A teenager in São Paulo sees a skincare routine on Instagram. She taps through a creator’s “get ready with me” video, follows a link to a livestream on a marketplace, compares bundles in an app, pays instantly through ApplePay, and picks up the product an hour later at a nearby locker. No shopping list. No store visit as a starting point. No “trip” to retail at all.

This is not a future scenario, it is already how retail works for many, particularly in the vast emerging markets of Asia and beyond. Discovery begins in entertainment. Commerce is embedded in content. Payment is invisible. Fulfilment is local, instant and omnipresent.

Retail has quietly stopped being a place. It has become a system.

I’ve seen this shift up close through my work this year with the business leaders of OXXO, the extraordinary proximity retail network built by FEMSA in Mexico and now expanding rapidly across North and South America, and also to Europe. What makes OXXO remarkable is not simply its scale, but its evolution: from convenience stores to everyday infrastructure for life itself.

In many communities, OXXO is no longer just where you buy snacks or drinks. It is where you pay bills, access financial services, send parcels, top up mobile data, pick up online orders, and increasingly where new services emerge – from healthcare clinics and government services, branded eateries to fuel partnerships, local market traders and community hub. It sits at the intersection of retail, finance, logistics, mobility and community life.

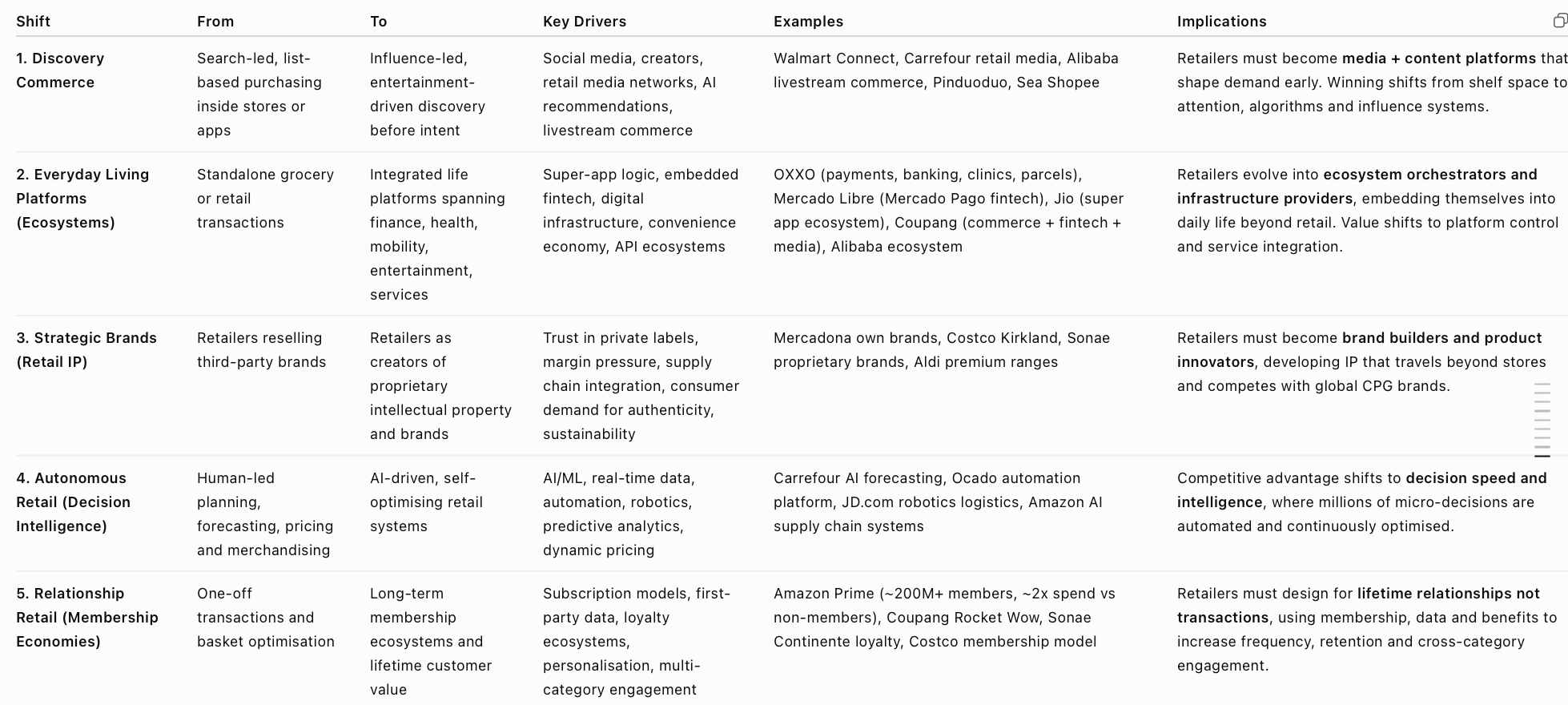

5 forces reinventing retail

Retailers are no longer competing to sell more products. They are competing to become the operating system of daily life.

What used to be a relatively stable value chain — manufacturers create, retailers distribute, consumers choose — has fragmented into a real-time, AI-mediated, platform-orchestrated environment where demand is continuously shaped, redirected, and monetised across multiple competing systems simultaneously.

And that shift is being driven by 5 powerful forces: discovery commerce, lifestyle ecosystems, strategic brands, autonomous retail and relationship-based membership. Together, they are rewriting what retail means—and who wins in the future.

The retail industry is seeing faster and more dramatic change than almost any other sector. Social influence, enabled by Instagram and TikTok has transformed the context in which consumers shop, integrators like Grab and Jio have transformed the channels by which they interact, and Walgreens to Walmart have transformed what they offer, and ultimately their reason for being.

