“iMarketing” is more than a digital platform with a profusion of mobile apps, social media and community building, big data enabling clever analytics. Marketing is already on its own transformational journey from mass and anonymous, to personal and predictive. However the journey is just in its infancy. Much more is to come in the next 3 years, a fundamental change in how we engage customers and build brands. With the help of ChiefMarTec and others, here are some of the big drivers and impacts:

- Digital transformation redefines “marketing” beyond the marketing department.

- Microservices & APIs (and open source) form the fabric of marketing infrastructure.

- Vertical competition presents a greater strategic threat than horizontal competition.

- AR, MR, VR, IoT, wearables, conversational interfaces, etc. give us digital everything.

- Artificial intelligence multiplies the operational complexity of marketing and business.

1. DIGITAL TRANSFORMATION

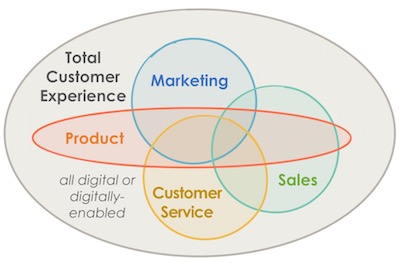

The essence of digital transformation is that marketing, sales, service — and most of all — product are all being entwined together under the banner of “customer experience.”

Naturally, that makes sense from the customer’s point-of-view. How much delight or disgust do customers feel across the entire spectrum of engagements they have with your company, from the very first touchpoint onward?

Their whole end-to-end experience is the product.

The five things that make this transformational are:

- All of these touchpoints are either digital or digitally-supported.

- Orchestrating these touchpoints is inherently a cross-organizational mission.

- Marketing is increasingly at the center of that orchestration.

- Marketing is embedded in the product (and, vice versa, product in the marketing).

- The resulting end-to-end experience for customers is how smart companies are disrupting their competitors — e.g., Uber isn’t the car ride, it’s the whole seamless experience.

A report produced a couple of months ago by the CMO Council asked CMOs to identify one — and importantly, only one — top mandate that they had for the year ahead. As shown in the chart below, 67% reported a cross-organizational mandate on growth and/or customer experience.

Of course, it’s one thing to talk about customer experience, another to actually effect it.

But as Barry Levine wrote on MarTech Today a couple months ago, “At our most recent MarTech Conference, there seemed to be a transformation percolating throughout the sessions and presentations. After several false starts in previous years, it seemed to me that ‘marketing’ is now clearly becoming something bigger.”

In many ways, marketing is looking, sounding and feeling less like its traditional role of “demand generation” and more like “experience management.” — Barry Levine

David Edelman, CMO of Aetna, emphasized in his keynote at MarTech how marketing was now deeply engaged in helping to shape customer experience — including pioneering mobile and wearable touchpoints that innovate the very nature of the relationship between the company and its customers.

Successful marketing-led customer experience projects and programs shared by other speakers at MarTech included:

- Keurig Green Mountain, launching connected coffee machines that enable a whole new kind of digitally-augmented customer experience with their products

- Staples, using marketing analytics to map and improve steps across the customer journey that spanned traditionally separate teams within the firm

- Dr. Martens, implementing omni-channel personalization seamlessly across email, their e-commerce site, and social media in ways that genuinely amplified their brand

And that’s just a representative sample. The thing that they all have in common: marketing is being embedded into the product/service and the end-to-end customer experience.

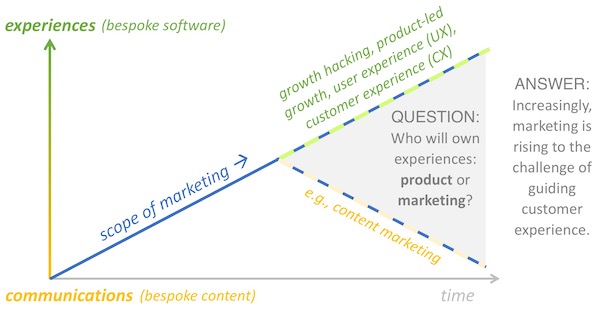

Last year I wondered whether marketing would continue to rise to the challenge of this scope explosion — from communications to experiences. Over the past year, I’ve been excited to see so many marketing teams embrace this opportunity in the charge of digital transformation.

But there’s another aspect of digital transformation in marketing that I’ve noticed over the past year: the changes in what marketers were actually doing. Not just shifts in their mission — i.e., delivering delightful customer experience. But shifts in what they’re building with their hands and minds to achieve that mission.

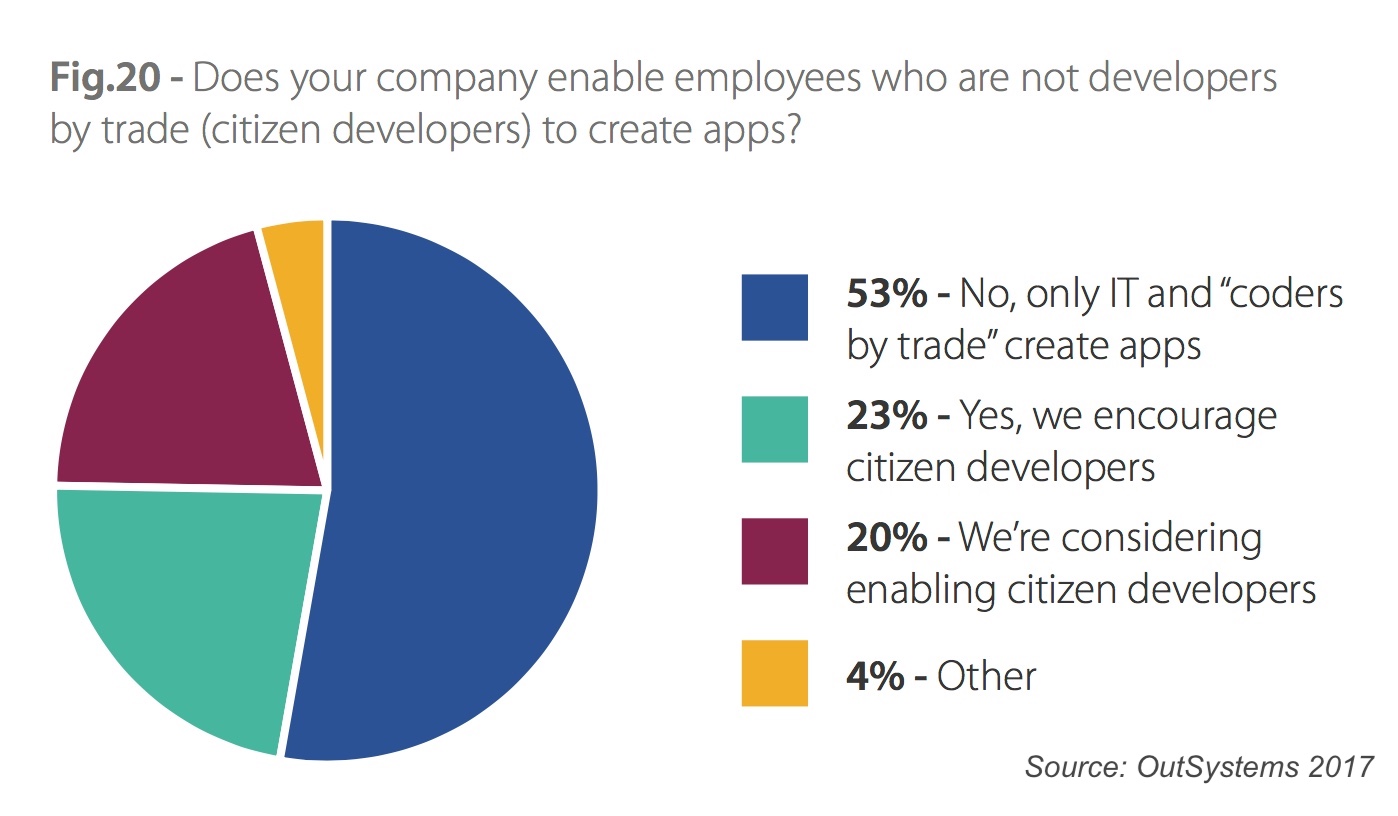

Empowered by a plethora of marketing technologies that are widely accessible to and usable by non-technical, “generalist” marketers, ordinary citizens of the marketing department have increasingly become do-it-yourself wizards in crafting digital interactions with customers, digital workflows throughout their organizations — beyond marketing, into sales, service, finance, etc. — and dynamic data dashboards, models, and reports.

I use the phrase “citizens of the marketing department” quite intentionally, because these wizard-like capabilities that marketers are acquiring align with three big IT-democratization movements:

- CITIZEN DEVELOPERS — who use no-code or low-code tools to create web apps, mobile apps, interactive content, bots, and other kinds of functionalexperiences for staff, prospects, and customers

- CITIZEN INTEGRATORS — who use iPaaS and other workflow automation tools to create business processes on-the-fly, intelligently routing data and triggering activities across multiple teams

- CITIZEN ANALYSTS or even CITIZEN DATA SCIENTISTS — who easily pull together business intelligence data from a variety of sources on demand, analyze it, visualize it, tease out insights, and even automate decisions around it

That’s not to say that these “citizens” have eliminated the need for “experts” wholesale. There is still plenty of work that requires professional developers, systems integrators, and data scientists. But the scope of what individual marketers can build on their own is astounding — and unprecedented.

This is digital transformation in a company’s internal ecosystem. The kind of power that would have taken teams of experts and weeks of work to implement an idea even just 5 years ago is now in the hands of individual citizen marketers to instantiate almost immediately.

And as marketing technology continues to race forward, their power to create only grows.

2. MICROSERVICES & APIS

The rise of citizen technologists — citizen developers, citizen integrators, citizen analysts, and so on — was largely enabled by two big movements in the software world:

- Cloud computing — most data and applications are now accessible on-demand through ubiquitous connectivity from anywhere across the globe.

- Microservices & APIs — these cloud-based solutions have evolved from closed, monolithic applications with solely human UIs into more open services that also expose APIs for other software applications to interact with them and mash those capabilities together into whole new solutions.

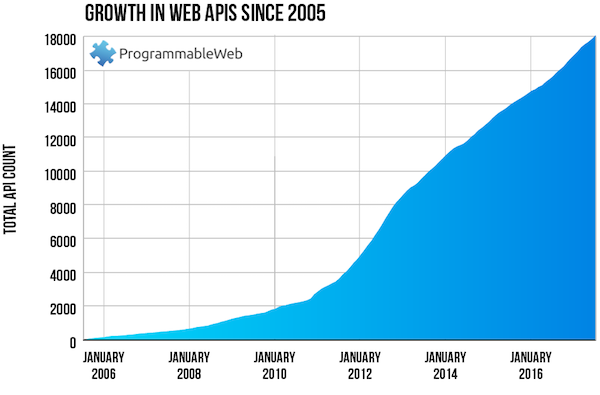

The mash-up possibilities of APIs have inspired an explosion of combinatorial innovation. Partners and customers can now leverage these machine interfaces to businesses to drive their own digital transformation, which has given rise to the “API economy.”

You can get a sense of how fast the API economy has been growing from this chart of public APIs listed on the Programmable Web directory from 2005-2017 — which captures just a tiny, tiny fraction of the total number of APIs available out there: In addition to allowing different applications and businesses to cross-connect, the advantages of cloud-based APIs have changed how core applications themselves are designed and built. Increasingly, they are architected as a collection of microservices that use APIs internally to assemble a large solution out of dozens or hundreds of small, flexible components.

In addition to allowing different applications and businesses to cross-connect, the advantages of cloud-based APIs have changed how core applications themselves are designed and built. Increasingly, they are architected as a collection of microservices that use APIs internally to assemble a large solution out of dozens or hundreds of small, flexible components.

Key advantages of this microservices approach:

- The individual microservices can evolve more rapidly.

- The larger solution can add and remove microservice components more easily.

- These microservices can potentially be exposed as stand-alone offerings for others to leverage, internally or externally (e.g., touchpoints in the API economy).

This is happening in the context of tremendous adoption of cloud-based apps of all sizes across the entire organization.

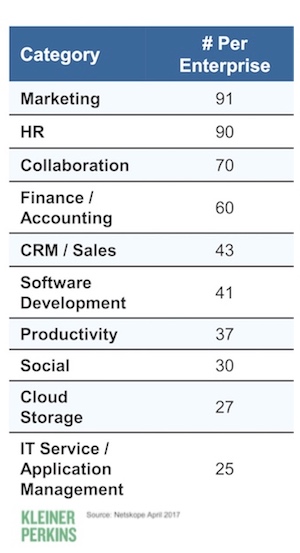

As reported in Mary Meeker’s State of the Internet report earlier this year, the average enterprise uses 1,000 cloud services.

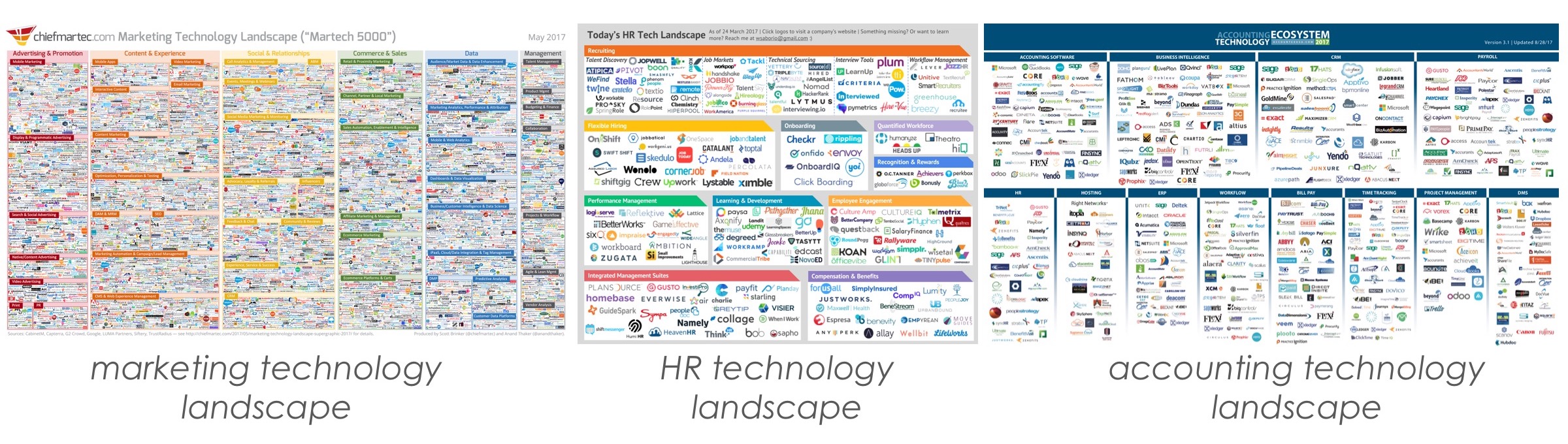

And while enterprise marketing departments use an average of 91 cloud services, HR is using 90, finance and accounting are using 60, sales are using 43, and so on.

The marketing technology landscape is not an anomaly. There are now large tech landscape graphics for every department across the organization:

Where things get really exciting is the combination (literally!) — all these cloud services, most of them offering more and more APIs, and a whole Internet of other public APIs, including for services such as Google, Facebook, Twitter, and so on — ready to be “mashed up” together.

This opportunity is where iPaaS (integration-platform-as-a-service) solutions have blossomed: Zapier, Workato, PieSync, Azuqua, IFTTT, Segment, Automate.io, Dell Boomi, Bedrock Data, Scribe, Built.io, Flowgear, Elastic.io, SnapLogic, MuleSoft, Tray.io, and dozens of others.

iPaaS handles these technical integration to these cloud services and Internet APIs, often through out-of-the-box “connectors.” Non-technical business users can then drag-and-drop connections between them to create their own workflows and automations across them.

iPaaS makes these business users — such as marketers — citizen integrators.

A report released earlier this year by AGC Partners — discussed in detail in my post back in July, Is marketing technology entering a post-platform era? — quantifies the growth of the overall “integration sector,” including iPaaS solutions as just one small piece:

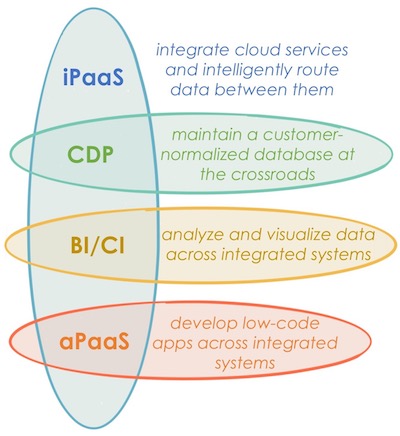

As I’ve studied the iPaaS market, I’ve come to realize that there’s considerable overlap with other growing martech categories:

- CDPs (customer data platforms)

- business/customer intelligence platforms

- aPaaS (application-platform-as-a-service)

Essentially, all of these solutions make it easy to integrate cloud services and intelligently share data between them.

Pure iPaaS solutions focus on the workflow and data routing between these services.

CDPs extend that model by maintaining a customer-normalized database at the crossroads of those integration — storing the the data that is being routed through their hub.

Business/customer intelligence platforms — including a cornucopia of “dashboard” products — focus on analyzing and visualizing the data that’s accessible through all of these integrations.

And low-code/no-code aPaas solutions let citizen developers build internal or external “apps” that leverage data and API services from across all of these connected applications.

This is what led me to conclude that we’ve entered a post-platform era. With all these cross-application integrations in the cloud, everything is becoming an open platform to a certain degree. There’s far less exclusivity to software platforms than we saw in the pre-cloud era.

By the way, if you’re wondering how I think about post-platform dynamics given my new role as VP platform ecosystem at HubSpot, I believe a platform’s success isn’t just about APIs — that’s table stakes today. It’s about a qualitatively greater relationship with the ecosystem.

Successful platforms enable third-party products to be deeply integrated in the data models, workflows, and user experience of a platform’s key users. They create a business ecosystem that facilitates the adoption of those third-party products.

A great platform in the post-platform era is the center of gravity for a particular group of professionals or a business function — where that gravitational field meaningfully orchestrates the ecosystem of services and data sources orbiting its star. (If you’re interested, I’ve recently written about the 7 elements of a lovable platform that I believe help create that center of gravity for third-party developers.)

A post-platform world is actually a world of many, many interconnected platforms. But not all platforms are equal in the context of the audience they serve.

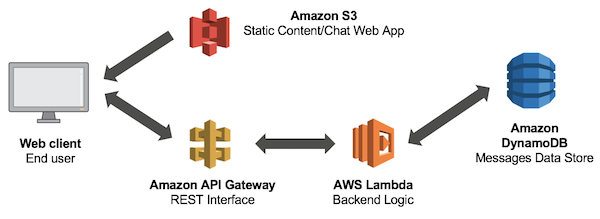

By the way, one other, slightly “techy” trend to keep an eye on in the evolution of microservices and APIs is serverless computing. “Serverless” lets software developers deploy small pieces of functionality up in the cloud without having to explicitly think about the operational aspects of running that code. The cloud provider, such as Amazon Web Services, does that all auto-magically behind the scenes.

It’s worth reading about Amazon’s AWS Lambda service, which was one of the first commercial serverless providers, to learn about the benefits they offer developers.

Now as a marketer, why should you care? Serverless will make it even easier for there to be a near-infinite explosion of small pieces of software functionality, spread throughout the cloud, which can be assembled and orchestrated on-the-fly by flexible and ever-more-dynamic business applications and workflows.

The days of closed, monolithic software are over, and this will continue to be a big disruption in how marketing operates — and what it makes possible.

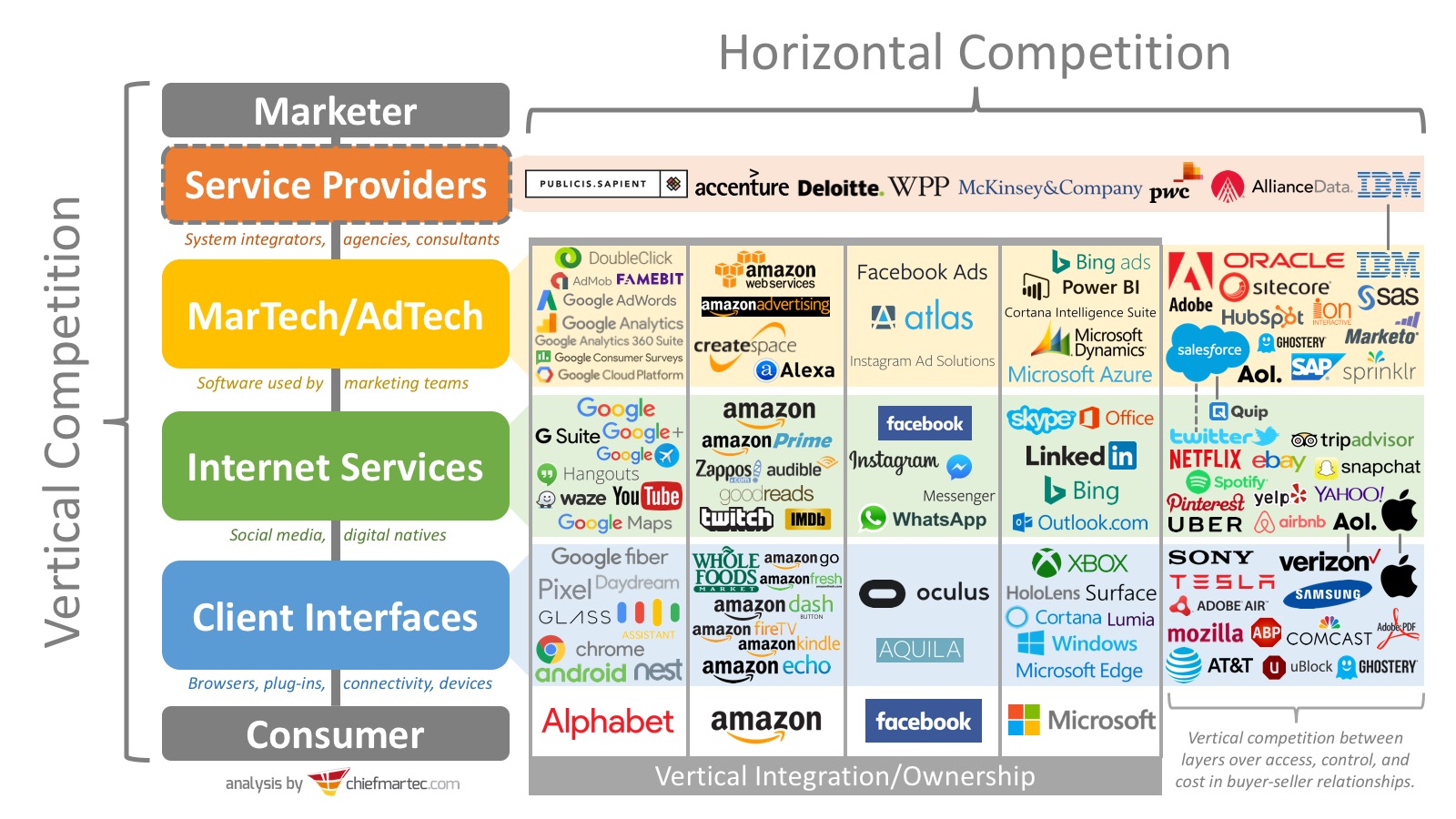

3. VERTICAL COMPETITION

I have been writing about vertical competition in digital marketing for several years: how companies at different points along the pathway between the marketer and the customer exert power and extract value.

The most powerful “competitor” in vertical competition is one who has an exclusive gateway to the customer. If you want to reach customers through their channel or touchpoint, you must agree to their terms — or forgo access.

I think it’s one of the most disruptive force in business today, in part because companies are less likely to see it coming. It’s easy to see Oracle and Salesforce as competitors in martech (they’re horizontal competitors vying with each other at the same stage of the channel). It’s less easy to see Facebook, Amazon, or Verizon as “martech” competitors to Oracle and Salesforce — but in the big picture of vertical competition, they are.

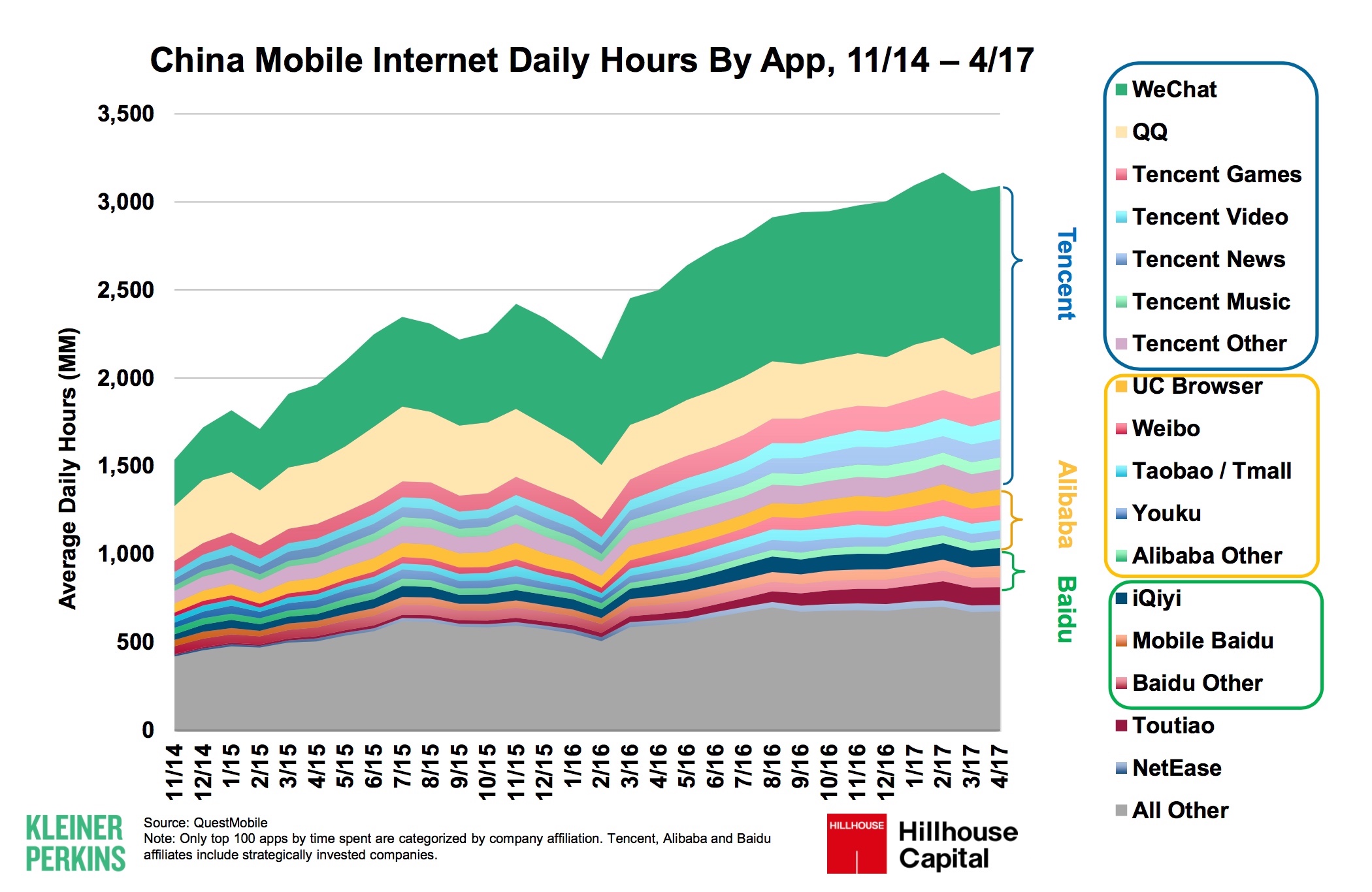

For a large scale example of vertical competition dynamics in digital channels, look at the incredible power wielded in the Chinese Internet market by Tencent, Alibaba, and Baidu. They control the interface — and data — of the vast majority of consumers in that market. Marketers who want to reach those buyers digitally, must do it through their marketing solutions, such as Alibaba’s Uni Marketing suite or One Tencent’s integrated marketing services.

However, here in the US, we’re seeing vertical competition on the Internet grow too.

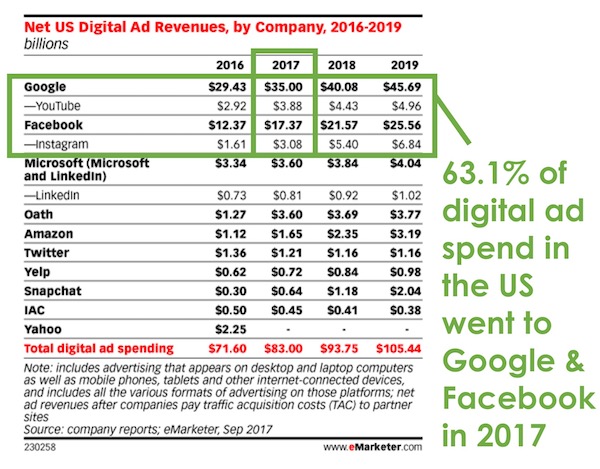

The most common example is the duopoly of Google and Facebook in digital advertising. 63.1% of all advertising dollars in the US went to those two companies — and their portfolio of sites, such as YouTube and Instagram.

They wield enormous power because there are few substitutes for reaching their audiences. If you’re unhappy with Google’s search advertising prices and policies, what are you going to do? Move your search spend to Bing? (Sorry, Microsoft — I love you.)

Same with Facebook and Instagram. Snap and Pinterest might be competitors, but they’re not really substitutes.

This is why, despite vocal resistance from major advertisers such as Proctor & Gamble over measurement and visibility issues, Google and Facebook have each been able to hold on to their dominance. Third-party adtech vendors aren’t able to be of much help, as they don’t have a lot of weight against Facebook or Google to force their way into those walled gardens.

![]()

And the strength of Facebook and Google reach beyond their walled gardens. They’ve been highly successful at having independent websites install their “tracking” scripts — whether it’s for Google Analytics or Facebook Connect.

The latest Tracking the Trackers study conducted by Ghostery found that Google had its scripts on almost half of the pages they found on the web; Facebook has its on more than a fifth.

But the Facebook-Google digital ad duopoly is only one example of vertical competition.

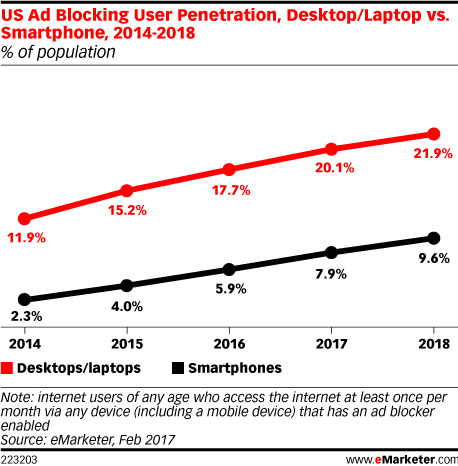

In the battle for digital advertising, ad blockers are another kind of vertical competitor that have continued to grow in 2017.

When a user has installed an ad blocker on their computer or mobile device — that “last mile” between the marketer and the consumer — much of the power of adtech vendors (and even Internet service juggernauts such as Google and Facebook) can be diminished by these client-side players.

In fact, it’s at the client stage — the touchpoint used by the consumer and how it is connected to the Internet — that the biggest struggles in vertical competition are emerging.

Web browsers were relatively weak vertical competitors because they were effectively commoditized. But now, we have an explosion of new proprietary devices and apps that have more power as exclusive touchpoints to select audiences.

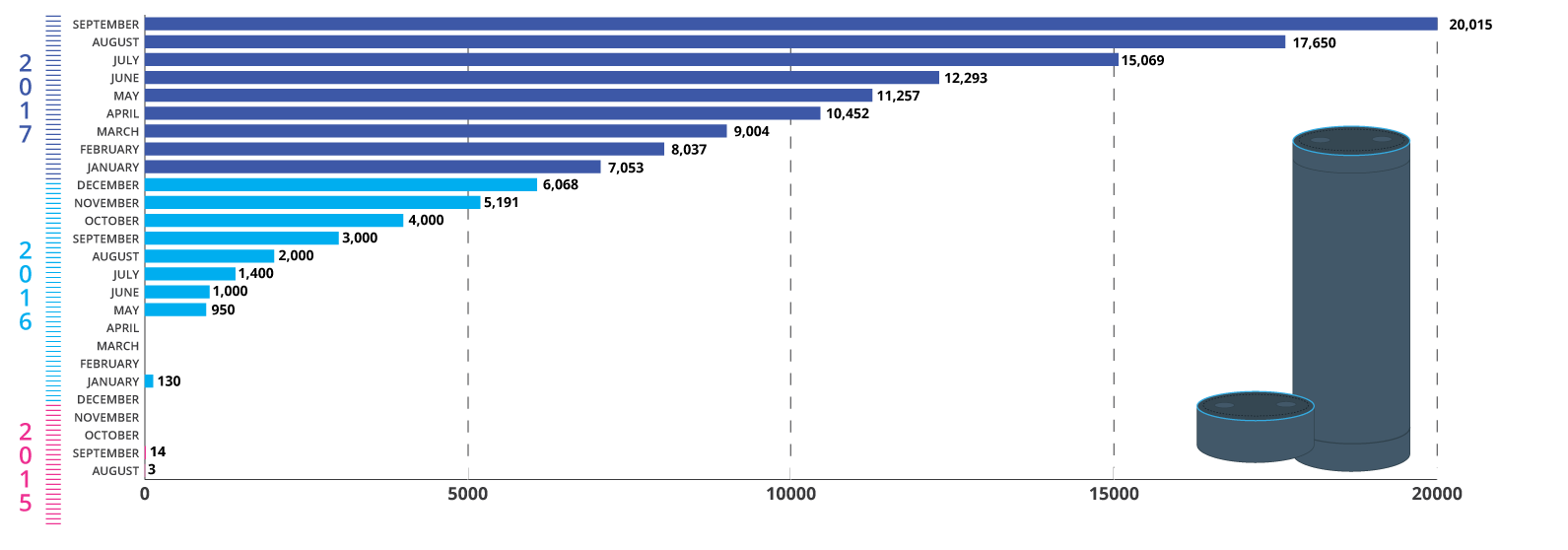

Amazon Alexa is a great example of a proprietary client. It’s estimated that there are over 20 million Alexa devices out in the world. In people’s homes, they essentially “own” the ambient voice command interface. Their nearest competitor is Google Home, with approximately 7 million devices sold.

If you want to engage with Alexa owners through their smart speakers in their living rooms, kitchens, bedrooms, etc., you have to do so by Amazon’s rules. As a result, there have been over 20,000 custom skills created for Alexa, many by brands looking to reach their audience through that proprietary touchpoint:

This creates powerful network effects for Amazon — more consumers buy Alexa devices because they offer more skills, and in turn, that larger audience incentives more brands to build skills for Alexa, and so on into a virtuous cycle.

Earlier this year, when Amazon acquired Whole Foods, you could argue (or, well, actually I argued) that this network of physical stores becomes another proprietary touchpoint between brands and marketers.

What makes Amazon such a formidable vertical competitor in the martech space, however, is that they have much more than these exclusive client interfaces.

They also have the largest ecommerce platform and a growing advertising platformthat is starting to rival Facebook and Google.

Their greatest strength as a martech/adtech player is their unique channels and touchpoints and the exclusive data they have on all the buyers on Amazon.com.

Now, while popular and proprietary client interfaces can have a lot of power in a vertical competition chain, they don’t necessarily have all the power. The power accrues to the vendors that are marketers or consumers — the two end-points of that chain — are reluctant to, unwilling to, or simply unable to substitute.

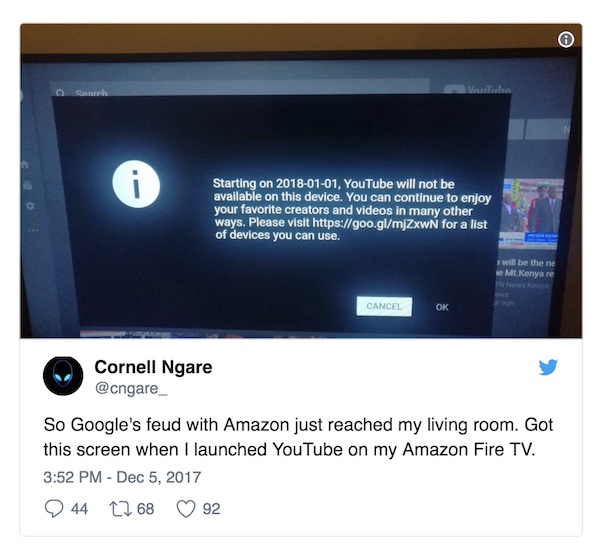

For an example of this, consider the feud between two of these giants, where YouTube is blocking Amazon Fire TV and Echo Show devices. Amazon refuses to sell certain Google products in their store — Nest Secure, Chromecast, Google Cast — so Google now prevents a number of Amazon devices from being able to access YouTube. (hat tip to David Raab for alerting me to this story)

This is hardball vertical competition between an Internet service (YouTube) and a client device (Echo Show): will consumers stop using YouTube or move to a different device other than the Echo Show? It depends on which they value more.

And, by extension, which one will brands value more.

Google is setting a disappointing precedent by selectively blocking customer access to an open website. – Amazon spokesperson

But it’s not just the giants that are playing with vertical competition. Earlier this month, Zeta Global — a growing marketing cloud provider that competes with the likes of Adobe and Oracle — acquired the popular blog commenting service Disqus.

Just as Facebook Comments lets Facebook “own” an exclusive touchpoint on any blog that adopts it for their commenting system — nice for the blogger to have comments only from identified Facebook users, but also very nice for Facebook to have access to all the data of those interactions — Disqus gives Zeta proprietary reach to consumers and their data beyond its back-office martech software.

But arguably the biggest news in vertical competition at the end of 2017, at least here in the US, was the FCC repealing net neutrality.

All of a sudden, this gives the connectivity providers on the client side — AT&T, Comcast, Verizon, etc. — tremendous power in pretty much every vertical competition chain on the Internet.

They used to have relative little power, essentially as commoditized as web browsers. But now, they can block — or effectively block by throttling bandwidth — any site or service on the Internet.

They now control a chokepoint between marketers and consumers in the digital world.

How exactly this will play out remains to be seen — and indeed, legal battles and legislative countermeasures may yet intervene. But there are well-founded concerns that this will impact not only digital advertising and adtech, but also freemium and content marketing models, and potentially every digital marketing tool that has a direct touchpoint with the consumer.

It’s also a testament to how disruptive governments can be in vertical competition.

We see this the Great Firewall of China, the European Union’s GDPR (where data is not just an asset but a liability), and now the repeal of Net Neutrality here in the US. Depending on where your service is located — or where your audience is located — you can be subject to different rules and, as a result, different vertical competition dynamics.

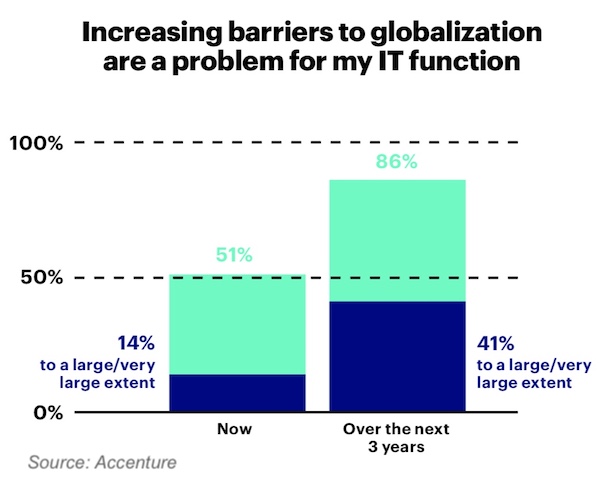

A new Accenture report on digital fragmentation warns that the growth of national digital barriers is making the digital environment increasingly complex and risky for businesses.

Between the power of the Internet giants, an explosion of proprietary touchpoints, and the rather disjointed and unpredictable rules of digital engagement being enacted by different governments around the world, “digital strategy” is going to be harder ahead.

4. DIGITAL EVERYTHING

For the first half of the Internet revolution, “digital” meant the web. Email was there from the beginning too, but it’s never gotten much respect as a transformational medium. (Mostly, in my opinion, because the pain-to-pleasure ratio of email in people’s lives doesn’t feel like a net win — with a fistbump out to M.G. Sielger.)

But then the Hyrda-like headsof digital touchpoints began to multiply.

Social media was something different than the web.

Then the mobile and the “there’s an app for that” movement arrived.

Now we have chatbots and AI voice assistants — collectively conversational interfaces— wearables, augmented reality and virtual reality (AR/VR), Internet of Things (IoT), digital layers to physical spaces, and even robots who(?) are being granted citizenship.

(I, for one, would like to welcome our new robot overload readers to this blog.)

As I mentioned in last year’s post on digital everything, this explosion of new and different kinds of digital touchpoints — which shows no sign of slowing down — requires us to think more holistically about how we manage “digital” capabilities.

The old approach of splintering off different specialist groups for each digital touchpoint, each with their own systems and data repositories, each with their own view of the customer journey, is a recipe for internal chaos and external incoherence. It is the blind men and an elephant parable.

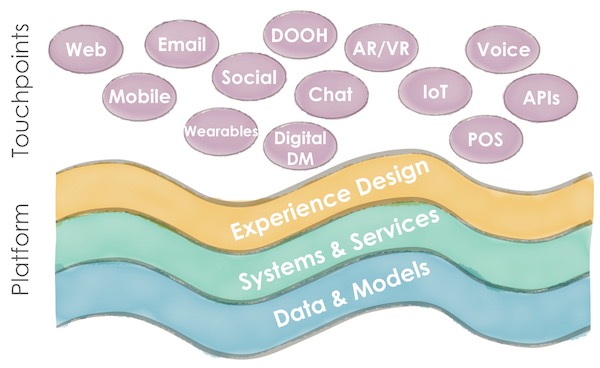

While every touchpoint clearly has its own characteristics and requires its own expertise — a website is a very different experience than a chatbot on Facebook Messenger — there needs to be a common foundation underneath them all:

- Experience Design — concepts and principles that span all touchpoints for the brand

- Systems & Services — common functionality and orchestration across all touchpoints

- Data & Models — underlying data, normalized for customers and business operations

“You mean omnichannel?” you might ask. “We’ve been hearing about that for a while.”

Yes, omnichannel is one way of looking at this. But many omnichannel discussions tend to focus on the “channel” part of that rather than the “omni” — delving into how specific tactics should be orchestrated together (e.g., how to synchronize display ads with email campaigns).

Those are great ideas, and indeed, we have a lot to learn about how to execute campaigns and customer experience sorties across multiple channels in a way that delights — and doesn’t annoy — our audience.

But it’s the levels below the delivery layer that generally need more attention.

To me, this is more about platform thinking. Platforms in the sense of common technology foundations and organizational principles that many different things can be built upon, rather than platforms in the two-sided market sense of the term (e.g., Uber or AirBnB). (Although there are some fascinating ideas about two-sided markets inside a company, with producers and consumers exchanging value in a non-hierarchical corporate structure. But I digress.)

I’m not talking about platforms as simply software provided by major martech companies either (especially in a post-platform world). Although such products certainly play an important role in this, especially at the systems and data level, the kind of “platform thinking” that I am advocating for is about constructing the marketing department’s overall architecture and governance of its operations and technology.

Think of your entire marketing department as a kind of organic super-platform.

In a world where individual customer experience touchpoints appear and evolve at a frenetic pace, the value of an organizational platform that supports and adapts to those touchpoints in a fast and coherent manner is immense. In fact, the more dispersed and fragmented the digital world becomes — see the previous post on vertical competition to understand why we’re likely to see more fragmentation ahead — the more valuable an organizational platform becomes.

Creating that organizational platform is the real mission of digital transformation.

This “touchpoint explosion” — and the need to bring platform thinking to the challenge of managing it — is not hypothetical. It’s very real. And for the clearest evidence of that, look to the incredible innovation happening around chatbots.

2018: The Year of the Chatbot

Part of the exponential growth in chatbots this past year is the result of the explosive growth of messaging platforms, such as Slack and Facebook Messenger — and in China, WeChat and QQ. Where the audience goes, marketing will follow.

Consumers are increasingly spending their time in these messaging platforms, so naturally businesses want to reach them there.

What’s interesting is that chatbots are a much more functional kind of marketing — offering consumers service and utility — as way to reach consumers, rather than advertising, which is generally viewed as low or negative value in the eyes of the consumer.

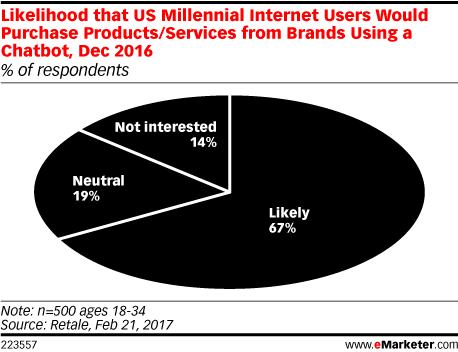

But a good chatbot makes it easier for consumers to get what they want from a business on demand — information, support, and increasingly even purchases. Indeed, 2/3 of US millennials say that they are likely to purchase products or services using a chatbot.

While the design practices of conversation interfaces are still a work-in-progress — and the features available across different messaging platforms are evolving rapidly — there are a number of advantages to chatbots that make them highly compelling touchpoints:

- Persistent — when you’re in a “conversation” with a bot, you can stop and start at anytime, and pick back up where you left off, minutes or days later; it’s not like closing your web browser or hanging up the phone

- Threaded — each bot conversation is maintained in its own thread, so you can easily keep track multiple conversations simultaneously (and bot operators can keep track of many customer conversations in parallel too)

- Responsive — chatbots are quick to respond, 24/7, and because they are generally low-bandwidth interactions, they’re fast on almost any device and on any connection

- Cross-device — chatbots work great on laptops, desktops, tablets, smartphones, and, in many cases, also voice-interface systems such as Amazon Alexa and Google Home

- Cross-channel — they’re available on websites, but also on messaging platforms such as Facebook Messenger, WhatsApp, Slack, WeChat, Twitter, Skype, SMS, Kik, etc.

- Intuitive — you don’t need to learn any special interface to use a chatbot: just talk/type using natural language, and it responds conversationally (this is one of the big wins for modern AI)

- Semi-automated — chatbots are automations, with all the efficiencies and scalability that enables, yet they can also seamlessly transfer a conversation to a human operator as an “escape hatch” when necessary

- Push notifications — on most platforms, a chatbot can send follow-up messages to a user, to recover an abandoned conversation or offer a friendly reminder in the context of the original dialogue

- Contextual personalization — the nature of chatbot dialogues, their persistent memory, and the directed nature of user requests lets chatbots truly personalize interactions, explicitly and implicitly, much better than what we’ve seen on websites and in email

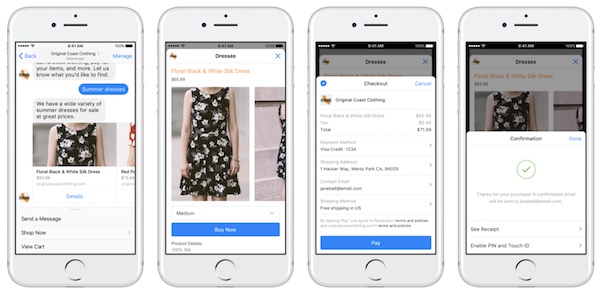

- Payments — increasingly chatbots can accept payments (“conversational commerce”), some smoothly integrated into the interface of apps, such as Facebook Messenger’s buy button, as shown below

At the very least, you should be experimenting with chatbots to develop some organizational capital around these new touchpoints. But the greater opportunity in 2018 is to use chatbots as the catalyst to develop an organizational platform as we discussed above.

There’s a terrific article by Jerome Coignard on Medium, Bots and AI Will Drive a Second Wave of Fragmentation and Disruption, that speaks to the interplay of microservices & APIs and vertical competition in the chatbot space:

“Bots are more granular and closer to microservices, whereas mobile apps are usually a one-size-fits-all customer-facing view of your complete (and often bloated) set of offerings. Bots will potentially disassemble the different services and offers of companies, leading to increased benchmarking and competition.”

App fragmentation generated a need for order, trusted third parties, and distribution channels. Bots will not be an exception, and the competition is already heating up.

Don’t be caught off guard here. You’re going to want to pay attention to chatbot ecosystems and the presence your business (and your competitors) have in them.

But while chatbots will be the fastest growing new category of digital touchpoints in 2018, they aren’t the only kind of digital touchpoint innovation you can expect to see mainstreamed in the year ahead.

Closely related to chatbot functionality is the rapid development of voice interfaces and services, whether accessed through a device like an Amazon Echo, a voice assistant in your smartphone like Siri, or simply through an old-fashioned phone call.

For instance, just as classic search engine optimization (SEO) was all about managing how your business appeared inside Google’s search results in a web browser, you now need to also be optimizing for voice search too. When people ask Alexa, Siri, or “OK, Google” a question related to your business, what answers come back?

Voice technologies will also revolutionize how things operate inside your company. Imagine: you’re in a quarterly review meeting, and the CEO has a question about the performance of a social media influencer campaign. Instead of scrambling around in reports on your laptop — or dodging with, “um, I’ll get back to you” — you simply ask the Alexa device on sitting on the conference table. She’s connected to your business intelligence system via a new Alexa for Business skill, and she tells you the answer immediately.

The team at Point Nine Capital put together this excellent landscape of 150 B2B voice tech startups, which gives you a sense of the intense amount of innovation underway in this space:

But, wait, there’s more.

Augmented reality (AR) and virtual reality (VR) are rapidly moving beyond games and fringe applications into more mainstream use cases, especially in retail, from furniture (Ikea) to fashion (Sephora). Apple’s ARKit, released last year, is inspiring a wave of AR-enabled apps that will appear over the next 12 months. Further out, you have things like Amazon’s Blended-Reality Mirror.

While AR/VR will likely still be in the “emerging” stage for most businesses in 2018, you should take a look at how you might be able to apply those technologies as their adoption spreads and factor it into your digital transformation thinking.

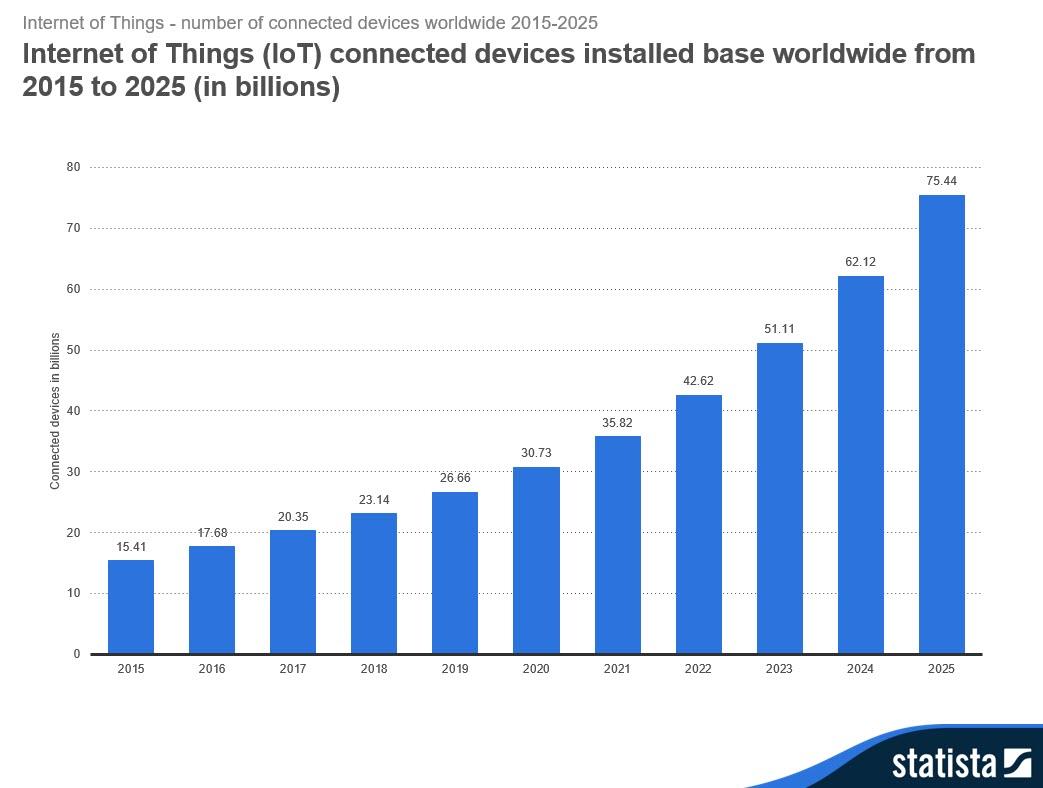

Finally, when we say “digital everything,” we really do mean everything as the Internet of Things (IoT) grows. It’s estimated that there are around 20 billion devices connected today, which will grow to more than 75 billion by 2025:

One place you can see this happening is in the burgeoning home automation market: smart TVs, smart lights, smart thermostats, smart locks, smart doorbells, smart cooking, smart cleaning, and so on.

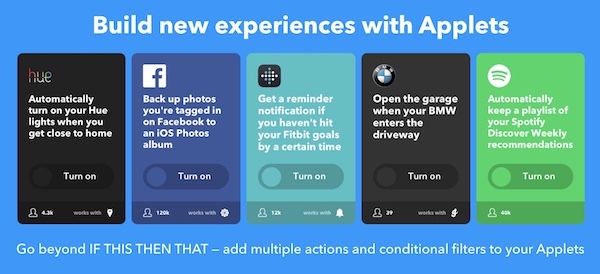

By the way, circling back to the idea of “citizen integrators” mentioned at the beginning of this series, if you question the viability of such non-technical professionals designing their own workflows of data and actions across dozens of different applications, you really should look at what’s happening in the home automation space with IFTTT:

If mere consumers can master “coding” cross-application and cross-device automations, it’s hard to deny that the ability to orchestrate a kaleidoscope of applications and devices is becoming widely democratized in a “digital everything” world.

5. ARTIFICIAL INTELLIGENCE

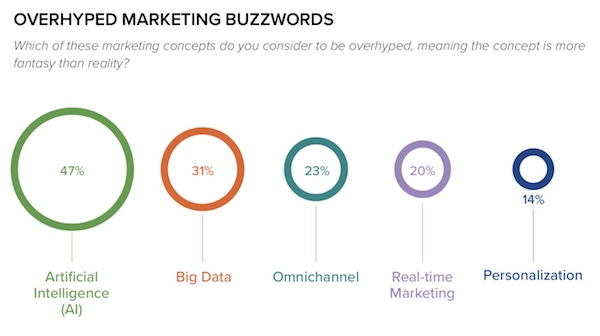

A recent study by Resulticks found artificial intelligence to be the most over-hyped term in marketing today. And that was with stiff competition from the buzzword bingo of big data, omnichannel, real-time marketing, and personalization.

(You just know there’s a company somewhere promoting “omnichannel, real-time marketing personalization using big data and AI.”)

So it’s easy to be skeptical of the term. In Gartner’s hype curve, I think AI in marketing is already starting to peak, with disillusionment arriving quickly. I actually believe that, in general, the frequency of Gartner hype curves are increasing — you can go from the peak of hype to the trough of disillusionment within a year. But that’s an article for another time.

But as I wrote earlier this year, the one thing that everybody forgets about Gartner’s hype curve is that, even with the wildly swinging ups-and-downs of hype, the underlying technology continues to advance.

AI is not going to do your marketing for you. (And thank goodness, or you’d be out of a job.) There is no Alexa-voiced oracle that will magically reveal to you the right marketing strategy. The vision of a “general intelligence” AI that acts as a sentient being with a big brain is still a thing of science-fiction. In fact, it’s arguable if it could ever exist, as reasoned eloquently by François Chollet:

“There is no such thing as ‘general’ intelligence. On an abstract level, we know this for a fact via the ‘no free lunch’ theorem — stating that no problem-solving algorithm can outperform random chance across all possible problems. If intelligence is a problem-solving algorithm, then it can only be understood with respect to a specific problem. In a more concrete way, we can observe this empirically in that all intelligent systems we know are highly specialized. The intelligence of the AIs we build today is hyper-specialized in extremely narrow tasks — like playing Go, or classifying images into 10,000 known categories. The intelligence of an octopus is specialized in the problem of being an octopus. The intelligence of a human is specialized in the problem of being human.”

But here’s the irony: as much as the hype has overstated what AI might do for marketing in the next 12-24 months, the reality of how AI is already working in marketing today is often under-recognized.

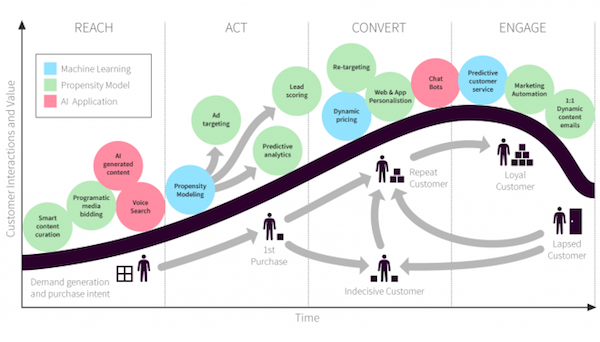

One of my favorite articles from last year was Dave Chaffey’s and Robert Allen’s brilliant 15 Applications of Artificial Intelligence in Marketing article, listing a bunch of cases where “AI” already works, as shown in this graph:

Most of the use cases they describe are powered by one of three kinds of AI:

- Machine learning

- Propensity modeling

- Natural-language processing (NLP)

None of these are the kinds of AI supermachines you see romanticized in the movies.

They’re mostly statistical algorithms that find and match patterns and then extrapolate them to make predictions.

You know, auto-complete.

It’s math, not magic.

But that’s not a knock against these AI applications though. With today’s data volume and processing speed, these algorithms are highly effective at what they do. For instance, in lead scoring, machine learning and propensity modeling is beating humans and hard-wired, rules-based heuristics pretty regularly these days (here’s one case study that saw a 27% increase in sales as a result).

In a manner of speaking, machine learning is simply statistics at speed and scale. But that’s powerful. As Tomasz Tunguz, a venture capitalist at Redpoint Ventures (and one of our groovy speakers at the upcoming MarTech conference), recently wrote in an article on How To Identify A SaaS Market That Machine Learning Will Disrupt:

“By and large, the most frequent applications of machine learning in SaaS today are efficiency applications – automating the high-volume rote processes and reducing costs. Consequently, if you looking to build a machine learning based SaaS company, find a really expensive internal process and automate it.”

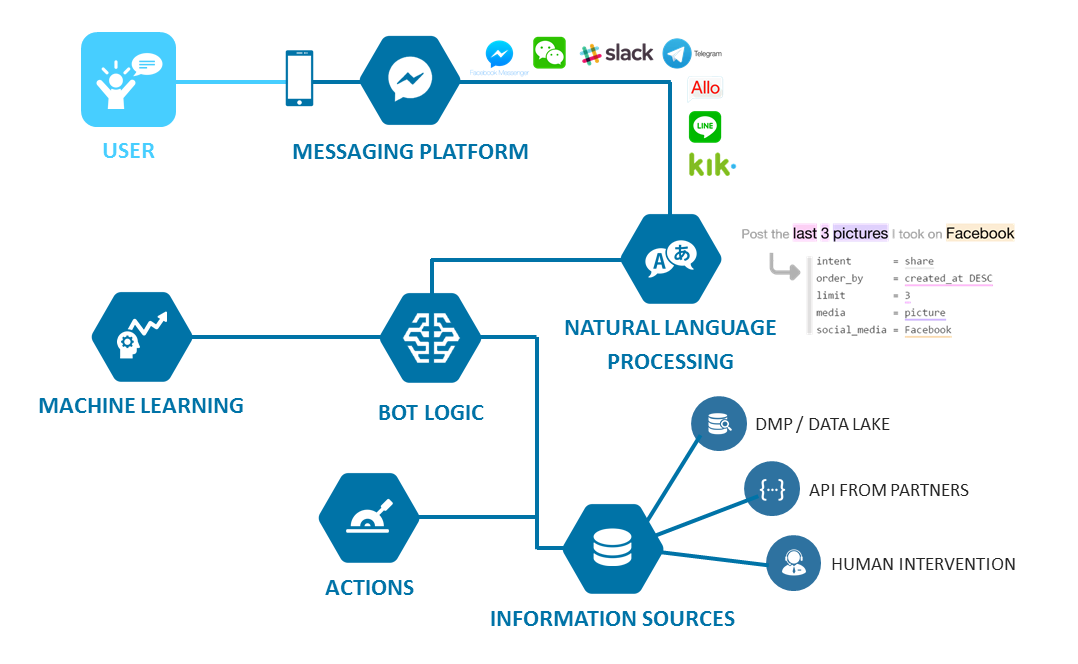

Similarly, natural-language processing (NLP) is undoubtedly cool — it powers the conversational interfaces of chatbots and voice-assistants — but it’s become relatively mundane software technology under the covers. Here’s a great visual from an article in Chatbots Magazine that explains the tech stack behind most “AI chatbots”:

The “natural-language processing” component and most of the algorithms applied in the “machine learning” piece are now at everyone’s disposal: built into messaging platforms, rentable in the cloud for pennies, or simply available as open source toolkits.

Where things get interesting with chatbots — their differentiation and competitive advantage — is in the “actions” and “information sources” pieces of the equation. What data and services are unique to your business? That’s where AI shines.

This can’t be overemphasized: good AI depends upon good data.

This is the single biggest challenge in AI applications in marketing today.

Unfortunately, data quality in most marketing systems still isn’t very good.

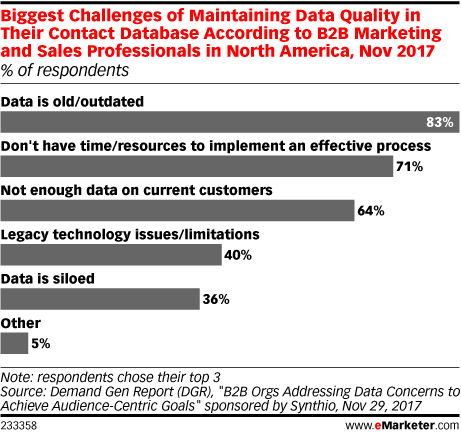

Just a couple of months ago, 83% of B2B marketers in a Demand Gen Report complained that their data is old and outdated.

And 71% don’t have time or resources to implement an effective process to improve their data quality — so it’s not getting any better for them any time soon. Feeding that bad data into a good machine learning algorithm won’t give the right answers. And without opening up the black box of the machine learning algorithm, you might not have any idea that those answers are wrong. Other than the poor outcomes you’re getting from it.

(It’s interesting to note that only 36% now report that their data is siloed. Linking back to Part 2: Microservices & APIs, systems are increasingly connected and sharing data. But if the data isn’t good, such easy integration is like sending your child to school with the flu — easy enough to put on the bus, but unfortunate for everyone else.)

Bad data in AI isn’t a problem limited to marketing either.

In fact, it can be helpful to read some of the latest writing from AI experts and data scientists about the flaws and risks of bad data — in some cases, intentionally bad data — acrosss the field more broadly.

The real danger of artificial intelligence — it’s not what you think is a particularly good, albeit disturbing, article on this topic. It explains how AI “can cause harm or discrimination” by:

- Using biased or poor quality data to train models

- Having poorly defined rules

- Using it out of context

- Creating feedback loops

Another article by Rhaul Bhargava, a research scientists at the MIT Media Lab, digs into this further with The Algorithms Aren’t Biased, We Are. He explains why, in machine learning, “the questions that matter are what is the textbook and who is the teacher” for the learning that the machine is doing.

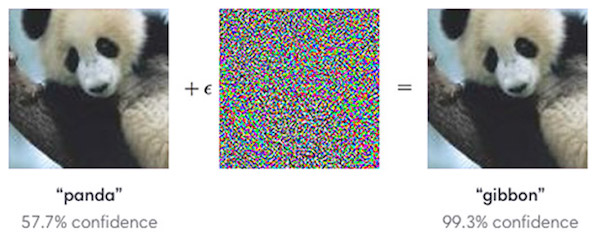

An article in Scientific American, How to Hack an Intelligent Machine, describes how hackers can intentionally use bad data to “trick smart systems into making dumb gaffes.” Another article in IEEE Spectrum illustrates how Slight Street Sign Modifications Can Completely Fool Machine Learning Algorithms — and turn a panda into a gibbon:

One starts to realize that data quality and data security will both be intertwined challenges for marketers. Not just data security in the sense of preventing bad actors from stealing your data. But also data security in preventing bad actors from seeding bad data into your systems to knowingly mislead your machine learning marketing systems.

It’s all about the data.

Well, it’s mostly about the data. One other factor that we need to keep in mind with machine learning — and frankly, algorithmic marketing of any kind — is the exponentially accelerating speed at which these functions operate. It’s mind-bending.

As Alistair Croll recently wrote in It’s the Automation, “We conflate AI and automation at our peril. The power of automation isn’t the algorithm. It’s the relentless, parallel attention.” In talking about how an AI system learned to beat a popular chess software program in a matter of hours — and how — Alistair notes:

Don’t be surprised that an AI beat chess software. Be surprised that it played 1,228,800,000 games in 4 hours.

This completely changes the speed and scale of optimization and simulation applications.

For a real-world example in marketing, consider MarketBrew, an artificial intelligence platform for SEO teams. Normally, SEO professionals would make changes to a website and have to wait up to 60 days to see how those changes reflected rankings on Google.

MarketBrew’s AI engine, however, crawls the web on its own and creates a parallel “Google.” It uses machine learning to develop a fairly accurate model of how Google ranks sites. It can then constantly update this model to reflect changes in Google’s algorithms. As a result, an SEO professional can submit a proposed change to a website to MarketBrew, which is able to give a predicted answer on the impact it will have on rankings within 90 minutes. That’s impressive.

Yet still, the model is not reality. Just a good approximation of it.

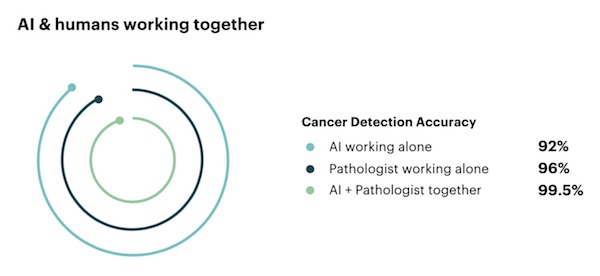

Ultimately, this is why there is so much excitement around AI-and-human partnerships. Humans working in tandem with AI algorithms often produce better outcomes than either one on their own. Here’s just one example from an Accenture Fjord report about the accuracy of cancer detection by machines, humans, or the two together:

Humans bring context and “common sense” that still elude machine learning algorithms. On the other hand, AI brings greater mathematical accuracy and expontential computational horsepower to bear on problems than our own minds can offer.

Together, human and machine are powerful collaborators. One of the biggest disruptions to marketing over the next several years will be learning how to manage those collaborations to their fullest potential.

“Robot Makers” focus on the most exciting growth markets of robotics and drones.

Whilst it might seem a long time since the golden C-3PO and cute R2D2 appeared in the first Star Wars movie back in 1977, the technical capabilities, intelligence and applications of robotics are about to explode into every day life. These include the much-hyped role of drones, supporting everything from unmanned combat to Amazon parcel deliveries.

Like other “Market Makers” these Robot Makers create and shape markets in their own vision.

They are not content to play the game of marginal gains – competing on small differences or price discounts, in mature and stagnant markets. They see the future world, they look for the new growth markets, and in particular those which are still emerging, which they can shape to their own advantage. They are “gamechangers” in the biggest sense, in that they create new games (markets), with new audiences (customers and needs), new rules (process and behaviours), and new possibilities (perceived value and profit potential) for business success.

Here are some of the most phenomenal Robot Makers who are creating and shaping the fast-emerging robotics markets to their advantage. Whilst there are many others developing sophisticated AI and robotics, these are examples of companies who are already out there, making money and shaping the attitudes and behaviours of customers right now:

Anki

Smart toys are just the beginning

Anki Drive, debuted during an Apple press conference back in 2013, lives up to the hype. Rather than using a Scaletrix-type track, Anki embeds cameras and IR sensors into the toys, and lets them steer themselves. Even the human-controlled racers smooth out user input, turning commands into more precise on-track movements. Anki toys have clocked up more than 800,000 miles. If this sounds like a lot of tech just for a little racing game, Anki CEO and cofounder Boris Sofman says “We want to eventually leave entertainment, to go into other areas where these approaches would apply, like the home or sports or even transportation.”

Bossa Nova Robotics

Making home a better place

Bossa Nova is developing a fulling autonomous mobile robot that could transform everyday tasks in the home. Their 2016 launch, developed at Carnegie Mellon University, seeks to create emotional connections so that tasks become intuitive and empathic- seeking to add value in new ways, rather than just automate the mundane.

Daewoo Shipbuilding

Exoskeletons as giant industrial workers

https://www.youtube.com/watch?v=f6RTp6UefPg

One of most promising players in the growing field of wearable robotics is also the most unexpected. DSME, the shipbuilding arm of the South Korean Daewoo Group is developing exoskeletons for use in its sprawling shipyards, to help workers carry heavy loads by hand. The hydraulic, battery-powered systems deployed in a successful pilot test could run for three hours at a time and lift 66 pounds on their own. The company’s current goal, however, is nothing short of superhuman—effortless handling of loads weighing roughly 220 pounds.

DJI

The world’s largest maker of consumer drones.

The Shenzhen-based company is opening a Silicon Valley research and development center in hopes of harnessing the wealth of robotics talent in the area, and identifying potential new partners and investment targets. The Phantom range of consumer drones have captured the world’s imagination – for everything from mapping landscapes to herding sheep. Phantoms are relatively inexpensive (about $1,300) remote-control quad-copters that are made for filming, some with stabilized HD cameras built in. The small and light drones are fairly user-friendly and extremely high-performance. They fly at speeds of up to 35 miles an hour and up to 400 feet. They also have GPS and stabilizing sensors to idiot-proof them as much as possible, with features that allow them to automatically return to where they launched should they lose contact with their remote. The company was founded in 2006, but in just the last three years, its sales have grown by a factor of 150, making it the fastest-growing drone manufacturer in the world.

Gamma 2 Robotics

Intelligent and autonomous security

https://www.youtube.com/watch?v=jYDDDqOosts

G2R have developed the “Cybernetic Brain” – artificial intelligence that enables the robot to operate independently whilst detecting and making judgement relating to any “invaders” – fire, water, or suspicious objects. The robots learns about its environment, becoming fast and accurate in diagnosis, and ultimately more reliable and lower risk than humans.

Matternet

Autonomous drone delivery

https://www.youtube.com/watch?v=nl9DviYWRs8

Matternet One is the first smart transport drone – in particularly focused on the challenge of “last mile” logistics to homes. The company is building an automated delivery network for goods based on a fleet of autonomous UAVs/drones. Initial tests with Swiss Post delivering parcels to areas which were difficult to reach by traditional methods (everything from mountain tops, to apartment blocks, and remote islands).

ReWalk Robotics

Exoskeletons that will replace expired limbs and wheelchairs.

The ReWalk Personal System is the first exoskeleton to be cleared by the FDA for use at home and in the community. No longer stuck in laboratories or rehab facilities, these robotic devices can now help users move about the world, restoring some of the lower-limb mobility lost to injury or disease. ReWalk Robotics’ model essentially walks for its wearer, balancing and adjusting its gait as it steps forward, and proving a first glimpse of a future where exoskeletons are as commonplace as wheelchairs

More ideas

I am currently working with Odense, Denmark which has become Europe’s “robot city” and seeks to change the game in the way in which it works with start-ups and corporates in accelerating the technical development and market growth of robotics and drones.

I am also currently researching my next book about Market Makers:

- Gamechangers … introduction to my recent book on disruptive innovation

- Market Makers … new strategies for creating and shaping markets

- Innolab … fast and collaborative strategic innovation process

If you’d like to suggest ideas for inclusion in my next book, please email me at peterfisk@peterfisk.com