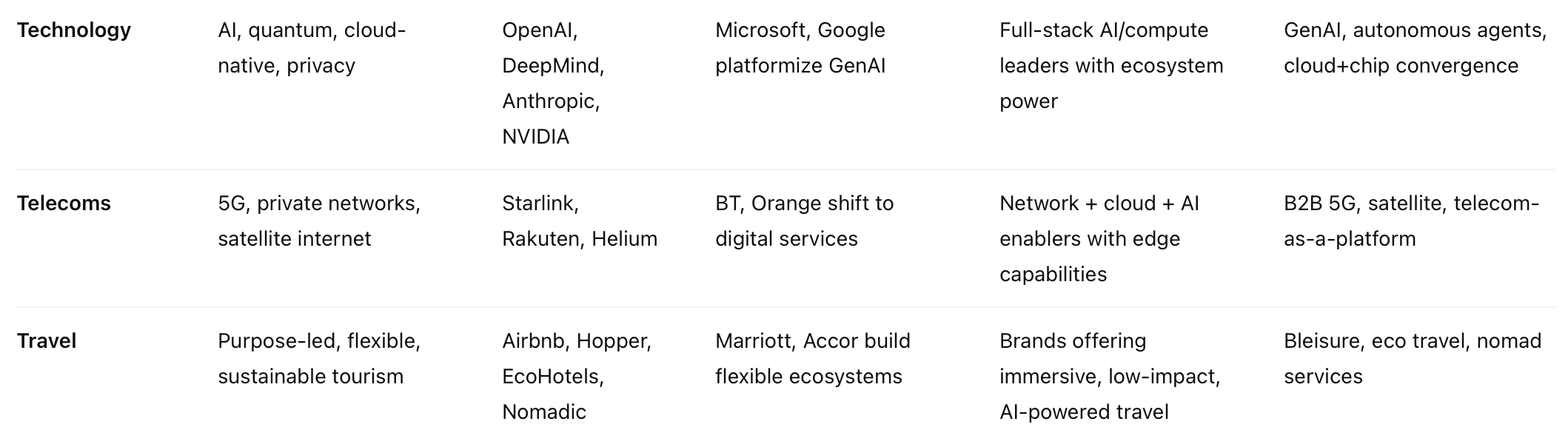

Technology

When OpenAI released ChatGPT, it stunned the world—and ignited an AI arms race. Technology is the force multiplier of every transformation. AI, quantum, chips, and decentralised platforms are reshaping what’s possible. Disruptors like DeepMind and Anthropic push the frontiers, while incumbents like Microsoft integrate AI into everything. The winners will be ecosystem architects, building the foundations of a superintelligent, secure, and inclusive digital world.

- Key Drivers: AI, cloud, quantum, cybersecurity

- Disruptors: OpenAI, DeepMind, Anthropic, Nvidia

- Incumbents: Microsoft and Google integrating GenAI across platforms

- Future Winners: Platform-native firms owning data, chips, and AI layers

- Growth Areas: GenAI, autonomous agents, AI operating systems

- Outlook: Tech drives all other industries; $10T+ value shift imminent

Telecoms

Starlink launched satellites fast enough to beam high-speed internet to war zones and remote villages alike. It showed how agile, hardware-software integrated telecom can leapfrog legacy infrastructure. With 5G, edge computing, and AI, telecom is evolving into a platform for everything—especially B2B. The leaders will connect not just people, but machines, data, and intelligence.

- Key Drivers: 5G, private networks, AI-managed ops

- Disruptors: Starlink, Rakuten Mobile, Helium Network

- Incumbents: AT&T, BT, and Orange reposition as digital service providers

- Future Winners: Providers offering integrated connectivity, intelligence, and cloud-edge infrastructure

- Growth Areas: Satellite internet, B2B 5G, telecom-as-a-platform

- Outlook: Telcos reinvent as enablers of digital society

Travel

Airbnb changed not just where we stay—but how we experience the world. It made travel more local, personal, and flexible. Now, the rise of conscious travelers, nomadic workers, and immersive tech is redefining journeys. EcoHotels and digital nomad platforms are growing fast. Future winners will offer sustainable, seamless, and soul-nourishing travel—with data-driven personalisation and low-impact design.

- Key Drivers: Sustainable tourism, remote work, personalization

- Disruptors: Airbnb, Boom, Hopper, Nomadic, EcoHotels

- Incumbents: Marriott and Accor push eco-design, digital concierge, loyalty platforms

- Future Winners: Brands offering flexible, immersive, low-impact experiences

- Growth Areas: Bleisure (business + leisure), digital nomad services, green destinations

- Outlook: Travel reimagined around purpose, data, and experience.

Winners and losers

Of all the industries listed, technology, energy, and healthcare are likely to be transformed the most dramatically and the fastest in the next five years. However, the strategic stakes are high across all industries — and the value impact of getting it right vs wrong can mean survival vs extinction, or exponential growth vs stagnation.

Technology is the enabler of disruption across every other sector. Its pace is exponential due to AI, quantum computing, chips, and software-defined everything. Winners will become AI-native platforms, building ecosystems not just products. Losers will underestimate AI’s impact or failing to adapt legacy business models. Companies that win, like Microsoft and Nvidia, are adding hundreds of billions in market cap. Losers risk obsolescence in 3–5 years.

In energy – accelerating due to climate pressure, policy shifts, and clean tech investment – the transition from fossil fuels to renewables is reshaping everything from national security to consumer choices. Winners will be joining the shift to decentralised, customer-centric energy platforms, like Octopus Energy. Losers cling to fossil-heavy models or slow-moving asset bases. This is a $100+ trillion transition opportunity globally, where winners gain access to premium markets and long-term capital.

And in healthcare – changing rapidly due to genomics, AI diagnostics, digital therapeutics, and aging populations – the reinvention is black and white: from reactive to predictive, from generic to personalised. Winners will invest in AI, data infrastructure, and consumer-led models. Losers fail to reinvent legacy systems or ignoring preventive platforms. Personalized medicine and digital health could unlock over $3 trillion in new value globally.

Time to reinvent everything

Across every industry, reinvention is no longer optional—it’s the new normal.

Forces such as AI, climate imperatives, digital-native consumers, and global competition are disrupting traditional business models and reshaping value chains. From energy to entertainment, food to finance, every sector is being redefined by new technologies, agile entrants, and escalating stakeholder expectations. The next five years will see more industry change than the last 50 years.

Future winners won’t simply digitize what they’ve always done. They will reimagine what’s possible. They will move faster, scale smarter, and act bolder—blending innovation, purpose, and resilience into every part of their business. They will be led by visionaries who see around corners and build adaptive, AI-powered organizations that learn and evolve in real-time.

The playbook for future winners includes:

-

Adopt a platform mindset: Build ecosystems, not empires. Share data, integrate services, and create value with partners.

-

Embed intelligence everywhere: Use AI to automate, personalize, and optimize—from supply chains to customer journeys.

-

Design for impact: Prioritize sustainability, health, and wellbeing. Turn climate and social challenges into innovation opportunities.

-

Act with agility: Use modular structures, empowered teams, and rapid iteration to adapt at speed.

-

Monetize intangibles: Build brands, trust, data, and communities—not just products.

-

Think globally, execute locally: Scale ideas fast, but tailor them to people and places with cultural insight.

The companies that win will create not just better businesses, but better futures—where growth and good are inseparable. The race is on to lead, to learn, and to leap.

Explore more, with Peter Fisk:

- The Reinvention Playbook: Lamborghini was a tractor company, Samsung was a grocery store

- Future Junkies: Why the best leaders are obsessed about what’s next

- What will they do next?: Anticipating the progress (and performance) of some of leading companies 2025 to 2030

- Music Reinvented: How an industry was reinvented through ecosystem thinking

- Reinventing Business with AI: the best of tech to radically reinvent organisations, and accelerategrowth

- The Net Positive Playbook. Allbirds to Climeworks, reinventing organisations for sustainable growth

- Pioneers and Transformers. Leading Airbus towards a better future, today and tomorrow

- The “Performer Transformer” Leader. Thriving in a world of relentless change

In a fast-changing global economy, the ability to grow, adapt, and innovate is no longer optional—it’s existential. Yet how companies pursue growth and innovation varies dramatically around the world. The business mindsets that shape these efforts are deeply rooted in regional histories, cultures, economies, and institutions.

Nowhere is this contrast more evident than between the three major economic blocs: America, Europe, and Asia. Each has developed a distinct approach to growth and innovation—reflecting differing attitudes toward risk, regulation, competition, social responsibility, and the role of the state. Understanding these differences is crucial for any global business leader looking to scale ideas or navigate new markets.

America … Bold, Fast, and Founder-Driven

America has long been the epicenter of disruptive innovation. From Silicon Valley tech giants to biotech startups in Boston and clean energy hubs in Texas, the US ecosystem rewards ambition, speed, and scale.

At the heart of the American mindset is the cult of the entrepreneur. Founders are celebrated as visionaries and risk-takers. Venture capital flows freely to big ideas with even bigger potential returns. The prevailing ethos is: “Move fast and break things”—a willingness to experiment, fail, and iterate quickly. Companies like Tesla, Amazon, and OpenAIexemplify this mindset—prioritising first-mover advantage, hypergrowth, and massive bets on the future.

This drive is underpinned by a strong private sector, deep capital markets, and a relatively light-touch regulatory environment. In many industries, competition is fierce but welcomed. Success is measured in market capture, valuation, and growth curves, often at the expense of short-term profit or social consensus.

In this environment, innovation is often radical and high-risk. Startups aim to “disrupt” incumbents. Companies pivot rapidly. Failures are seen as a rite of passage. And platforms, not products, increasingly dominate—designed to scale globally from day one.

But the American model is not without drawbacks. Its focus on speed and dominance can lead to backlash—regulatory (as with Big Tech), social (as with gig economy labor practices), or ethical (as seen in AI and data privacy concerns). Its innovation engine is powerful but often individualistic and capital-centric, sometimes prioritising shareholder returns over broader social value.

Europe … Cautious, Collaborative, and Responsible

Europe takes a different approach. Its innovation mindset is shaped by stability, regulation, inclusivity, and sustainability. European companies often innovate incrementally rather than disruptively, and growth is usually slower but more deliberate and long-term.

Many European business cultures value consensus, quality, and risk management. Innovation is typically tied to social goals, such as environmental responsibility, worker rights, and long-term societal benefit. This is evident in the European Union’s push for the Green Deal, data sovereignty rules like GDPR, and a wave of regulation around AI and digital markets.

Rather than creating monopolistic platforms, Europe tends to foster ecosystems of collaboration—between companies, governments, universities, and civil society. Companies like Siemens, Schneider Electric, Novo Nordisk, and Vestasinnovate in deeply technical, highly regulated sectors such as clean energy, healthcare, and infrastructure. Their innovations are less about market blitzing and more about resilience, compliance, and systems thinking.

The European Union supports this mindset with robust public funding for research (like Horizon Europe), strong worker protections, and frameworks for ethical innovation. The rise of B Corps, social enterprises, and circular economy models shows how innovation and purpose increasingly go hand in hand.

However, Europe’s strengths can also be its constraints. Risk aversion, bureaucratic inertia, and fragmented marketscan stifle ambition and delay digital transformation. There are fewer unicorns and less venture capital than in the U.S. Talent can be conservative, and scaling across borders is slowed by linguistic and legal complexity.

Yet Europe’s values-led approach positions it well for the next wave of innovation, especially in climate tech, digital trust, and responsible AI—areas where regulation and ethics are not barriers but competitive advantages.

Asia … Adaptive, Ambitious, and Systemic

Asia represents a third model—marked by adaptive pragmatism, national ambition, and technology-driven scale. In markets from China and India to Southeast Asia and South Korea, growth and innovation are often intertwined with nation-building, infrastructure development, and leapfrogging legacy systems.

Asian companies thrive in fast-growing, often chaotic markets, where customer needs are diverse and infrastructure is uneven. This has led to the rise of super apps, AI-based services, and platform-based business models that solve multiple problems at once. Think of Tencent’s WeChat, Grab in Southeast Asia, or Jio in India—each reimagining what a business can do by bundling services around digital lifestyles.

In China, companies like Bytedance, Alibaba, and Ping An have used data, AI, and ecosystems to create new forms of digital infrastructure—combining finance, commerce, healthcare, and entertainment. Innovation here is not just product-focused but systemic—built around whole-of-society digital platforms.

The role of government is critical. Unlike in the US, where the state often steps back, or Europe, where it regulates from the side, many Asian governments actively shape markets—setting industrial policies, funding tech R&D, building smart cities, and partnering with private companies. This creates rapid feedback loops between regulation, demand, and innovation.

Culturally, the Asian mindset is often collectivist, resilient, and entrepreneurial. There’s a strong bias for execution and iteration, often in highly competitive markets. While Western companies debate strategy, Asian startups tend to move quickly and adjust on the fly. Innovation is driven less by ideology and more by necessity and pragmatism.

Yet Asia’s innovation model also faces challenges. In China, state influence can lead to unpredictability, especially around data and regulation. In India, infrastructure gaps and bureaucracy can slow transformation. In many Asian countries, protecting intellectual property remains an ongoing issue.

Still, the continent’s speed, scale, and systems thinking have made it the most dynamic innovation region of the 21st century.

It’s increasingly difficult to make sense of the speed of progress.

The acceleration of AI is mind boggling, doubling in its power every 3 months. ChatGPT, Gemini and Perplexity, and many others, will soon be displaced by a new generation of agentic bots and intelligent interfaces. Transforming work, play, and almost every aspect of life. The advances in multionomics, or genetic engineering, are at a similar pace, and even more profound. Ready to transform our bodies, health, and our very concept of living. And more. Much more.

Our understanding of progress will continue to evolve. We will need to reflect on and adapt to what we think meaningful progress looks like. However, as the world moves towards more complexity, and in an era of quantum shifts, change is happening very quickly, making foresight both increasingly more challenging and more important.

At the start of 2025 I brought together over 100 trend reports, as a platform to share in keynotes and workshops, and also for my own sanity. Not being up to speed feels stressful, not being able comprehend seems alienating. But we all need more fluid minds to cope in today’s fast and complex spaces, to make some sense of the drama and dimensions of change.

I started with a trend kaleidoscope if you like, analysing all the reports, curating the most profound changes, relevant right now. You can download the presentation A to Z:

But then I needed to go much further.

Incredible Tech

There are many sources of foresight. Some accessible, some credible, some comprehensible. Most people tend to focus on technology. Revolutionary, rampant and remarkable. AI’s impact is already incredible, as its ability to galvanise other tech, and in particular networks (blockchain), multinomic (genetics), energy (storage), and robotics.

Two of the best future tech reports that come out each year have just been published

- Big Ideas 2025: ARK Invest focus on the opportunities for investors in a bewildering world of opportunity

- Tech Trends 2025: Future Today Institute’s epic 1000 page report on the tech and tech titans embracing it

Tech gets all the focus, the glamour, the hype. But the future is much more than tech. It’s how you use it.

Inspiring Possibilities

How can tech address the big challenges of a changing world – social mobility, climate change, and much more? How can tech align with human capability and social aspirations, to enable us to do more? How can tech be embraced within new business models to create real breakthrough innovations which can transform markets and business?

To go beyond tech, I love the annual reports from the Dubai Future Foundation. While they might sound like a provincial think tank, preoccupied with turning the UAE into a land of foresight, they are much more global thinking, and profound too. There are two fantastic reports, just published, exploring the big ideas for innovation and growth in a world of quantum shifts:

- Megatrends 2025: Exploring the 10 megatrends that are shaping the world over the next decade

- The Global 50: Focusing on the 50 big opportunities which these convergent trends offer us.

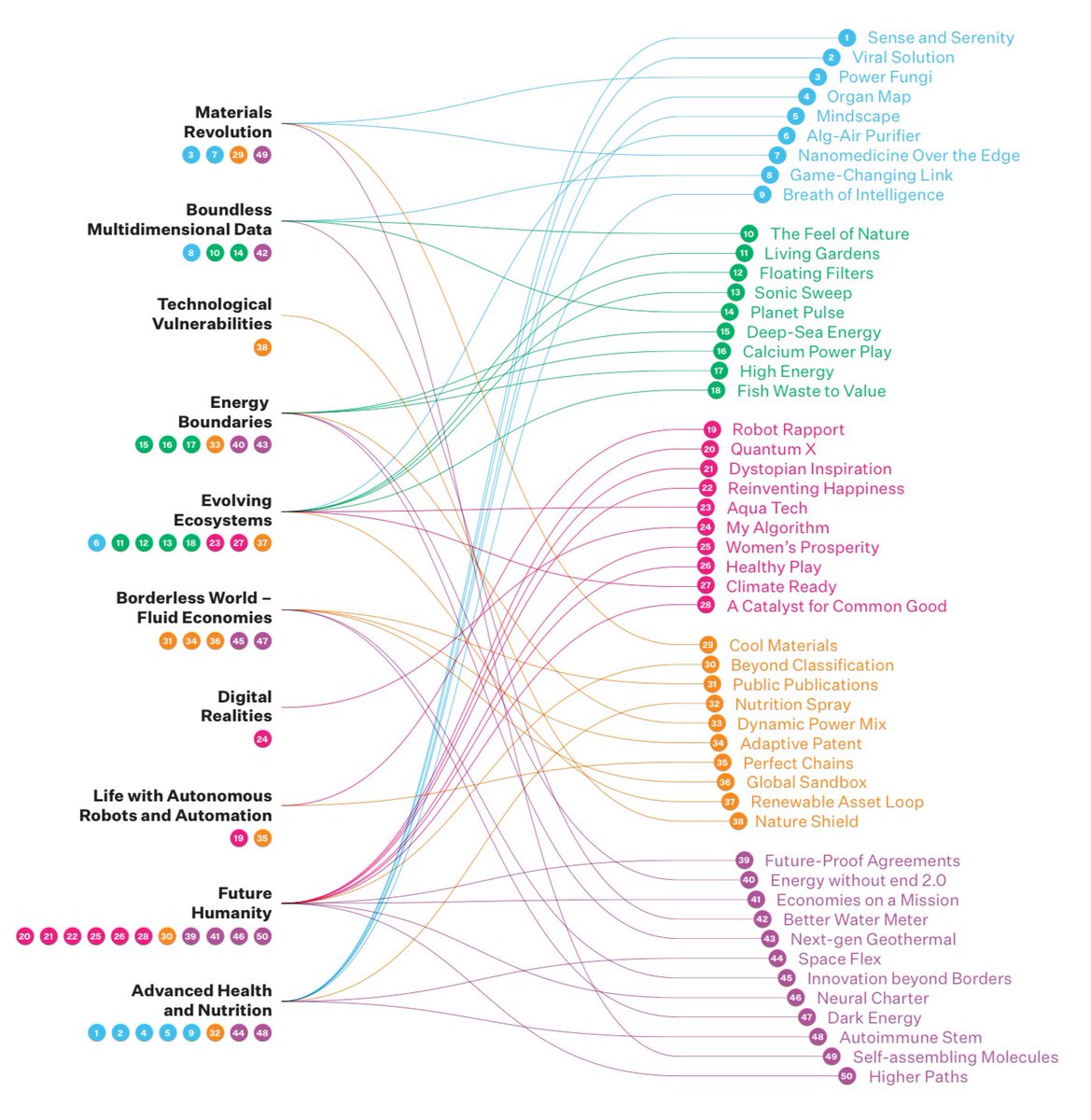

The emerging opportunities are driven by the convergent megatrends, and cluster into 5 significant opportunity spaces. The opportunities are defined in ways that sound futuristic, even fun, but have huge consequences for every government and corporation, startup and investor, in terms of how the rampant technologies and evolving societies could embrace them:

Opportunity Space 1: Health Reimagined … Redefine mental and physical health, support longer lives, drawing on science, technology and nature for better health and new ways to personalise access for individuals and communities everywhere.

- Sense and Serenity

- Viral Solution

- Power Fungi

- Organ Map

- Mindscape

- Alg-Air Purifier

- Nanomedicine Over the Edge

- Game-Changing Link

- Breath of Intelligence

Opportunity Space 2: Nature Restored … Minimise environmental risks and harness nature’s capacity to restore itself or have a positive impact on crucial environmental ecosystems and habitats, creating a more stable, healthier planet for all.

- The Feel of Nature

- Living Gardens

- Floating Filters

- Sonic Sweep

- Planet Pulse

- Deep-Sea Energy

- Calcium Power Play

- High Energy

- Fish Waste to Value

Opportunity Space 3: Societies Empowered … Empower societies by offering solutions to humanity’s most complex and universal needs, optimising systems they rely on, safeguarding risks that could make societies more fragile in the face of crises, and extending individual and collective potential for growth and development.

- Robot Rapport

- Quantum X

- Dystopian Inspiration

- Reinventing Happiness

- Aqua Tech

- My Algorithm

- Women’s Prosperity

- Healthy Play

- Climate Ready

- A Catalyst for Common Good

Opportunity Space 4: Systems Optimised … Improve and build more effective and resilient systems underpinning advances in services and solutions at various levels of business, government and society.

- Cool Materials

- Beyond Classification

- Public Publications

- Nutrition Spray

- Dynamic Power Mix

- Adaptive Patent

- Perfect Chains

- Global Sandbox

- Renewable Asset Loop

- Nature Shield

Opportunity Space 5: Transformational … The power to radically change ways of life by replacing the models that countries, communities and individuals live by. These new models enable individuals and communities to innovate and improve the transformation of humanity to new digital and non-digital realities.

- Future-Proof Agreements

- Energy without end 2.0

- Economies on a Mission

- Better Water Meter

- Next-gen Geothermal

- Space Flex

- Innovation beyond Borders

- Neural Charter

- Dark Energy

- Autoimmune Stem

- Self-assembling Molecules

- Higher Paths

Innovative Reinvention

The big question for most of us, is then how can we embrace these incredible opportunities within the businesses of today? How will they help to transform our mindset about possibilities, to supercharge innovation, to accelerate growth, to reinvent business?

Look around us, and we already have so many incredible innovators shaking up every market, not just through product innovations but through fundamental reinvention of organisations, markets, and entire industry sectors.

So which are the innovative companies around the world that inspire you? My passion is to track down and learn from the world’s most inspiring companies – disrupting conventions, reinventing business models, innovating and transforming, creating value with positive impact. Fast Company is a great source of inspiration, and has just launched their latest ranking

- Most Innovative Companies 2025: from Waymo to Nvidia, Nubank and RocketLab

- Most Innovative Companies by Sector: from Advertising to Agriculture, Architecture to Automotive

Every one of these companies has a fabulous story, and great insights in terms of how to unlock the new opportunities of change, and how to drive innovation for practical, profitable success. I typically focus most on their leaders, what inspires them, and their strategies, what drives their futures. You can explore many more on my website, A to Z of the Most Inspiring Companies.

What can you learn from them? In this world of incredible possibility, what will you do?

Because the future starts here. Next is now.

Reinventing Inditex

Pablo Isla has arguably created a blueprint for 21st century fashion retail.

I recently sat down with him, to talk about his career (he was twice ranked by HBR as the world’s #1 CEO) and the future of fashion retailing. We talked about the changing world and transformational change, AI and sustainability, faster fashion and much more. He struck me as quiet and thoughtful, but also visionary, provocative and clearly an inspiring leader.

For 16 years Pablo Isla was CEO (and chairman) of Inditex (one of the world’s leading fashion retail groups with brands like Zara, Bershka, Massimo Dutti, Pull & Bear, and Stradivarius) and grew the market value of the company by over 450% (from €13 billion to over €100 billion, 2005 to 2019), while doubling sales and tripling profitability.

I asked him how. As business leader over these years, was his mindset largely about selling more, doing the same thing better and better. Or was it about reinvention, from product and process innovation, all the way to reinventing brand concepts and business models?

He was emphatic … “In retail, you can never stand still. You have to reinvent yourself constantly, not just every year, but every season, every week” … with the changing aspirations and influences of consumers being the biggest driver.

Zara, of course, was a pioneer of fast fashion. Yet in today’s markets, with challenger brands like Shein and Temu, fast has become ultra-fast. And, at the same time, other agendas have become important, such as sustainability and performance – from reducing emissions and waste, to developing high-tech fabrics and consumer loyalty.

“Innovation is not just about technology. It’s about rethinking how we design, produce, distribute, and communicate — faster, smarter, and more sustainably” he reflects.

He transformed Inditex into the world’s most agile, digitally integrated, and sustainable fashion retailer, with a major shift toward digital retail, investing early and heavily in integrating online and physical retail. He also positioned Inditex as a leader in sustainable fashion, committing to 100% sustainable cotton, linen, and polyester by 2025. Plus zero landfill waste and use of renewable energy across logistics and manufacturing.

Global retail to thoughtful fashion

While Inditex is one of the world’s largest fashion retailers, the much smaller Aster Textile is one the most interesting manufacturers of fabrics and clothing. Having worked with the leadership team of the fast-growing Turkish business for the last 7 years, I’ve watched the rapidly changing opportunities and priorities of the fashion industry.

Aster started as a business designing and producing vast ranges of basic cotton tees and sweats for companies like H&M and M&S (and typically as the lowest cost). Today it has transformed into a company that puts high performance, sustainable fabrics first. And now partners with leading brands like Hugo Boss and Lacoste, On and Zegna.

“Thoughtful fashion” is Aster’s purpose statement. And in strategy workshops, trend analysis and business planning, I help them to think deeply and differently about what it takes to win in the fashion world today, and tomorrow. Indeed, a very practical symbol of this change is Aster’s acquisition and development of its subsidiary business, Artesa, a futuristic state-of the-art fabric development business.

Some of Aster’s future is obvious. We know fashion is relentless. And increasingly it not just how things look, but how they perform too. New materials, innovative fabrics, new techniques, innovative designs.

But it’s also about how brands and retailers work together, and how they work differently with consumers. For example in terms of new business models like Stitch Fix, delivering new types of experiences like Coke 3000, built around new communities like Nike’s SNKRS.

What’s the future of fashion?

The global fashion industry is undergoing a profound transformation. Faced with growing pressure to address climate change, shifting consumer values, and the rise of technology, brands and designers are rethinking every aspect of the fashion value chain—from the materials used to make clothes to how they’re designed, sold, and worn. This reinvention is not just about sustainability or aesthetics—it’s about building entirely new models of fashion that are smarter, fairer, and more future-ready.

1. Bio-Based, regenerative, and circular materials

Textiles are at the heart of fashion’s transformation. Emerging companies are developing innovative fabrics that challenge traditional norms.

For instance, Matereal recently launched Polaris, a bio-based replacement for polyurethane, dramatically reducing the environmental footprint of coated fabrics. Similarly, Modern Meadow and Bolt Threads are leading pioneers in biofabrication. Bolt Threads has developed Mylo, a leather alternative made from mycelium (mushroom roots), already used by brands like Stella McCartney and Adidas.

Circular innovation is also taking hold. Companies like Refiberd use AI and hyperspectral imaging to analyze discarded garments for recycling, helping to close the loop on textile waste. In parallel, Renewcell in Sweden recycles worn-out cotton and viscose into new fabric feedstock, branded as Circulose, which H&M and Levi’s have incorporated into their collections.

These material innovations reduce fashion’s reliance on oil-based synthetics, toxic dyes, and water-intensive natural fibers—marking a fundamental shift toward regenerative fashion systems.

2. Agile, on-demand, and AI-powered production

One of fashion’s greatest inefficiencies has always been its inventory problem—producing too many garments, too far in advance. That’s beginning to change.

The concept of agile retail, pioneered by platforms like MannyAI, uses real-time consumer data to forecast demand and trigger production only when needed. This minimizes overstock and waste while allowing brands to respond more quickly to trends.

Some labels are taking this even further. Unspun, a San Francisco-based startup, uses 3D scanning to create jeans custom-fitted to each shopper—produced on-demand with minimal waste. Similarly, PlatformE, a Portuguese tech company, enables luxury brands to personalize products at scale, powering the rise of “mass customization.”

AI is also transforming supply chains. Tools like Tilkal and TrusTrace provide transparency and traceability across suppliers, helping brands ensure ethical sourcing and verify sustainability claims.

3. Secondhand, rental, and resale models

Resale is no longer niche—it’s one of the fastest-growing segments of the fashion industry. According to ThredUp, the secondhand market is projected to grow three times faster than the global apparel market by 2030.

Luxury and high-street brands alike are embracing resale. Gucci has partnered with The RealReal, while COS Resell, Patagonia Worn Wear, and Lululemon Like New offer platforms for customers to buy and sell pre-loved garments directly.

Meanwhile, rental platforms like HURR (UK), Rent the Runway (US), and Style Theory (Southeast Asia) are shifting consumer behavior by promoting access over ownership. These services allow people to rotate wardrobes without contributing to overproduction or clutter.

This trend reflects a deeper mindset shift: clothes are no longer disposable, but valuable assets to be shared, traded, or revived.

4. Digital fashion and virtual garments

The rise of the metaverse and digital identity has given birth to a bold new category: digital-only fashion.

Companies like DRESSX and Tribute Brand design 3D garments that exist purely in virtual environments. Consumers can “wear” these digital clothes on social media, in video games, or augmented reality experiences. This creates new forms of self-expression without the environmental impact of physical production.

Luxury brands are experimenting, too. Gucci launched its Gucci Vault as an experimental space blending NFTs, digital wearables, and metaverse experiences. Meanwhile, digital-native fashion houses like The Fabricant collaborate with artists and brands to create couture for avatars, while building new economic models around NFTs and blockchain-based ownership.

Digital fashion also plays a role in design prototyping, enabling brands to visualize and refine garments before cutting any fabric—saving time, money, and materials.

5. Inclusive and purpose-driven brands

Inclusion, transparency, and values-led branding are now competitive advantages.

Emerging designers are leading the way. The 2025 CFDA/Vogue Fashion Fund finalists include names like Ashlynn Park (Ashlyn) and Julian Louie (Aubero), who are exploring themes of gender fluidity, cultural identity, and mental health through fashion.

Social innovation is also rising. Brands like Fashion Revolution and Tonlé prioritize ethical labor, zero-waste production, and community empowerment. In Africa, Studio 189 (co-founded by Rosario Dawson and Abrima Erwiah) promotes artisan-made fashion while supporting economic development in Ghana.

Even larger companies are responding. Nike has launched adaptive apparel for people with disabilities, and Tommy Hilfiger Adaptive continues to expand its universally designed collections.

Consumers—especially Gen Z—are demanding accountability, diversity, and purpose in the brands they support. The fashion industry is responding by building deeper connections, not just pushing products.

6. Localism, upcycling, and craft

Global fashion is becoming more local—and personal. The slow fashion movement, long popular in Scandinavia and Japan, is now gaining traction worldwide.

Brands like E.L.V. DENIM in London make high-end jeans entirely from upcycled materials, hand-cut and tailored in East London. In India, designers like Kriti Tula of Doodlage create one-of-a-kind pieces from factory waste, preserving craft traditions while reducing textile landfill.

Elsewhere, Bode in New York celebrates vintage fabrics, storytelling, and embroidery in menswear; while Cecilie Bahnsen in Denmark handcrafts romantic, voluminous pieces with timeless quality.

These models challenge the idea of “newness” and elevate slowness, repair, and authenticity as fashion ideals.

Inspired by ideas from beauty, entertainment, sports

Fashion, once a seasonal and product-centric industry, is now under pressure to become faster, more digital, and more emotionally connected to consumers. As trends accelerate and consumer values shift, the most forward-thinking fashion brands are increasingly looking outside their sector—to beauty, entertainment, and sports—for inspiration on how to innovate and reinvent. These adjacent industries offer valuable lessons in agility, engagement, platform thinking, and purpose-led growth.

From the beauty sector, fashion can learn the power of community and co-creation. Brands like Glossier have built empires not on advertising but on direct customer dialogue and user-generated content. Glossier invited fans into the product development process, listened to feedback, and created a feedback loop that feels authentic and empowering. Similarly, Fenty Beauty disrupted the cosmetics world by embracing radical inclusivity, launching 40 foundation shades and redefining representation. Fashion brands are now following suit—SKIMS, for example, applies similar inclusivity and community-building to shapewear and loungewear, creating cultural resonance and loyalty.

In entertainment, innovation revolves around storytelling and immersive worlds. The rise of the “experience economy” has shown that people want more than products—they want narratives and emotional connection. Luxury fashion houses like Balenciaga and Gucci have embraced this by launching collections inside video games, such as Fortnite and Roblox, or staging surreal digital runway shows that feel more like film than fashion. Moncler’s Genius project is another standout, using artist and designer collaborations to reimagine the brand’s DNA in ever-evolving drops—blurring the lines between fashion and cultural performance.

The sports industry, particularly brands like Nike, offers a masterclass in ecosystem thinking. Nike doesn’t just sell sneakers—it sells a lifestyle powered by community, data, and performance. Through apps like Nike Run Club and SNKRS, it combines social connection, personalized recommendations, exclusive content, and gamification. The result is a highly engaged customer base that sees the brand not just as a retailer, but as a partner in personal progress. Fashion brands like Lululemon and On Running have adopted similar models, blending retail, wellness, events, and digital tools into unified ecosystems that build long-term loyalty.

Globally, brands are also experimenting with cultural hybridity and hyper-localization—learning from K-pop, anime, streetwear, and sneaker culture. Japanese brand Ambush, founded by Korean-American designer Yoon Ahn, fuses fashion with music, gaming, and pop culture, while India’s Sabyasachi combines traditional craftsmanship with global luxury aesthetics, using storytelling to elevate heritage into modern desirability.

The key lesson across sectors is that innovation is not just technological—it’s cultural and strategic. Fashion brands must embrace agility, purpose, and participation, evolving from static labels into dynamic platforms. By learning from the beauty industry’s inclusivity, the entertainment world’s immersion, and sport’s ecosystem thinking, fashion can reinvent itself for a future defined not just by style, but by meaning, emotion, and connected experience.

Reinventing fashion brands and retail

To reinvent themselves for the future, fashion retailers and brands must move beyond just selling clothes — toward becoming platforms for identity, culture, and sustainability. The future of fashion lies in fusing creativity with technology, sustainability with scalability, and personalization with global relevance. Reinvention isn’t just about new products, but new value propositions, business models, ecosystems, and mindsets.

Fast Fashion to Smart Fashion

- Shift from mass production to on-demand, data-driven production.

- Use AI and predictive analytics to design and stock what consumers actually want.

- Reduce overproduction and waste.

Example: Zara has integrated RFID and real-time inventory systems to better align demand and supply.

Brand-Centric to Community-Driven

- Build fashion communities — not just customer bases.

- Engage fans in co-creation, feedback, and shared values.

- Leverage UGC, creators, and digital influencers.

Example: Glossier in beauty built a brand entirely on community feedback and engagement.

Ownership to Access

- Embrace rental, resale, and circular models.

- Monetize fashion through subscription services, digital wardrobes, and lifetime value.

- Promote circularity as a premium experience.

Example: Rent the Runway and Vestiaire Collective have redefined fashion access and reuse.

Stores to Experience Hubs

- Reinvent physical retail as immersive, multi-sensory spaces.

- Combine storytelling, technology, and social media appeal.

- Offer in-store exclusives, events, or services that can’t be found online.

Example: Nike’s House of Innovation in NYC blends AR, personalization, and real-time customization

Apparel to Identity Platforms

- Expand into lifestyle, wellness, beauty, gaming, or even mental health.

- Fashion becomes part of the creator economy and self-expression across channels.

Example: SKIMS by Kim Kardashian blends fashion, pop culture, body positivity, and functional design.

Physical Fashion to Digital Fashion

- Tap into virtual fashion, NFTs, avatars, and metaverse experiences.

- Brands create virtual collections, sell skins for avatars, or dress influencers’ AI twins.

Example: Balenciaga launched digital collections in Fortnite, while Drest lets users style virtual models with real luxury looks.

Linear to Regenerative Fashion

- Regenerative farming for raw materials (cotton, wool).

- Brands invest in take-back schemes, upcycling, and closed-loop production.

Example: Patagonia’s “Worn Wear” and Allbirds’ carbon accounting per product.

What to do next?

Fashion brands and retailers need to reframe their thinking. To move beyond the conventional mindsets of clothing and stores, to reimagine how they can most effectively add value:

-

Think like a tech company: agile, iterative, data-rich.

-

Act like a media brand: emotional, story-led, culturally attuned.

-

Operate like a sustainability pioneer: transparent, circular, responsible.

-

Move like a lifestyle platform: fluid across categories, channels, and markets.

In a time of accelerated disruption, technological breakthroughs, and mounting global uncertainty, the ability to adapt is no longer a competitive advantage — it’s a survival imperative.

Companies that once thrived on scale, efficiency, or dominance can now be outpaced by agile startups or overwhelmed by global crises almost overnight. In this environment, being “future-ready” means building a business that is constantly reinventing itself — anticipating change, embracing innovation, empowering talent, and aligning deeply with the evolving needs of society and the planet.

Paul Polman, former CEO of Unilever, captures the mindset, saying “The businesses that are going to survive and thrive are the ones that take responsibility for the future.” He transformed Unilever into a sustainability leader, linking future-readiness to broader stewardship.

Klaus Schwab, founder of the World Economic Forum says “In the new world, it is not the big fish which eats the small fish, it’s the fast fish which eats the slow fish.” He underscores speed, agility, and adaptability as critical for survival in the modern economy.

But what does it really mean to be a future-ready business? And how are organizations around the world redesigning themselves to thrive amid the chaos?

Future-Ready Mindset

Satya Nadella of Microsoft says “Our industry does not respect tradition — it only respects innovation.” His transformation of Microsoft highlights the importance of continual reinvention and forward-looking leadership.