We see a dramatic restructuring of the industry, built on a convergence of many adjacent sectors, an acceleration of technologies, and a disruptive change in business models, demanding new capabilities and new leadership. This goes far beyond new store formats, omnichannel delivery, and personalised loyalty. This is rapid, radical reinvention.

The world’s most innovative retailers – Amazon to Alibaba, Carrefour to Coupang, Getir to Gojek, Shopee to Sonae – increasingly look less like merchants and more like media companies, platform businesses, technology firms and lifestyle partners.

1. Discovery Commerce … from search to influence

Consumers increasingly buy what influences them, not what they search for. Shopping decisions are made long before a shopping list is written, shaped by creators, communities, AI recommendations, livestreaming and social media. The customer journey has shifted from “Search, Compare, Buy” to “Inspire, Discover, Validate, Purchase”.

The old journey was a functional journey, in the context of transactional retail. The new model typically starts elsewhere, on the sofa, in the gym, on vacation, with friends. On Instagram, or TikTok. Increasingly too, shopping is becoming entertainment. Consumers don’t simply discover products, they discover stories, experiences and communities.

Leading retailers are responding by becoming media businesses. Walmart Connect has become one of the world’s largest retail media platforms, enabling brands to influence shoppers long before they enter a store. Carrefour combines retail media with AI and loyalty data to personalise engagement, while Alibaba pioneered livestream commerce that blends entertainment and shopping. Pinduoduo transformed shopping into a social experience through group buying and gamification, while Sea’s Shopee combines gaming, creators and commerce to drive product discovery.

- More than 70% of purchase decisions are influenced before consumers enter a store, through digital content, recommendations and social engagement.

- Retail media is expected to exceed $175 billion globally by 2028, making it one of the fastest-growing advertising sectors.

- Livestream commerce already generates hundreds of billions of dollars annually in China, and is rapidly expanding globally.

What it demands: Retailers must stop thinking like merchants and start thinking like media companies. Systems thinking rather than funnel thinking. Winning is no longer about stocking products, it is about creating influence, shaping demand and building communities long before purchase.

2. Everyday Living … from food stores to lifestyle ecosystems

The world’s leading retailers are no longer building retail businesses—they are building platforms for everyday living. Grocery is becoming just one service within much broader ecosystems that include finance, healthcare, entertainment, logistics, telecoms, education and mobility.

The ambition is no longer to own a bigger share of a customer’s shopping basket, but a bigger share of their daily life.

OXXO has evolved into a neighbourhood services platform, offering banking, payments, parcel collection, telecom services and everyday financial transactions. Mercado Libre transformed an online marketplace into one of Latin America’s largest fintech businesses through Mercado Pago, alongside lending, insurance and logistics. Coupang combines retail with grocery, food delivery, streaming, fintech and its Rocket Wow membership, while Reliance Jio is creating India’s leading super app, integrating commerce, payments, pharmacy, entertainment, education and digital services. Alibaba has built an ecosystem spanning retail, payments, cloud computing, logistics, AI, entertainment and local services. Sea links gaming, digital finance and e-commerce into a single consumer platform.

Increasingly, retailers are becoming part of national and community infrastructure. They help people manage money, access healthcare, collect parcels, receive prescriptions, stream entertainment and navigate everyday life—not simply buy products.

- Mercado Pago now serves more than 60 million monthly active users, becoming one of Latin America’s largest digital financial platforms.

- Jio Platforms serves more than 490 million subscribers, creating one of the world’s largest integrated digital ecosystems.

- Ecosystem businesses consistently achieve significantly higher customer lifetime value because customers engage across multiple services rather than isolated transactions.

What it demands: Retailers must evolve from store owners into ecosystem orchestrators. Their role is to connect multiple services around the customer, creating indispensable platforms that customers use every day.

3. Strategic Brands … from private labels to IP advantage

Private labels are no longer cheaper alternatives, they are becoming strategic intellectual property. The strongest retailers are creating brands that stand for innovation, health, sustainability, premium quality and unique customer experiences. They have obvious advantages over conventional manufacturer brands, they can add services, become experiences, and be portfolios.

Increasingly too, these brands extend well beyond the retailer’s own shelves through licensing, partnerships, digital products and exclusive experiences.

Mercadona has built one of Europe’s most admired own-brand portfolios through relentless product innovation and deep supplier collaboration. Costco’s Kirkland Signature has become a global consumer brand in its own right, often outperforming traditional manufacturers. Sonae continues to develop proprietary brands that increasingly reach consumers beyond its own retail formats. It also means that sometimes more experiential stores can thrive like Eataly, where eating and cooking, come before buying.

- Private-label products account for more than 40% of grocery sales in several European markets.

- Premium private-label ranges continue to grow faster than value ranges as trust in retailer brands increases.

- Own brands typically deliver higher margins and stronger customer loyalty than equivalent national brands.

What it demands: The retailer is evolving from distributor to creator. Retailers must think like brand builders and product innovators, creating valuable intellectual property that customers actively seek rather than simply accept.

4. Autonomous Operations … from automation to decision intelligence

AI is becoming retail’s operating system. Rather than simply automating repetitive tasks, AI is increasingly making thousands of operational decisions every day—from demand forecasting and merchandising to dynamic pricing, inventory optimisation, personalised marketing and autonomous fulfilment.

Leading retailers are creating businesses that become progressively more self-managing. Carrefour uses AI to improve forecasting, optimise assortments and personalise promotions. Ocado has built one of the world’s most sophisticated AI-powered fulfilment platforms, combining robotics, automation and predictive analytics. JD.com deploys robot warehouses and autonomous delivery technologies, while Amazon continues to expand AI across merchandising, logistics and store operations.

- AI can reduce forecasting errors by 20–50%, significantly lowering waste and stock-outs.

- Leading retailers now deploy AI across merchandising, pricing, marketing, supply chains and customer service rather than isolated functions.

- Autonomous fulfilment can dramatically improve productivity while reducing operating costs and delivery times.

What it demands: Competitive advantage increasingly comes from decision intelligence—the ability to make millions of faster, smarter and more autonomous decisions than competitors.

5. Relational Experiences … from transactions to membership

The most valuable customers are not those with the biggest baskets, but those with the strongest relationships. The world’s leading retailers are shifting from transactions to memberships, creating recurring engagement, richer customer data and greater lifetime value.

Loyalty is evolving into subscription. Membership becomes the operating system that connects multiple services into one seamless customer relationship.

Amazon Prime has redefined retail membership by combining fast delivery, groceries, entertainment, healthcare and exclusive benefits into a single subscription. Coupang’s Rocket Wow performs a similar role by integrating grocery, commerce, food delivery, streaming and rapid fulfilment into one membership experience. Sonae’s Continente loyalty ecosystem connects supermarkets with health, fashion and partner services, creating a richer, more personalised customer relationship across multiple aspects of everyday life.

- Amazon Prime has more than 200 million members globally, with members spending approximately twice as much annually as non-members.

- Subscription and membership customers typically shop more frequently, remain customers for longer and demonstrate significantly higher lifetime value.

- The combination of membership, first-party data and AI is becoming one of retail’s most powerful competitive advantages.

What it demands: Retailers must optimise customer lifetime value rather than basket value—building relationships that become stronger with every interaction, across every format and service.

The Bigger Shift … retail beyond retail

Across all five shifts, one pattern repeats:

- From products, to platforms

- From stores, to systems

- From transactions, to relationships

- From operations, to intelligence

- From retail, to infrastructure to everyday life

Retail is no longer a sector defined by selling goods. It is becoming a set of overlapping influence systems, service ecosystems, brand factories, autonomous decision engines and relationship platforms.

The companies that win will not simply move along these axes individually—they will integrate all five simultaneously into a coherent operating model of modern life.

The future of retail is not a more efficient version of what exists today, it is a fundamentally different role in society.

Retail will increasingly disappear as a distinct “sector” at all. Instead, it will be woven into the fabric of everyday life: shaping what people want before they know it, orchestrating services across health, money, mobility and entertainment, and using AI to anticipate needs in real time. Stores will matter less as destinations and more as nodes in living networks. Brands will matter less as labels and more as trusted systems. And transactions will matter less than continuous relationships.

The most successful retailers will no longer ask how to sell more things. They will ask a deeper question: how do we become indispensable to how people live?

In that world, the boundary between retail, technology, media, healthcare, finance and infrastructure dissolves. What emerges instead are adaptive platforms that learn, evolve and respond—quietly shaping daily life in the background, while feeling effortless on the surface.

And perhaps the most profound shift of all: retail stops being something we go to.

It becomes something that is always with us.

For more than 35 years, I have been fortunate to work with business leaders in every corner of the world, helping them imagine what comes next and reinvent their organisations for a changing future. Along the way, I have worked with more than 300 companies across over 50 countries, from global giants to ambitious start-ups, from government agencies to family businesses.

One lesson has become increasingly clear. Great ideas are not confined to Silicon Valley, London or Shenzhen. Innovation can emerge anywhere. Not because one place has better technology than another, but because people everywhere face problems worth solving. The best innovators simply see those problems differently.

In Argentina, I helped Mercado Libre develop one of the world’s leading fintech platforms. In Egypt, I worked with Orascom to imagine entirely new cities. In Azerbaijan, Azercell reinvented telecoms as a life concierge. In China, I watched Haier transform from an appliance manufacturer into a global ecosystem of connected products and services. In Iceland, Climeworks pushed the boundaries of carbon capture. In Denmark, the city of Odense reinvented itself as one of the world’s leading robotics hubs.

These experiences have convinced me that the geography of innovation is being rewritten. Every country, city and organisation has the potential to shape the future in its own distinctive way. That is why Mehran Gul’s The New Geography of Innovation resonated so strongly with me. It captures a truth I have seen repeatedly throughout my career: the next great idea could come from anywhere.

Innovation without borders

It is a rethinking of one of the most persistent myths in modern business: that innovation is concentrated in a small number of global “hotspots,” most notably Silicon Valley. Gul challenges this idea directly, arguing instead that innovation is becoming increasingly distributed, multipolar, and shaped by a far more complex global landscape of cities, institutions, capital flows, and talent networks.

At its core, the book is about movement—of ideas, people, capital, and technologies—and how that movement is reshaping where innovation happens and who gets to participate in it. Gul’s central argument is that we are entering an era in which innovation is no longer anchored to a few dominant geographies, but instead emerges from a shifting mosaic of regional ecosystems, each with its own strengths, constraints, and strategic logic.

Rather than treating innovation as a purely technological phenomenon, Gul frames it as a geopolitical, institutional, and urban process. Where innovation happens depends not just on talent and venture capital, but on regulation, culture, infrastructure, education systems, state capacity, and global connectivity. In this sense, geography is not background—it is destiny-shaping.

Beyond Silicon Valley

One of the book’s central intellectual targets is the “Silicon Valley narrative”, the idea that breakthrough innovation is primarily the product of a unique concentration of talent, risk capital, and entrepreneurial culture in one region.

Gul does not deny Silicon Valley’s importance. Instead, he argues that its dominance has created a misleading mental model. For decades, policymakers and business leaders have assumed that replicating Silicon Valley requires copying its surface features: venture capital, startups, incubators, and tech campuses. But this overlooks deeper structural conditions that are far harder to replicate.

These include:

- deep university-industry linkages

- immigration-enabled talent inflows

- legal frameworks that support risk-taking

- massive defence and research spending

- dense professional networks

- a culture of failure tolerance

- global market access

Silicon Valley is not just a cluster of companies. It is an entire institutional ecosystem that evolved over decades, often through unique historical conditions.

Gul’s key point is that trying to reproduce Silicon Valley elsewhere often fails because it focuses on symptoms rather than systems.

The rise of new innovation hubs

Rather than a single dominant centre, Gul describes a world in which multiple innovation hubs are emerging simultaneously, each specialising in different dimensions of technological and industrial development.

He highlights the rise of cities and regions across Asia, the Middle East, Europe, and Latin America that are developing distinctive innovation profiles. Some excel in manufacturing ecosystems, others in digital platforms, fintech, biotech, or deep-tech research.

For example:

- Shenzhen represents manufacturing speed, hardware iteration, and supply chain density.

- Bangalore has become a global hub for software engineering and digital services.

- Tel Aviv stands out in cybersecurity and defence-related innovation.

- Berlin and London combine creative industries with fintech and digital entrepreneurship.

- Singapore has positioned itself as a regulated innovation hub, balancing state capacity with openness.

Rather than competing to become “the next Silicon Valley,” these regions are developingdifferent models of innovation suited to their institutional contexts.

Gul’s argument is that this diversity is not a temporary phase, but the defining characteristic of the next era.

Innovation as an ecosystem, not a place

A central conceptual shift in the book is the move from thinking about innovation as location-based to thinking about it as ecosystem-based.

In Gul’s framing, innovation is not simply what happens in a city. It is what happens when multiple systems align:

- universities producing research and talent

- firms commercialising ideas

- investors allocating risk capital

- governments shaping regulation and incentives

- infrastructure enabling connectivity

- global networks linking local ecosystems to markets

When these elements reinforce each other, innovation accelerates. When they are misaligned, even well-resourced regions struggle.

This explains why some cities with significant capital and talent still fail to produce sustained innovation, while others with fewer resources succeed.

Gul emphasises that ecosystems are dynamic. They evolve over time, responding to shocks such as technological shifts, geopolitical changes, and economic crises. This dynamism means that no innovation geography is permanently dominant.

The role of the state in shaping innovation

A particularly important theme in the book is the role of the state—not as a passive regulator, but as an active architect of innovation systems.

Gul argues that different countries adopt fundamentally different models of state involvement in innovation. Some adopt a laissez-faire approach, relying heavily on markets and venture capital. Others take a more interventionist stance, using industrial policy, strategic investment, and infrastructure development to shape outcomes.

Importantly, he suggests that both models can work—but in different contexts and for different types of innovation.

For example, state-led strategies have been particularly effective in scaling industries that require coordination, capital intensity, and long time horizons, such as semiconductors, renewable energy, and advanced manufacturing. Market-led systems tend to excel in software, platforms, and consumer internet innovation, where experimentation and speed matter more than coordination.

The implication is that there is no single optimal model of innovation governance. Instead, countries must align their institutional structures with their strategic ambitions.

Globalisation and fragmentation

Another key argument in The New Geography of Innovation is that globalisation is not disappearing, but transforming.

Earlier phases of globalisation were characterised by increasing integration, with supply chains spreading across borders in pursuit of efficiency. Innovation often followed this pattern, with multinational firms distributing R&D, production, and talent across global networks.

However, Gul argues that we are now entering a more fragmented phase, shaped by geopolitical competition, supply chain resilience concerns, and strategic decoupling in certain industries.

This fragmentation does not eliminate innovation networks, but it reshapes them. Companies and countries are increasingly building regionalised innovation systems, balancing global connectivity with strategic autonomy.

As a result, innovation is becoming both more global and more local at the same time: global in knowledge flows, but local in production and strategic control.

Talent as the true currency of innovation

Across the book, Gul consistently returns to one central resource: talent.

While capital is mobile and technology is increasingly accessible, talent remains the most important constraint on innovation ecosystems. However, talent itself is becoming more geographically fluid due to remote work, digital platforms, and global education networks.

This creates a paradox: talent is both more concentrated in certain hubs and more distributed globally than ever before.

Cities and countries that successfully attract, retain, and develop talent gain disproportionate advantages. Immigration policy, education systems, quality of life, and professional opportunity all become critical determinants of innovation success.

Gul suggests that in the long term, the most successful innovation ecosystems will be those that function as talent magnets rather than capital magnets.

The importance of institutional density

A subtle but important idea in the book is what might be called “institutional density.” Innovation ecosystems thrive not just because of individual companies or universities, but because of the richness of interactions between institutions.

Dense ecosystems allow:

- rapid knowledge transfer

- cross-sector collaboration

- faster commercialisation of research

- mobility of talent between firms

- feedback loops between markets and innovation

Silicon Valley’s enduring advantage, Gul argues, is not just venture capital or startups, but the density of relationships between universities, firms, investors, and government agencies.

Emerging hubs that want to compete must therefore focus not only on attracting anchor companies, but on building these deep relational structures.

Innovation cycles and shifting leadership

Gul also emphasises that innovation leadership is cyclical. Historically dominant regions eventually lose their edge as new technologies, industries, and institutional conditions emerge.

For example, leadership in industrial innovation has shifted over time from Britain to the United States, and now increasingly to a more distributed global system involving Asia, Europe, and beyond.

These shifts are not random. They reflect changes in:

- energy systems

- communication technologies

- production methods

- education systems

- geopolitical structures

The implication is that current innovation maps are temporary. The geography of innovation is always being rewritten.

The new geography

The most important idea in The New Geography of Innovation is that innovation is not anchored to place—it is anchored to systems of alignment.

Places matter, but only insofar as they enable the alignment of institutions, capital, talent, infrastructure, and governance.

This reframing has significant implications for governments, investors, and corporate leaders. Instead of asking “Where is the next Silicon Valley?”, the more useful question becomes:

Where are the ecosystems most effectively aligning the conditions for innovation in a particular domain?

A more complex innovation world

The New Geography of Innovation ultimately replaces a simple story with a more complex—but more realistic—one. Innovation is no longer the preserve of a handful of global cities. It is a distributed, competitive, and evolving system shaped by multiple overlapping forces.

Gul’s message is both cautionary and optimistic. Cautionary because no region can assume permanent leadership in innovation. Optimistic because the diffusion of innovation capabilities creates more opportunities for countries, cities, and organisations to participate in shaping the future.

The geography of innovation is no longer fixed. It is fluid, contested, and constantly being redrawn.

“The world is in perpetual motion, and we must invent the things of tomorrow. One must go before others, be determined and exacting, and let your intelligence direct your life. Act with audacity.”

Few quotations capture the essence of innovation and leadership as elegantly as these words from Madame Clicquot, the visionary behind one of the world’s greatest champagne houses. Written to her great-granddaughter more than 150 years ago, they read less like family advice and more like a timeless manifesto for anyone determined to shape the future.

Madame Clicquot understood something that many leaders still struggle to embrace: change is not an interruption to business, it is the natural condition of the world. Markets evolve, technologies redefine industries, customer expectations shift, and competitive advantage is always temporary. The only sustainable response is to keep inventing what comes next.

Her challenge to “go before others” is a call to lead rather than follow. The future is rarely created by those who wait for certainty or consensus. It belongs to those with the courage to explore new possibilities, question accepted wisdom, and act before the opportunity is obvious to everyone else.

Yet she also recognised that bold ambition without disciplined execution is little more than wishful thinking. She combined audacity with determination, precision and exacting standards. Innovation succeeds not simply because ideas are original, but because they are pursued with relentless excellence.

Perhaps her most important message is to “let your intelligence direct your life.” In an age overwhelmed by noise, opinion and convention, she reminds us to think independently, stay curious, trust evidence and exercise sound judgement.

The entrepreneurial life of Barbe-Nicole Clicquot

In 1805, at just 27 years old, Barbe-Nicole Ponsardin Clicquot was widowed when her husband, François Clicquot, died unexpectedly. François was heir to a small but promising Champagne house in Reims, a region already beginning to develop international recognition for sparkling wine.

Their marriage had been as much commercial partnership as personal union. François was interested in expanding the business, and Barbe-Nicole had been exposed early to commerce, finance, and disciplined thinking through her family background in French aristocratic banking circles.

When François died, the business was fragile. France was still in the turbulence of the Napoleonic era. Trade routes were unstable, and luxury consumption was unpredictable.

The opening of her story, often portrayed in modern retellings including the recent film Widow Clicquot, is strikingly stark. At François’s funeral, she stands in grief—but also at a crossroads that is both personal and structural.

Her father-in-law, Philippe Clicquot, saw only risk. He proposed selling the vineyards to the Möet family, effectively dissolving the enterprise into a rival dynasty.

This is where the story becomes strategic rather than sentimental.

The Möet family, already influential in Champagne, would later become part of what is now Moët Hennessy Louis Vuitton through modern consolidation. At the time, however, they represented competitive absorption: a reminder that industries tend to consolidate around stronger operators unless countered by decisive leadership.

Barbe-Nicole refused.

She resisted not just emotional loss, but structural absorption. She argued to retain control of the vineyards and the business. In doing so, she made a decision that transformed her from widow into operator, and eventually into one of the earliest examples of a global brand architect.

Widow Clicquot, the movie

Her life has recently been reinterpreted in the film Widow Clicquot, which opens with the emotional shock of François’s funeral in 1805 and the immediate threat of losing the vineyards.

A line from the film captures its symbolic resonance: “When they struggle to survive, they become more reliant on their own strength… they become more of what they were meant to be.”

While fictionalised in places, the film captures an essential truth: pressure reveals structure. Barbe-Nicole Clicquot’s life was not defined by inheritance, but by transformation under pressure.

The reinvention of champagne

What followed was not continuation, it was reinvention.

She took control of a fragile, regional wine house and, over the next decades, transformed it into one of the first globally recognised luxury brands in history.

Her leadership can be understood through four interlocking dimensions that remain foundational to modern branding and entrepreneurship.

1. Building a global business in a time of extreme disruption

Her first strategic act was international expansion under conditions that should have made expansion impossible.

France in the early 19th century was defined by war, blockade, political upheaval, and fragile trade infrastructure. