To understand OpenAI, you have to start with intent. This is not a company that exists merely to ship software faster than competitors or extract short-term value from a hot technology cycle. Its founding purpose – to ensure AI advances in ways that benefit humanity – is not a slogan pinned to the wall, but a living constraint that shapes decisions, priorities and trade-offs.

That sense of mission permeates the organisation. People do not join OpenAI simply to work on AI; they join to work on questions that feel consequential. What should intelligence become? Who should it serve? How quickly should it move, and under what guardrails? These questions are not peripheral. They sit at the centre of everyday conversations, from research choices to product launches.

The result is a workplace that feels less like a conventional technology firm and more like a high-velocity research institution operating inside a global platform business. It is ambitious, demanding and often uncomfortable — but rarely complacent.

A global mindset, not a Californian bubble

OpenAI’s internal reality reflects the global nature of the systems it builds. Walk through its offices or join a virtual meeting and you encounter a mix of languages, disciplines and worldviews. Researchers trained in physics debate designers focused on human behaviour. Engineers with roots in Asia, Europe and Africa exchange ideas with ethicists, policy thinkers and product leaders.

This diversity is not ornamental. It is essential. Building general-purpose intelligence demands perspectives that stretch beyond code and compute. The organisation actively values difference — not as a tick-box exercise, but because the complexity of the challenge requires it.

The working style mirrors this diversity. Collaboration is intense and cross-functional by default. Teams form around problems rather than rigid hierarchies, and roles flex as ideas evolve. Titles matter far less than contribution. What counts is the quality of thinking, the clarity of argument and the willingness to challenge assumptions — including those of leadership.

OpenAI is based in San Francisco, California, with its main offices are in the Mission District, which is where most leadership, research, engineering and product teams are based.

However it operates as a distributed organisation. Employees work from other parts of the United States. There are team members across Europe and other regions Remote and hybrid working is common, especially for research and engineering roles So while San Francisco is the centre of gravity, OpenAI functions as a globally connected organisation, reflecting the worldwide impact of the technologies it builds.

Sam Altman and his team

Sam Altman’s influence on OpenAI is less about charismatic pronouncements and more about how he frames trade-offs. He operates as a systems thinker rather than a traditional CEO — someone preoccupied with second- and third-order effects, long-term consequences, and the uncomfortable edges of progress. His leadership style blends ambition with restraint: pushing the organisation to move faster than almost anyone else in the field, while simultaneously insisting that safety, alignment and governance cannot be treated as afterthoughts.

Altman is known internally for asking deceptively simple questions that cut to the heart of complex debates. What happens if this scales globally? Who is excluded? What risks compound over time? These questions shape not just product decisions, but the cadence at which OpenAI releases capabilities and forms partnerships. He is willing to pause momentum when risks feel unresolved — a discipline that is rare in hyper-competitive technology environments.

Crucially, Altman does not operate alone. OpenAI’s leadership team is deliberately plural. Senior figures across research, engineering, policy, safety, product and partnerships hold real power and are encouraged to disagree openly. This creates a leadership dynamic that is more collegiate than hierarchical, and often intellectually demanding. Decisions are debated rigorously, sometimes painfully, before alignment is reached.

The broader executive team reflects the organisation’s hybrid identity: part research institution, part global platform company, part public-interest steward. Technical leaders bring academic depth and frontier expertise; operational leaders focus on scaling systems responsibly; policy and safety leaders ensure that societal implications are surfaced early rather than retrofitted later.

Together, this leadership group functions less like a command structure and more like a deliberative engine — designed to balance speed with reflection, confidence with doubt, and commercial reality with ethical obligation. It is an imperfect, evolving model, but one that mirrors OpenAI’s central challenge: advancing rapidly without losing sight of why it exists in the first place.

Strategy at OpenAI … vision, horizons and agility

Strategically, OpenAI operates on multiple time horizons at once. There is the long game: the pursuit of increasingly capable, general intelligence aligned with human values. There is the medium term: translating breakthroughs into usable tools that create value for individuals, organisations and society. And there is the short term: deciding what to build next, what to release, and what to delay or abandon.

What distinguishes OpenAI’s strategy is not a fixed roadmap, but a commitment to directional clarity combined with tactical agility. The destination is clear. The route is deliberately adaptive.

Rather than locking itself into multi-year plans, the organisation treats strategy as a living system. Choices are revisited as evidence changes. New capabilities reshape priorities. Risks are reassessed continuously. This allows OpenAI to move at speed without drifting into chaos — a balance many organisations struggle to achieve.

Innovation at OpenAI … ideas, systems and portfolios

Innovation at OpenAI is not housed in a lab at the edge of the organisation; it is the organisation. Experimentation is constant and expected. Ideas are tested early, often in imperfect form, then refined or discarded quickly.

Crucially, innovation is managed as a portfolio, not a single bet. Some work is incremental, improving existing models and products. Other efforts are exploratory, pushing into unknown territory with no guarantee of near-term return. This mix allows OpenAI to learn continuously while still delivering tangible outcomes.

Partnerships play a vital role. OpenAI does not attempt to build everything alone. It collaborates with universities, enterprises, governments and technology partners, recognising that ecosystems scale faster than silos. Internally, knowledge is shared deliberately; breakthroughs are documented and reused, not hoarded.

Scaling, when it happens, is intentional. Experiments are not celebrated simply for novelty, but for their ability to move from insight to impact.

Leadership at OpenAI … catalysts, collaborators and culture

Leadership at OpenAI is notably understated. Authority comes less from position and more from judgment. Leaders are expected to be deeply informed, forward-looking and comfortable with uncertainty. They set direction, but they also listen — and they expect to be challenged.

This creates a culture of constructive tension. People are encouraged to question, debate and disagree, provided they do so thoughtfully and in service of better outcomes. Courage and curiosity are valued more than certainty.

The absence of rigid hierarchy speeds decision-making and empowers teams, but it also demands maturity. Individuals are expected to take responsibility, not wait for instruction. Leadership is distributed — a skill to be practised, not a title to be granted.

Culture at OpenAI … speed, ambiguity and learning

Working at OpenAI is not easy. The pace is intense. The expectations are high. Ambiguity is constant. Decisions are often made with incomplete information and real consequences.

Yet for many, this is precisely the appeal. The work feels meaningful. The problems are hard. The learning curve is steep. There is a sense of participating in something that may shape the future, not just respond to it.

The culture rewards substance over optics, progress over perfection, and long-term impact over short-term applause. That does not suit everyone — and OpenAI does not pretend otherwise.

Performance at OpenAI … trust, impact and long-term value

OpenAI’s approach to performance reflects its broader philosophy. Financial sustainability matters — it enables independence and scale — but it is not the sole measure of success. Value is assessed over the long term, including societal impact, trust, safety and ecosystem health.

Relationships with partners and investors are framed around shared horizons, not transactional wins. The organisation is explicit about trade-offs, risks and constraints, preferring credibility over hype. In an era obsessed with speed and valuation, this long-term lens is both rare and instructive.

What can we learn from OpenAI?

5 things you can take away from Sam Altman and his team …

1. Strategy: Direction without rigidity

Purpose is not decoration; it is a strategic filter. Be clear about the future you are trying to create, make explicit choices about where to play and where not to, and treat strategy as a dynamic system rather than a static plan. Agility works best when anchored in conviction.

2. Innovation: Build a portfolio, not a pipeline

Innovation thrives when experimentation is normal, collaboration is easy and learning is fast. Manage innovation as a portfolio of bets — some safe, some bold — and design pathways to scale what works rather than celebrating ideas that never leave the lab.

3. Leadership: Flatten, look forward, stay curious

The most effective leaders today create clarity without control. They look ahead, invite challenge, and model learning. Authority should come from insight and integrity, not hierarchy. Courage and curiosity matter more than certainty.

4. Culture: Design for truth, not comfort

High-performing cultures allow disagreement, reward substance and tolerate discomfort in service of progress. Psychological safety does not mean avoiding tension; it means handling it well. Culture should enable honest thinking at speed.

5. Performance: Think in decades, not quarters

Sustainable value is built over time. Align investors, partners and teams around long-term outcomes. Measure what matters — trust, capability, resilience — not just what is easy to count. Performance is a system, not a scorecard.

Building the future

OpenAI is not a template to be copied wholesale. Its context is unique, and its challenges extreme. But its underlying principles — purpose with teeth, strategy with flexibility, innovation as a system, leadership without ego and performance measured over time — are profoundly relevant.

In a world of accelerating change, the most important lesson may be this: the future does not belong to the fastest organisations, but to those that can learn, adapt and act with intention — again and again.

In a world of dramatic change – from AI and robotics, to climate crisis and resource constraints, shifting consumer values and social expectation – the business imperative has shifted. Once the goal was efficiency: to do more with less. Then the narrative turned to sustainability and corporate social responsibility (CSR): reduce negative impact, comply with regulation, show you care. More recently, environmental, social and governance (ESG) frameworks have offered a mainstream rubric to investors and boards.

But today a deeper shift is underway: from “less bad” to “more good”. This is the domain of regenerative business models, companies that not only minimise harm, or reuse resources, but actively rebuild ecosystems, enrich communities, and embed purpose into the heart of their value creation. Regeneration is not a sideline—it becomes strategy.

Crucially, this shift is not merely moral or philanthropic. It is becoming commercial. Because in a world of increasing volatility, companies that embed resilience, long‑term value, stakeholder alignment and ecosystem thinking are more likely to thrive. Their intangible assets — brand trust, purpose alignment, supply‑chain partnerships, community goodwill — become the strategic differentiators. Regeneration and commercial success are not opposed; in many cases they are intertwined.

In this article we examine how leading European firms are walking this path. We explore their purpose and strategy, leadership and culture, business model and innovation, supply‑chain and ecosystem design, and financial and non‑financial performance. The cases illustrate how regeneration is more than a buzzword — it is a lens for business reinvention.

What do we mean by “regenerative”?

“Regenerative” is a difficult word in the corporate world, and has many interpretations. At one end sits compliance and efficiency; next comes sustainability and then circularity — strategies designed to reduce waste and reuse materials. Regeneration goes beyond: it aims actively to rebuild ecological systems and social capital. That means restoring soil health and biodiversity, rebuilding coastal and marine habitats, reversing carbon accumulation in the atmosphere by sequestering carbon in the ground and vegetation, and reweaving fair and resilient local economies. It’s not simply a product attribute; it is a systemic ambition encoded into corporate purpose, governance, investment, and metrics.

There are three distinctive features of regenerative business models:

-

Give more than take … business models and ecosystems, products and services, are designed so that, across their lifecycle, they return more social and environmental value than they extract.

-

Reinventing the way we work … companies partner with suppliers, communities and public actors to alter production systems (for instance, shifting commodity agriculture to regenerative farming practices).

-

Purpose and profit are equally important … structures and metrics (from ownership to capital allocation) are engineered so that long-term ecological and social outcomes are core to decision-making, not peripheral.

These criteria form the lens through which we explore a new mindset for business success.

Patagonia, of course, has long been held up as a trailblazer in this context. Yvon Chouinard’s business has show the way in conscious capitalism, showing the businesses can be platforms for good, creating a business model that looks beyond money making, and a brand as a community of people fighting for a bigger cause.

But what about some of the other companies around the world?

Europe’s Regenerative Leaders

Europe has become a hotbed of regenerative businesses over recent years, driven by social and political agendas, as well as an awakening among business leaders of a better way. No company, of course, is perfect; but each of the following companies show significant progress on their journey, combining ambition with practical transformation:

Acciona, Spain … regenerative infrastructure

Strategy:

Acciona has positioned itself at the forefront of regenerative infrastructure. Its business model integrates environmental and social value creation into construction, renewable energy, and water projects. The company’s master plan goes beyond reducing harm; it actively restores ecosystems and social capital. Climate mitigation, biodiversity recovery, circular construction, and water stewardship are embedded in each project, with an explicit goal of leaving a net-positive footprint on both natural and human systems.

Leadership:

Leadership at Acciona links executive remuneration and career progression directly to measurable sustainability targets. José Manuel Entrecanales and his team have cultivated a culture in which project managers and engineers consider ecological and social outcomes as integral to decision-making. Sustainability is treated not as compliance, but as a lens through which all operational and strategic choices are evaluated.

Innovation:

The company has pioneered low-carbon concrete, modular construction that allows for disassembly and reuse, and recycling of complex materials such as wind turbine blades. Nature-based solutions — including urban green corridors, pollinator habitats, and rewilded zones — are standard practice in large-scale infrastructure projects.

Ecosystem:

Acciona’s scale allows it to convene suppliers, local authorities, NGOs, and academic institutions in a shared agenda for regeneration. Supplier standards require low-emission materials and ethical sourcing, while urban development projects are designed to integrate biodiversity, local employment, and climate resilience.

Performance:

More than 90% of Acciona’s capital investments now align with the EU sustainable taxonomy. Renewable energy operations continue strong growth, and biodiversity indices show measurable gains across key project sites. Acciona demonstrates that infrastructure can generate ecological and social value alongside financial return.

Arket, Sweden … regenerative fashion

Strategy:

Part of the H&M Group, Arket differentiates itself through durable essentials for men, women, children, and home, combining minimalistic design with circularity. Its 2030 vision aims for fully sustainable sourcing and a circular product life cycle. Unlike conventional fashion brands, Arket measures success not by volume but by product longevity, reuse, and repairability, positioning sustainable consumption as central to its strategy.

Leadership:

Arket benefits from H&M’s global infrastructure but operates with a culture of transparency and accountability. Leadership incentivises teams to prioritise durability and traceability, promoting a mindset where design, materials, and supply chain choices are all scrutinised for environmental and social impact.

Innovation:

Arket’s circular innovations include children’s clothing rental, repair services, and mono-material garments designed for recycling. Regenerative fibres — organic cotton, Tencel, and recycled polyester — are standard, while low-impact dyes and sustainable packaging reduce the brand’s environmental footprint.

Ecosystem:

The brand leverages H&M’s supplier network to implement circularity at scale, working with textile recyclers, start-ups, and technology partners. Customer engagement campaigns educate consumers on care, repair, and reuse, effectively extending the life of products while reinforcing brand loyalty.

Performance:

Despite being relatively young, Arket has enhanced customer retention and brand value through sustainability-led differentiation. Its initiatives prepare the business for a market increasingly attentive to ethical consumption, while generating operational efficiencies from reduced returns and extended product lifespans.

BayWa, Germany … regenerative agriculture

Strategy:

BayWa AG combines agribusiness, renewable energy, and building materials under a regenerative framework. Its strategy focuses on sustainable crop production, carbon-smart farming, and energy efficiency. By integrating these sectors, BayWa decouples growth from environmental degradation while enhancing resource productivity.

Leadership:

CEO Marcus Pöllinger promotes long-term ecological stewardship. Leadership works with farmers and partners to adopt regenerative practices such as cover cropping, reduced tillage, soil restoration, and biodiversity initiatives. Training programmes, financial incentives, and knowledge-sharing mechanisms embed these practices across the ecosystem.

Innovation:

BayWa has developed digital farming platforms that measure soil health, track carbon sequestration, and optimise crop yields. Simultaneously, BayWa r.e. expands solar, wind, and biogas projects that provide energy back to farms and communities, creating integrated synergies between agriculture and renewables.

Ecosystem:

The company’s ecosystem spans farmers, suppliers, energy providers, and research institutions. These stakeholders collaborate to improve soil quality, increase biodiversity, and reduce environmental impact while maintaining productivity.

Performance:

BayWa reports consistent growth in renewable energy and sustainable agriculture. Pilot projects show measurable ecological improvements, demonstrating that traditional agribusiness can be transformed into a commercially viable regenerative enterprise.

Climeworks, Switzerland … regenerative carbon

Strategy:

Climeworks leads in direct air capture technology, removing CO₂ from the atmosphere to counter climate change. Its approach is regenerative at the planetary scale: by permanently storing carbon, the company contributes directly to restoring the balance of the carbon cycle.

Leadership:

Founders Christoph Gebald and Jan Wurzbacher foster a culture of scientific excellence and climate responsibility. Leadership emphasises transparency, verification, and the scaling of technology for systemic impact. The company’s ethos integrates ethical stewardship with commercial pragmatism.

Innovation:

Climeworks’ technology generates revenue through subscriptions, corporate partnerships, and government programmes. The Orca and Mammoth plants in Iceland exemplify industrial-scale carbon capture powered by renewable energy. Research and development focus on improving efficiency, reducing costs, and integrating storage solutions that secure long-term carbon removal.

Ecosystem:

The company collaborates with governments, energy providers, and research institutions, creating a networked ecosystem that multiplies impact. Partnerships with corporations such as Microsoft and Stripe demonstrate how private and public sectors can co-invest in scalable regenerative solutions.

Performance:

Climeworks has operationalised commercial-scale direct air capture and attracted substantial investment, proving the financial and technological viability of a regenerative carbon removal model.

Danone, France … regenerative food

Strategy:

Danone integrates regenerative agriculture across its global supply chain, focusing on soil health, water stewardship, and biodiversity. The goal is to transition from linear commodity sourcing to restorative farming models, ensuring that every litre of milk or plant-based ingredient contributes to ecological renewal.

Leadership:

Executives embed sustainability metrics into corporate strategy and remuneration. Leadership cultivates collaborative relationships with farmers, promoting shared learning, capacity building, and ecosystem stewardship. Strategic decisions are evaluated through a dual lens of financial and regenerative impact.

Innovation:

Danone combines consumer-facing innovation with upstream regenerative practice. Programmes include regenerative dairy, sustainable plant-based sourcing, circular packaging, and soil carbon monitoring. Technology and data allow the company to measure outcomes at scale, aligning commercial and environmental objectives.

Ecosystem:

Farmers, co-operatives, NGOs, and suppliers collaborate to implement regenerative methods. This networked approach creates resilience, enhances biodiversity, and stabilises supply chains. Cross-sector partnerships also advance financial models for soil-carbon crediting and sustainable investment.

Performance:

Danone reports measurable improvements in soil carbon, biodiversity, and sustainable sourcing, all while maintaining market share and product profitability. Its model demonstrates that regenerative agriculture can underpin both ecological restoration and commercial growth.

EcoAlf, Spain … regenerative fashion

Strategy:

EcoAlf transforms ocean plastics and other post-consumer waste into high-quality apparel and accessories. Its strategy is purpose-driven: tackle marine pollution while demonstrating that circular materials can deliver premium consumer products. By embedding regeneration into both supply chain and brand storytelling, EcoAlf converts waste into tangible ecological and economic value.

Leadership:

Founder, my good friend, Javier Goyeneche champions a culture of environmental responsibility and creativity. Leadership prioritises material innovation, transparency, and systemic thinking, motivating teams to pursue solutions that restore natural systems while appealing to conscious consumers.

Innovation:

EcoAlf uses recycled ocean plastics, discarded fishing nets, and textile offcuts to produce clothing and bags. Its innovation extends beyond materials to business models, integrating consumer education, transparent impact reporting, and premium branding that aligns profit with planetary benefit.

Ecosystem:

The company collaborates with local waste collectors, recycling facilities, and NGOs to close the loop. Partnerships extend across design, production, and distribution, creating a network that reinforces circularity and environmental awareness.

Performance:

EcoAlf has achieved global market penetration while retaining its regenerative focus. The company demonstrates that luxury and circularity can coexist, proving that consumer goods can be both profitable and restorative.

Ecosia, Germany … regenerative search

Strategy:

Ecosia merges digital technology with ecological regeneration. Its search engine business model channels advertising revenue into reforestation and ecosystem restoration globally. By aligning user activity with planetary benefit, Ecosia operationalises regeneration at scale in an otherwise digital sector.

Leadership:

Founder Christian Kroll instils a culture of transparency, ecological responsibility, and accountability. Leadership emphasises measurable impact, with quarterly reports on tree planting and project outcomes, fostering trust with users and stakeholders.

Innovation:

The company monetises search engine traffic to fund reforestation. Innovations include integrating geographic data to prioritise planting in biodiversity hotspots, developing local community engagement models, and tracking long-term ecological outcomes.

Ecosystem:

Ecosia works with NGOs, local governments, and community groups, forming a collaborative ecosystem that maximises social and environmental value. This network extends to technology providers, advertisers, and civic partners to scale regeneration globally.

Performance:

Ecosia has planted tens of millions of trees and restored degraded land, demonstrating that a simple digital model can generate measurable regenerative outcomes while sustaining a profitable platform.

First Milk, UK … regenerative dairy

Strategy:

First Milk operates as a farmer-owned co-operative, integrating regenerative agriculture into milk production. Its approach focuses on soil health, biodiversity, and carbon sequestration, while maintaining high-quality dairy outputs.

Leadership:

Leadership promotes long-term collaboration with farmer-members, incentivising regenerative practices through both technical support and financial rewards. The culture encourages stewardship over extraction, emphasising resilience and ecological value creation.

Innovation:

The co-operative combines traditional dairy techniques with soil-restorative interventions, such as rotational grazing, cover crops, and hedgerow restoration. It monitors regenerative outcomes, linking ecological performance to member remuneration.

Ecosystem:

Farmers, co-operatives, distributors, and local communities collaborate to implement regenerative practices across the supply chain. This network creates resilience and ensures alignment between ecological goals and operational realities.

Performance:

The programme has enhanced biodiversity, soil quality, and carbon sequestration while maintaining milk yields and market competitiveness. First Milk demonstrates that regenerative agriculture can underpin both ecological health and commercial stability.

Greiner, Austria … regenerative plastics

Strategy:

Greiner, a leader in plastics and foam, has come along way since I first worked with them 10 years ago. It has embraced regeneration through its “Blue Plan” framework, focusing on reducing emissions, increasing recycled content, and restoring material value. The strategy combines operational transformation with long-term ecological objectives.

Leadership:

Leadership integrates sustainability deeply into corporate culture, promoting generational thinking, science-based targets, and innovation in materials. The management ethos balances commercial ambition with environmental accountability.

Innovation:

Greiner’s innovations include mono-material designs for easier recycling, compostable packaging, and high-recyclate foam solutions. Product development actively substitutes virgin plastics with recycled alternatives without compromising performance.

Ecosystem:

Supplier audits, EcoVadis certification, and closed-loop recycling programmes exemplify ecosystem engagement. Greiner collaborates with partners, customers, and regulatory bodies to extend the regenerative impact of its products.

Performance:

With revenues approaching €2 billion, Greiner demonstrates that industrial-scale operations can align with regenerative principles. Emission reductions, increased recycled content, and product longevity all highlight the practical viability of heavy-industry regeneration.

Holcim, Switzerland … Cement and building materials

Strategy:

Holcim is one of my favourite clients, and I have worked with their leaders across the business. It aims to transform construction into a regenerative sector. Its focus is on low-carbon cement, circular aggregates, and climate-positive construction practices. By redesigning both materials and processes, Holcim seeks to mitigate the traditionally high environmental footprint of building materials.

Leadership:

Miljan Gutevic and his executive teams embed sustainability targets into operations, R&D, and capital allocation. Leadership emphasises systemic thinking, linking material innovation to broader environmental restoration goals. Their investor presentations (see the recent Capital Markets Day 2025) are a great example of putting sustainability and regeneration at the core of their strategy.

Innovation:

Holcim invests in alternative binders, recycled aggregates, and carbon capture technologies. Pilots of carbon-negative concrete and modular construction techniques demonstrate tangible regenerative outcomes in urban development.

Ecosystem:

Collaboration with construction companies, municipalities, architects, and NGOs creates a network that extends regenerative impact across the value chain. By sharing knowledge and materials solutions, Holcim accelerates sector-wide adoption.

Performance:

Holcim has reduced CO₂ emissions per ton of cement and launched the first commercial-scale carbon-negative concrete projects. This demonstrates that heavy construction materials can evolve from extractive to restorative business models, paralleling innovations seen in Interface flooring.

IKEA, Sweden … regenerative retail

Strategy:

IKEA aims to become climate-positive by 2030, embedding circular design, renewable materials, and forest stewardship into every aspect of operations. Its approach combines product innovation with supply chain regeneration to create systemic environmental benefit.

Leadership:

Leadership integrates sustainability into product development, corporate strategy, and capital planning. Teams are incentivised to optimise both environmental impact and customer experience, fostering a culture where regeneration is core to the business model.

Innovation:

IKEA has advanced circular design, enabling product repair, reuse, resale, and recycling. Renewable and recycled materials underpin the offering, while digital platforms facilitate product take-back and lifecycle management.

Ecosystem:

Suppliers, forest managers, recyclers, and logistics partners collaborate to achieve regenerative outcomes. This mirrors Arket’s approach to circularity but at a global scale, demonstrating the intersection of industrial and retail ecosystems in driving systemic change.

Performance:

IKEA has increased the share of sustainable materials, implemented energy-positive factories, and piloted resale and repair initiatives, all while sustaining global growth. The company exemplifies the commercial feasibility of large-scale regenerative retail.

Interface, Netherlands/US … regenerative flooring

Strategy:

Interface’s mission, articulated through its Climate Take Back initiative, is to reverse climate change by creating carbon-negative flooring and restoring natural systems. Unlike incremental sustainability measures, Interface targets net-positive impact, aiming to leave the planet better than it found it.

Leadership:

Leadership fosters mission-driven innovation and transparency. Executives embed environmental responsibility into every level of decision-making, from R&D to sales, cultivating a culture where long-term ecological and financial objectives coexist.

Innovation:

Interface produces modular flooring using recycled materials, bio-based alternatives, and closed-loop designs. Programmes like Net-Works convert discarded fishing nets into carpet tiles, simultaneously reducing ocean plastic pollution and supporting coastal communities. Innovative manufacturing methods reduce carbon intensity and water usage, creating a replicable model for regenerative industrial production.

Ecosystem:

Suppliers, recyclers, NGOs, and communities collaborate to extend impact across the supply chain. Partnerships combine ecological restoration, social benefits, and commercial viability, creating a systemic regenerative ecosystem that stretches beyond the company itself.

Performance:

Interface has reduced greenhouse gas emissions per square metre of flooring while expanding revenue from sustainable products. The company demonstrates that restorative industrial practices can scale, supporting both ecological regeneration and brand leadership.

Klima, Germany … regenerative living

Strategy:

Klima offers a digital platform that enables individuals and organisations to measure, reduce, and offset their carbon footprint. Its regenerative approach encompasses ecosystem restoration, carbon neutrality, and behaviour change, translating climate responsibility into tangible outcomes.

Leadership:

Leadership emphasises transparency, accountability, and measurable environmental impact. Teams are encouraged to integrate climate science into product design and user engagement, cultivating a culture of climate-conscious innovation.

Innovation:

Klima funds tree planting, ecosystem rehabilitation, and carbon offset projects through subscription services and corporate partnerships. Innovative algorithms track user emissions and measure reductions, linking behaviour change to actionable regenerative outcomes.

Ecosystem:

The company collaborates with reforestation NGOs, project developers, and local communities, creating a networked model of environmental restoration. Corporate clients and individual users amplify the regenerative effect, while technological integration ensures data-driven impact monitoring.

Performance:

Klima has facilitated measurable reductions in CO₂ emissions and supported ecosystem restoration projects across multiple continents. Its tech-enabled regenerative model demonstrates that digital platforms can play a vital role in systemic environmental impact.

Lush, UK … regenerative cosmetics

Strategy:

Lush integrates regenerative sourcing, ethical supply chains, and community engagement into its cosmetics business. Ingredients are chosen not only for quality but for their ability to restore and maintain ecological systems.

Leadership:

Leadership champions mission-driven culture, embedding social and environmental goals into product development, marketing, and operations. Lush demonstrates how corporate governance can directly reinforce regenerative outcomes.

Innovation:

Lush’s products use natural, ethically sourced ingredients. Programmes include packaging-free “naked” products, refill initiatives, and regenerative farming partnerships. Research and sourcing teams work to continually improve both environmental and social impacts.

Ecosystem:

Supplier networks are carefully managed to promote fair trade, biodiversity, and local community development. Collaborations with NGOs and farmers strengthen regenerative practices while creating resilient, traceable supply chains.

Performance:

Lush maintains strong financial performance alongside measurable social and environmental impact. Its approach illustrates that regenerative principles can be central to brand differentiation, loyalty, and profitability in consumer goods.

PulPac, Sweden … regenerative packaging

Strategy:

PulPac develops fibre-based alternatives to single-use plastics, aiming to regenerate natural systems by substituting renewable, recyclable materials for traditional plastics. The company positions itself at the intersection of material innovation and systemic environmental restoration.

Leadership:

Leadership integrates sustainability into R&D and business growth strategies. Corporate culture encourages material innovation that scales globally while reducing carbon intensity and environmental burden.

Innovation:

PulPac’s proprietary technology produces high-performance fibre packaging suitable for food, pharmaceuticals, and consumer goods. Innovations include high-speed manufacturing processes and compatibility with recycling infrastructure, ensuring low environmental impact at scale.

Ecosystem:

The company works closely with consumer goods brands, material suppliers, and recyclers to expand regenerative impact. Partnerships ensure that fibre substitution translates into measurable ecological benefits, closing the loop on single-use plastic reduction.

Performance:

PulPac has scaled operations internationally, demonstrating that fibre-based, low-carbon packaging solutions are commercially viable. Environmental impact metrics highlight reductions in plastic waste and carbon emissions, reinforcing the regenerative potential of industrial innovation.

Triodos Bank, Netherlands … regenerative finance

Strategy:

Triodos specialises in financing enterprises that deliver social, cultural, and environmental benefits. The bank’s regenerative approach integrates ethical principles into investment decisions, creating systemic positive outcomes across multiple sectors.

Leadership:

Leadership fosters a culture of transparency, ethical responsibility, and long-term thinking. Corporate governance aligns lending and investment policies with measurable regenerative outcomes, demonstrating that finance can be a driver of ecological and social restoration.

Innovation:

Triodos designs lending and investment products that prioritise renewable energy, regenerative agriculture, and social enterprises. Innovative financial instruments link returns to environmental and social impact, allowing capital to flow to projects that generate measurable regeneration.

Ecosystem:

Partnerships with NGOs, renewable energy developers, and social enterprises amplify systemic impact. Triodos’ approach demonstrates the catalytic effect of finance in scaling regenerative solutions across geographies and sectors.

Performance:

The bank has delivered stable financial returns while ensuring positive ecological and social outcomes. Its model proves that banking can be transformed into a regenerative enterprise that supports both profit and planetary well-being.

Veja, France … regenerative footwear

Strategy:

Veja integrates regenerative cotton farming and Amazonian wild-rubber sourcing into its footwear production. Its approach is systemic, targeting soil health, community empowerment, and ecosystem restoration within the supply chain. By embedding regenerative principles into raw material sourcing, Veja demonstrates that fashion can be both profitable and restorative.

Leadership:

Leadership emphasises transparency, environmental integrity, and social impact. Founders Sébastien Kopp and François-Ghislain Morillion cultivate a mission-driven culture, encouraging ethical decision-making across design, sourcing, and marketing.

Innovation:

Veja’s innovations combine sustainable materials, ethical production, and durable design. The company also develops traceable supply chains using digital tools, ensuring that each product reflects measurable regenerative impact.

Ecosystem:

Veja collaborates closely with cooperatives, smallholder farmers, and NGOs to implement regenerative practices. Partnerships support biodiversity, fair income, and local community development, creating a resilient and scalable regenerative ecosystem.

Performance:

Veja has achieved global recognition for sustainability, product quality, and profitability. Its model illustrates that regenerative sourcing can drive brand differentiation and commercial success simultaneously.

Vestre, Norway … regenerative furniture

Strategy:

Vestre designs and manufactures public furniture with a regenerative lens, prioritising biodiversity, low-carbon production, and social value creation. Its approach extends beyond product to factory and urban environment, aiming to leave a net-positive ecological footprint.

Leadership:

Leadership embeds long-term environmental and social objectives into strategic planning. CEO Olav Kristensen promotes a culture where design thinking, industrial manufacturing, and sustainability are inseparable, creating alignment between purpose and execution.

Innovation:

Vestre innovates with low-emission steel production, circular material usage, and design that encourages community engagement and ecological restoration. Its flagship factory, The Plus, embodies regenerative principles in architecture, energy, and workflow.

Ecosystem:

Suppliers, designers, urban planners, and municipalities collaborate to maximise social and environmental impact. Projects integrate ecosystem thinking at city scale, demonstrating how industrial design can influence urban regeneration.

Performance:

Vestre has secured international contracts while achieving significant reductions in carbon footprint and environmental impact. Its regenerative approach strengthens brand value, employee engagement, and global competitiveness, illustrating the viability of purpose-led industrial design.

Wildfarmed, UK/Belgium … regenerative food ingredients

Strategy:

Wildfarmed connects major food brands with regenerative farms, focusing on soil health, biodiversity, and carbon sequestration. Its purpose is to transform conventional agricultural supply chains into networks of ecological and social renewal.

Leadership:

Leadership prioritises systemic change, farmer engagement, and regenerative agriculture education. Founders cultivate a culture that balances commercial viability with environmental responsibility, ensuring that each product sourced contributes positively to the ecosystem.

Innovation:

Wildfarmed acts as a bridge between regenerative farms and industrial-scale manufacturers. Innovations include traceability platforms, impact measurement tools, and sourcing models that reward ecological stewardship, enabling regenerative practices to scale commercially.

Ecosystem:

The company’s ecosystem spans farmers, brands, and supply chain partners. By integrating regenerative criteria into purchasing decisions, Wildfarmed creates incentives for widespread adoption of soil-restorative practices, enhancing biodiversity and carbon capture across landscapes.

Performance:

Despite its smaller scale, Wildfarmed has enabled measurable ecological improvements while maintaining commercial viability for partners. Its model demonstrates that supply chain innovation can operationalise regeneration in global food systems.

Common Themes in Regeneration

Across Europe, leading regenerative companies reveal a coherent set of principles and practices that distinguish them from conventional sustainability initiatives. What unites these businesses is not just a commitment to reduce harm, but a deliberate strategy to create net-positive social, environmental, and economic impact.

From carbon-capturing technologies to circular fashion, regenerative enterprises demonstrate that business can restore ecosystems, strengthen communities, and redefine value creation. Several interlinked themes emerge as critical to their success.

Regenerative Strategy

At the heart of every regenerative company is a purpose-driven strategy that transcends traditional corporate responsibility. This strategy is proactive, systemic, and measurable: it aims not only to mitigate negative impact but to generate positive ecological and social outcomes. Companies like Climeworks target atmospheric carbon removal at scale, EcoAlf transforms marine waste into high-value apparel, and ACCIONA designs infrastructure projects that enhance biodiversity, water quality, and climate resilience.

Regenerative strategies are often codified into specific, quantifiable objectives—carbon neutrality targets, soil health metrics, circular material utilization rates, biodiversity enhancements, or water conservation goals. These metrics inform investment decisions, product development, and operational priorities, creating a clear line of sight between corporate purpose and measurable outcomes. Importantly, these strategies align with wider systemic agendas, such as the EU sustainability taxonomy, ensuring that regenerative ambition is compatible with regulatory frameworks and market incentives.

In effect, regenerative strategy reframes business from a transactional, extractive activity into a restorative system, where every decision—from sourcing to end-of-life design—contributes to environmental and social health.

Regenerative Leadership

Leadership is the engine of regenerative transformation. In these companies, executives do more than set high-level vision; they embed regenerative thinking into culture, governance, and performance systems. Senior leaders link remuneration, career progression, and investment priorities directly to ecological and social outcomes, signalling that regeneration is central to business success.

This leadership ethos cultivates a culture of long-term thinking, resilience, and adaptability. Employees are empowered to participate in sustainability initiatives, suggest innovations, and engage with communities. At Greiner, cross-departmental collaboration drives closed-loop plastics solutions, while at Vestre and Veja, leadership ensures that regenerative principles permeate daily operational decisions—from sourcing and design to logistics and retail.

Crucially, regenerative leadership extends beyond internal culture: it shapes external partnerships, drives advocacy, and aligns corporate strategy with systemic environmental and societal goals. It positions companies as both market leaders and ecosystem stewards, capable of influencing peers, suppliers, and regulators.

Regenerative Innovation

Innovation in regenerative companies is multidimensional, extending far beyond technology to business models, service design, and system-wide processes. Companies demonstrate that regenerative principles can be commercially viable, generating new revenue streams while restoring natural and social systems.

For example:

-

Arket experiments with rental and resale models for clothing, extending product lifespans and reducing resource demand.

-

Climeworks operates subscription-based carbon capture services, monetizing ecological restoration at scale.

-

PulPac produces fibre-based packaging as a high-performance alternative to single-use plastics, creating circular material flows in industries traditionally dependent on virgin resources.

-

Wildfarmed bridges regenerative farmers with industrial-scale food manufacturers, incentivizing soil restoration and biodiversity while maintaining commercial viability.

Such innovation challenges the linear “take-make-dispose” paradigm, fostering circularity, net-positive outcomes, and system-wide resilience. The regenerative mindset encourages companies to design offerings, processes, and collaborations that generate both ecological benefit and business advantage, proving that restoration and profitability are mutually reinforcing.

Regenerative Ecosystems

No company operates in isolation; regeneration is inherently collaborative and networked. Leading businesses actively engage suppliers, communities, NGOs, governments, and even competitors to achieve systemic impact.

Notable examples include:

-

Interface’s Net-Works programme, which collects discarded fishing nets to manufacture carpet tiles, simultaneously restoring marine ecosystems and supporting livelihoods for coastal communities.

-

Ecosia, which directs search-engine revenue into tree-planting initiatives managed in partnership with local NGOs.

-

Danone, collaborating with farmers and cooperatives across Europe to embed regenerative practices into dairy and plant-based supply chains.

In these cases, the supply chain functions not just as a cost center, but as a driver and amplifier of regenerative impact. Companies cultivate ecosystems where stakeholders share knowledge, align incentives, and jointly measure outcomes, demonstrating that regeneration is as much about relationships as it is about technology or products.

Regenerative Performance

A defining feature of regenerative enterprises is the mutual reinforcement of financial and environmental performance. Far from being a burden, regenerative initiatives enhance brand reputation, foster customer loyalty, engage employees, and strengthen operational resilience.

Financially, companies report growth in revenue from sustainable products, operational efficiencies, and risk mitigation. For example:

-

IKEA’s repair and resale programmes extend product life and reduce raw material costs.

-

Climeworks’ subscription revenue model scales alongside measurable carbon removal.

-

EcoAlf has built a profitable global fashion brand based on recycled materials.

Non-financial performance is equally critical and measurable:

-

Greenhouse gas reductions (Holcim, Interface)

-

Soil regeneration and carbon sequestration (Danone, Wildfarmed, First Milk)

-

Biodiversity enhancement (Acciona, Vestre, Veja)

-

Water conservation (BayWa, Acciona)

-

Social impact metrics including fair labor practices, community development, and employee well-being (Lush, Triodos Bank)

By quantifying both ecological and social outcomes, these companies demonstrate that regeneration is not a soft aspiration but a strategic, measurable, and profitable business imperative.

Regenerative Futures

The regenerative revolution is underway, offering a compelling narrative for the future of business. Across sectors, companies like Climeworks and Danone, Greiner and Holcim, demonstrate that restoring the planet and society need not compromise financial success. On the contrary, embedding regeneration can foster innovation, resilience, and long-term growth.

The cases illustrate that regeneration is both practical and scalable, spanning advanced industrial operations, consumer goods, agriculture, finance, and technology. Leadership, purpose, innovative business models, and ecosystem engagement form the pillars of success. Crucially, regeneration shifts the frame from avoiding harm to actively creating positive impact, aligning commercial success with the flourishing of people and planet alike.

In a world facing rapid ecological, social, and economic change, the regenerative revolution is not optional—it is a blueprint for sustainable prosperity, proving that businesses can thrive while restoring the very systems upon which they depend.

The companies above represent different routes to regeneration.

Greiner shows how heavy industry can reorient towards regenerative ends through product design, alliance building and operational decarbonisation. Ecoalf demonstrates how consumer brands can turn environmental restoration (marine clean-ups) into the raw material for premium products, creating jobs and local benefits. Interface and Patagonia reveal the power of governance and supply-chain redesign to make profound claims credible. Danone, Unilever and IKEA underline the systemic leverage of global buyers to alter agricultural and material systems. Vestre and VEJA show that industrial architecture and transparent supply chains can embed environmental renewal into daily life.

What can leaders learn?

-

Integration into Core Strategy: Regeneration is most successful when it is embedded into the business model, rather than treated as an ancillary initiative. Companies like Acciona, IKEA, and Interface exemplify strategic integration, linking financial performance with ecological outcomes.

-

Leadership and Culture: Executive commitment, performance incentives, and cultural alignment are essential. Across the sample, leadership consistently connects vision, operations, and measurable impact — from BayWa’s stewardship ethos to Triodos Bank’s ethical investment principles.

-

Innovation Across Products and Processes: Regeneration is driven by both material and process innovation. Holcim’s carbon-negative cement, PulPac’s fibre-based packaging, and EcoAlf’s marine-waste apparel show that regenerative thinking catalyses new product categories and business opportunities.

-

Ecosystem Thinking: Partnerships with suppliers, communities, NGOs, and governments amplify impact. Ecosystem approaches ensure that regenerative gains are systemic rather than localised, as seen in Climeworks’ carbon capture networks or Wildfarmed’s supply chain interventions.

-

Performance and Measurability: Financial and ecological metrics are increasingly intertwined. European regenerative leaders demonstrate that profit and impact are not mutually exclusive — measurable environmental restoration often correlates with customer loyalty, market differentiation, and operational resilience.

-

Scalability and Replicability: Many of these companies, from Greiner to Arket, show that regenerative models can scale across sectors, geographies, and industrial processes, proving that regeneration is commercially viable at multiple levels.None of this is easy. Regeneration requires patient capital, new metrics, policy support and an acceptance that short-term profit optimisation will sometimes be subordinate to long-term ecological and societal value creation. Yet the evidence is mounting that companies can — and some already do — write business models that replenish the natural and social capital on which all commerce ultimately depends.

Across sectors and geographies, Europe’s regenerative leaders reveal a new paradigm for business—one in which strategic purpose, leadership, innovation, ecosystem engagement, and measurable impact converge. Their approaches show that companies can go beyond sustainability, actively restoring natural systems, empowering communities, and generating commercial value.

In a world facing escalating ecological and social challenges, these examples provide a blueprint for business transformation, proving that regeneration is both a moral and economic imperative.

More from Peter Fisk

- Eyes on Tomorrow: What Leaders Must See before Everyone Else … exploring the most important megatrends that are transforming markets, and leadership mindsets, and how the best companies embrace them as opportunities … based on the new Megatrends 2035 report by Peter Fisk, and its implications for every business.

- The Reinvention Playbook: Thriving in a World of Relentless Change … the best organisations seek to continually reinvent themselves in a world of constant, uncertain and dynamic change. They rethink, refocus, and reinvent everything – embracing new agendas from AI to GenZ, climate change and social inequality.

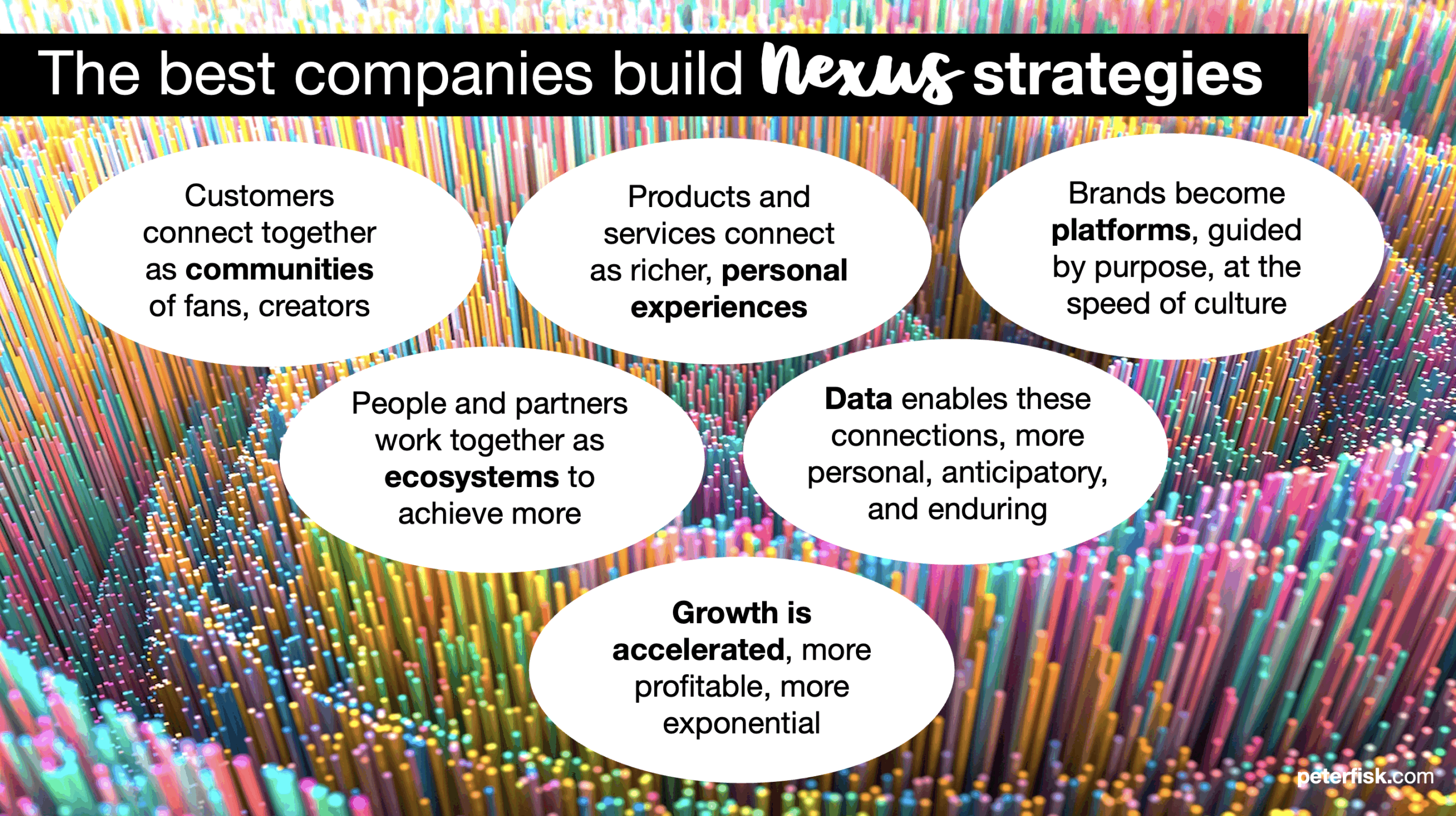

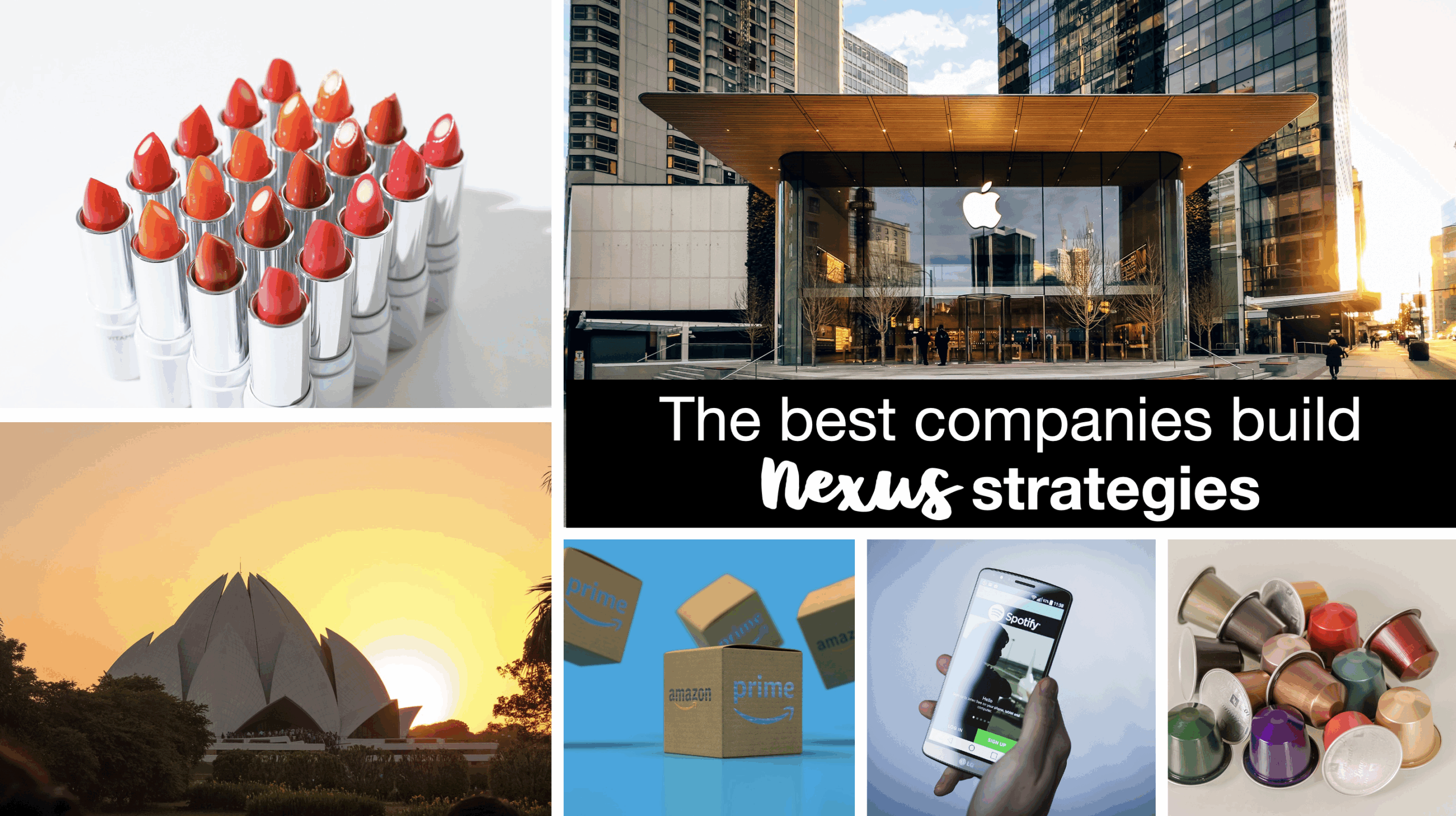

- The Nexus Effect: Unlocking the Power of Connections … How can businesses and brands really unlock the power of data and networks, flywheels and AI, communities and ecosystems, to transform their futures?

- The New Growth Playbook: 9 New Ways to Accelerate Growth … many companies struggle to find new ways to grow their business … instead we look at how the best companies find radically new ways to grow.

- Super Innovators: Innovation Beyond the Normal … 10 radical ways to disrupt conventions, embrace deeper insights, unlock valuable assets, and stretch innovation for more dramatic impact.

- Consumer of the Future … “Aisha blinked twice, the smart lenses in her eyes had already scanned her biometric mood, cross-checked her carbon budget, and pulled up items her climate-positive friends were buying this week”

- Competing in the FLUX: How to develop a dynamic strategies in a world of relentless change … combining a strong, enduring direction with micro-moves that adapt quickly to emerging shifts:

- Business Transformation: The new superpower of business leaders … reimagining the future, redefining strategy, reinventing the organisation, rewiring performance … the journey to deliver step change in value creation.

- The Sustainable Consumer: Go on, do the Right Thing … how brands can accelerate the consumer shift to sustainable products and practices … from food and fashion, to energy and electric cars, making sustainability desirable and better.

- The “Performer Transformer” Leaders: How great leaders deliver today and create tomorrow … with dual thinking, to build dynamic ambidexterity, continually strategyzing, to perform and transform.

- The Hire-Wire Act of Leadership: Leading in a world of intense competition and relentless change … being visionary and innovative, learning to adapt and endure … inspired by Taylor Swift, Roger Federer, Beyoncé, and Lionel Messi

- Becoming a Future-Ready Business … in a world of relentless change, organisations need to anticipate change, embrace innovation, empower talent, and align deeply with the evolving needs of society and the planet

For over a century, the boardroom has been a place of authority, oversight, and assurance. Directors assessed risk, monitored performance, and protected continuity. In a stable world, this approach was sufficient. But stability is now a luxury few businesses can afford.

We live in an era of relentless change: markets shift at unprecedented speed, technologies converge, customer expectations evolve, and environmental and social imperatives demand urgent action. The rules of competition are being rewritten, often overnight. In such a world, a board that governs only the status quo risks not only irrelevance, but the survival of the business itself.

Enter The Boardroom Compass: a three-day immersive retreat for company boards, designed to equip directors to navigate complexity, make sense of emerging opportunities, and act decisively in shaping the long-term future.

The program is conceived and led by Peter Fisk, a globally recognised authority on business leadership, strategy, and reinvention, together with Pierre Kairouz, a seasoned expert in board governance and executive leadership. Their combined experience ensures the retreat is at once visionary and grounded, stretching thinking while remaining practically actionable.

Why boards must evolve

Boards are no longer merely custodians of performance; they are architects of the future. The most successful boards:

- Think strategically with courage, imagination, and a long-term lens.

- Align business models, strategies, and organisational design to a compelling purpose.

- Embed transformation not only in plans, but in culture, leadership, and capabilities.

- Engage stakeholders across generations, from Gen Z to ageing populations, balancing divergent expectations.

- Understand the strategic impact of AI, data, and convergent technologies, and use these insights to guide opportunity and risk.

Without this evolution, boards risk being reactive, marginalised, or unable to support their CEOs in delivering transformational change.

The Boardroom Compass

The Boardroom Compass is built around a central idea: boards must navigate the future with clarity, courage, and collaboration.

It provides directors with:

- A structured framework for understanding disruptive forces and strategic inflection points.

- Exposure to global examples of business reinvention and organisational transformation.

- Tools to translate insight into actionable guidance for executive teams.

- Opportunities to strengthen cohesion, alignment, and confidence in decision-making.

Importantly, it is not a management course. Participants remain firmly in the boardroom seat, exploring the implications of emerging trends, assessing strategic options, and sharpening their stewardship capabilities.

Key themes explored

1. Making Sense of the Future

Boards are bombarded with information but often starved of insight. The retreat helps directors distinguish between transient noise and enduring signals, using scenario thinking to explore plausible futures and anticipate strategic inflection points.

2. Strategy as a Dynamic Capability

Static, annualised strategies are insufficient. Boards are guided on how to oversee strategy as a living system, continuously adapting to market changes, technological shifts, and stakeholder expectations. Companies like Amazon and Microsoft exemplify this, demonstrating boards’ role in endorsing ambition while ensuring feasibility.

3. Technology and Convergent Forces

AI, robotics, data analytics, and platform technologies are no longer optional tools; they are central to value creation. Boards explore the implications of emerging technologies on business models, ethics, and competitive advantage.

4. Stakeholders and Trust

Trust is now a strategic asset. Boards consider how to engage stakeholders authentically, balancing generational expectations, social legitimacy, and customer experience. Examples from Unilever, Patagonia, and On Running illustrate purpose-led engagement as a driver of growth and resilience.

5. Board–CEO Partnership

Future-ready boards are active partners in transformation. They provide guidance, mentorship, and air cover for bold decisions without overstepping into operational management, enhancing the CEO’s ability to deliver strategic outcomes.

Global examples of board-supported transformation

- Microsoft: Alongside CEO Satya Nadella, the board endorsed a shift from defending legacy software to a cloud and AI-driven platform strategy, supporting a growth mindset culture.

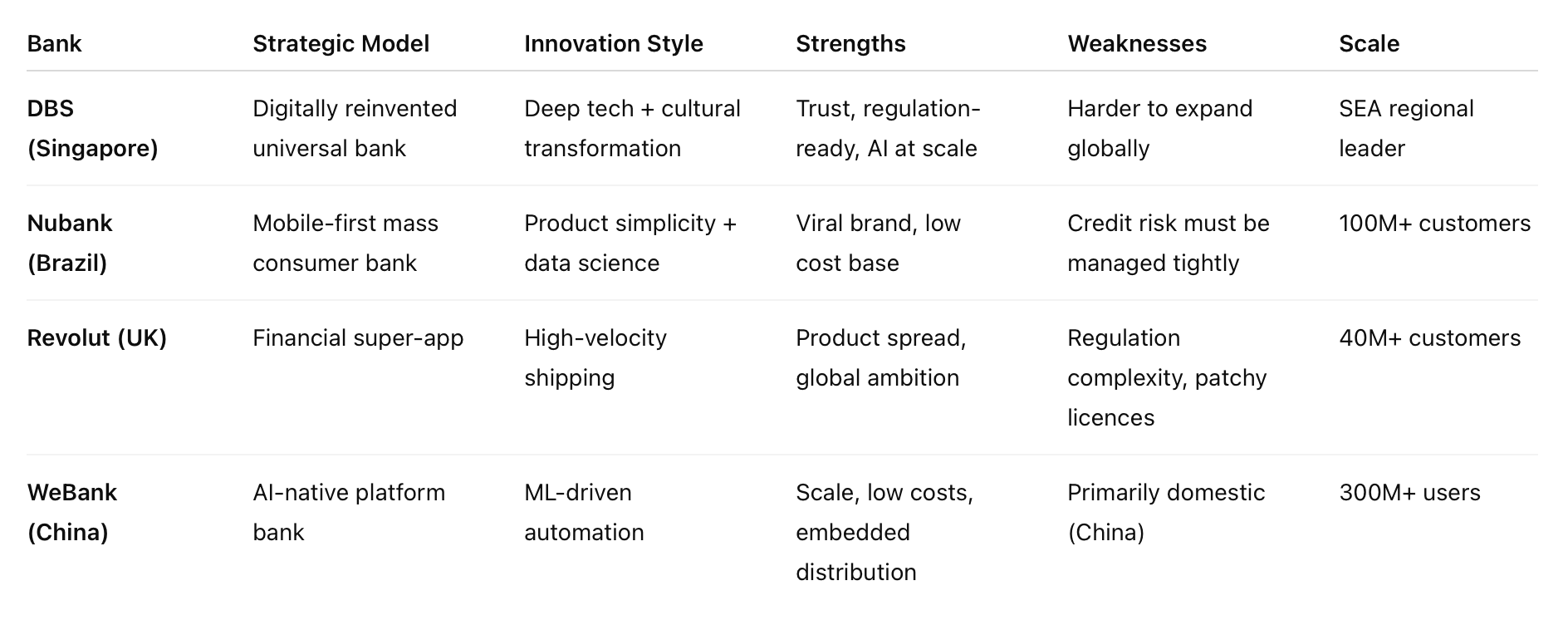

- DBS Bank: Singapore’s most innovative bank reimagined itself as a “tech company in banking,” with the board sponsoring agile teams and digital-first leadership.

- Schneider Electric: Transitioned from hardware to IoT-enabled services, with board oversight ensuring sustainability, digital capability, and organisational alignment.

- Lego: Board guidance enabled a return from near-bankruptcy to global innovation leadership through purpose-aligned strategy and a culture of creativity.

These examples underscore that board-level stewardship is critical to both bold ambition and successful execution.

The Boardroom Compass Program Outline

Duration: 3 days

Format: Immersive, interactive, and board-focused, combining global insight with applied exercises.

Day 1 … Navigating the Strategic Horizon

- Purpose and Vision: Explore why the organisation exists, define long-term ambitions, and clarify what success looks like.

- Global Disruptors: Examine megatrends, technologies, change drivers and risks across sectors.

- Business Reinvention: How companies around the world are reinventing themselves for the future.

- Strategic Priorities: Identify opportunities, risks, and five-year growth imperatives.

Day 2 … Reimagining the Organisation

- Leadership for the Future: Assess leadership gaps, mindset shifts, and behaviours required to deliver transformation.

- Culture and Values: Analyse current culture, design future culture to support strategy, and embed purpose-led decision-making.

- Organisation Design: Explore agile, platform, and hybrid structures to match strategic ambitions.

- Capabilities and Ecosystems: Identify talent, technology, and partnership requirements critical to execution.

Day 3 … Guiding Transformation

- Alignment and Integration: Map strategy to organisational structure and capabilities, ensuring coherence and feasibility.

- Phased Transformation Roadmap: Define waves of change, KPIs, and governance mechanisms.

- Ownership and Commitment: Assign responsibility, clarify accountability, and establish ongoing engagement.

- Future-Ready Board: Reflect on insights, define personal and collective commitments, and embed the future-ready mindset.

Outcomes for boards

Participants leave The Boardroom Compass with:

- Strategic Clarity: A shared understanding of long-term direction, risks, and opportunities.

- Organisational Insight: Recognition of the culture, leadership, and capabilities needed to succeed.

- Actionable Roadmap: A phased, realistic, and prioritised plan for transformation and value creation.

- Enhanced Board Cohesion: Greater confidence, alignment, and ability to challenge constructively.

- Future-Ready Mindset: Capability to navigate uncertainty, embrace emerging technologies, and guide the executive team with courage and foresight.

Future-ready boards

The boardroom of the future is not a passive hall of oversight; it is a space for active stewardship, bold thinking, and long-term impact. The Boardroom Compass is a novel and inspiring program that helps boards navigate the uncertainty of today to ensure the prosperity of tomorrow. By combining deep insight, practical frameworks, and global inspiration, it equips directors to lead with clarity, courage, and confidence – turning strategic foresight into meaningful action.

In an era of relentless change, boards that embrace this shift are not merely guardians of value, they are architects of it.

“Strategic foresight” – or as I prefer to call it, leading the business from the future back – is rapidly becoming a core leadership capability. In a world defined by accelerating change, deep uncertainty and constant disruption, the leaders and organisations that consistently outperform are not those that predict the future most accurately, but those that anticipate change earlier, make better decisions today, and actively shape what comes next rather than reacting to it.

For much of the last century, leadership was about optimisation. Competitive advantage was built through scale, efficiency and control. Strategy assumed continuity, and planning largely meant extrapolating the past. That logic no longer holds. Today, any advantage is temporary, industry boundaries are porous, and shocks propagate across systems faster than traditional planning cycles can respond.

“Thinking like a futurist” is no longer a niche skill or an innovation luxury. It is a leadership discipline, one that connects long-term possibility to near-term performance, and imagination to execution.

Over the past two decades, one of the most powerful tools I have worked with leadership teams to embed — across food and fashion, travel and telecoms, energy and entertainment — is strategic foresight integrated directly into strategy, innovation, portfolio management and capital allocation. When foresight is embedded properly, it consistently drives better growth, stronger margins, lower risk and more durable value creation.

Why business leaders need a future mindset

The case for a future mindset is both strategic and economic.

First, the pace of change is accelerating faster than traditional planning cycles. Technology adoption curves are compressing. Consumer expectations reset annually, not generationally. Regulation, geopolitics and climate risk increasingly reshape markets with little warning. In this environment, five-year plans become obsolete within months if they are not continuously refreshed.

Second, the nature of value itself has changed. Today, over half of corporate value is driven by intangible, future-facing assets: brands, ideas, data, platforms, ecosystems and capabilities that determine tomorrow’s growth rather than yesterday’s efficiency. These assets are shaped by choices made long before results appear in financial statements.

As a result, companies that anticipate change earlier consistently outperform those that react later. Across sectors, they:

- Innovate more successfully, with higher hit rates and faster scaling

- Deliver stronger profitability and faster, more resilient growth

- Allocate capital more effectively, exiting declining assets earlier and investing sooner in future growth platforms

- Build future-ready organisations that attract talent, partners and long-term investors

At the heart of this performance gap is a shift in mindset.

Business leaders who think like futurists move:

- From analysing the past to imagining better futures

- From seeking certainty to building agility and preparedness

- From optimising the present to continuously reinventing for what comes next

Today still matters — but always in the context of tomorrow.

What it means to think like a futurist

Thinking like a futurist is not about prediction. It is about perspective.

Futurist leaders start from the future back, rather than extrapolating the past forward. They define what success could look like five to ten years from now, then work backwards to identify the strategic choices, capabilities and investments required today.

They learn outside-in more than inside-out. External signals — from customers, culture, technology, regulation and adjacent industries — carry more weight than internal reports optimised around existing structures.

They look beyond competitors to understand how value is shifting across ecosystems, not just within categories. The most disruptive threats — and the most powerful opportunities — often come from outside the industry frame.

Crucially, futurist leaders are able to see signals in the noise. They do this by:

- Making sense of megatrends such as climate change, demographics, technology acceleration and geopolitical realignment

- Identifying patterns across markets, consumers and categories, not just within one business unit

- Focusing on intersections, where trends multiply and new value pools emerge

Over time, foresight becomes a leadership skill built on four capabilities:

- Curiosity: actively seeking unfamiliar perspectives and challenging orthodoxies

- Sense-making: turning weak signals into strategic meaning

- Future-back thinking: defining long-term success and working backwards

- Making better choices: using foresight as the starting point for strategy and innovation decisions

How leading companies use foresight

Leading companies do not use foresight as a theoretical exercise. They embed it directly into decision-making, with tangible impact on both short- and long-term performance.

Example 1. Disney: backcasting the future of experience

Disney’s evolution from a traditional animation studio into a multi-platform entertainment ecosystem is the result of deliberate future thinking. Rather than extrapolating from the present, Disney frequently uses backcasting — defining a desired future state and working backwards to determine what capabilities, technologies and acquisitions are required to get there.

When Disney asks, “What will immersive storytelling look like in 2040?”, the answer shapes decisions made today — from acquisitions such as Pixar, Marvel and Lucasfilm to investments in theme parks, streaming platforms and experiential technologies.

Disney also maintains a dedicated strategic foresight capability that works directly with the C-suite, identifying disruptive “black swan” events — from pandemics to shifts in travel behaviour — and exploring their implications long before they materialise. The result is not agility alone, but coherence across decades.

Example 2. Shell: making uncertainty governable

Shell is widely regarded as the pioneer of corporate foresight. Its scenarios team has been operating for more than half a century, famously helping the company navigate the oil shocks of the 1970s by having already rehearsed a world of volatile prices and geopolitical disruption.

What distinguishes Shell is not the quality of its scenarios, but how they are used. Shell does not attempt to predict a single future. Instead, it develops multiple, radically different “possible worlds” — and stress-tests strategy and investments against each of them.

Foresight at Shell is not advisory. It is institutionalised. No major capital project proceeds without a scenario resilience check. In effect, foresight functions as a governance mechanism, forcing leaders to confront uncomfortable possibilities before committing billions. Uncertainty is not eliminated — it is made manageable.

Example 3. Unilever: using the future as a strategic constraint

Unilever stands out for its deeply outside-in approach, particularly around social and environmental megatrends. Through its Sustainable Living Plan — now evolved into the Unilever Compass — the company integrated foresight into its brand and portfolio strategy. Instead of asking what competitors are doing, Unilever asks what the world will require.

What does it mean to operate within planetary boundaries? What will consumers expect of brands in a carbon-constrained, resource-limited world? These questions become strategic constraints that shape innovation, sourcing, packaging and marketing decisions today.

Unilever uses “future-fit” benchmarks — measuring brands not just against current market norms, but against what will be necessary by 2030 and beyond. This forces earlier, sometimes uncomfortable, pivots — but builds long-term relevance and trust.

Example 4. Siemens: turning foresight into investment logic

As an industrial technology leader, Siemens has institutionalised foresight through its “Pictures of the Future” methodology.

This approach combines systematic trend scouting with “wild card” analysis — low-probability, high-impact events that could fundamentally reshape markets. The output is not generic trend decks, but detailed future scenarios for specific domains such as energy systems, mobility and urban infrastructure.

Crucially, these future pictures inform R&D roadmaps and portfolio decisions. When foresight suggests that decentralised energy will dominate, Siemens begins reallocating investment away from centralised fossil-based systems years before markets peak. Foresight becomes an early-warning system — and a trigger for capital reallocation.

Example 5. Lego: designing for future relevance

Lego’s turnaround from near-bankruptcy in the early 2000s was built on a profound commitment to foresight and human insight.

The company established a Future Lab that operates with startup-like autonomy, supported by a global scanning network of children, educators, technologists and cultural observers. The goal is not to track toy trends, but to understand how play itself is evolving — cognitively, socially and digitally.

This foresight reshaped Lego’s strategy: expanding into digital gaming, movies and experiences, while simultaneously investing in sustainable materials and circular design. It did not abandon its core. It reinterpreted it for the future.

Across these examples, foresight-driven companies consistently do three things differently:

- Use scenarios to stress-test strategy and challenge assumptions

- Make earlier moves into future growth categories and value pools

- Actively reshape portfolios rather than defending legacy assets

In FMCG and adjacent sectors, the practical impact is clear:

- Faster growth from foresight-aligned brands, within and across categories

- More resilient margins through relevance and premiumisation

- Higher return on innovation investment

- Reduced exposure to regulatory, sustainability and demand shocks

The strategic implications for how we do business

When foresight is embedded effectively, it reshapes the entire operating model.

- It transforms strategy, shifting organisations from fixed plans to dynamic portfolios that evolve as the future unfolds.

- It reframes innovation, moving from linear pipelines to portfolios of experiments deliberately spread across time horizons.

- It strengthens supply chains, evolving transactional supplier relationships into resilient, sustainable partnerships.

- It redefines talent, shifting from treating people as resources to building the capabilities required to create the future.

- It changes how organisations approach transformation, moving from crisis-driven change to continuous, future-led renewal.

At a deeper level, foresight drives a fundamental shift in leadership and decision-making:

- From past-driven, experience-led thinking to future-oriented, possibility-led thinking

- From assuming incremental change to preparing for non-linear disruption

- From seeking certainty to building preparedness

Strategic thinking moves from single forecasts to multiple scenarios; from static plans to adaptive pathways; from defending current positions to shaping future markets.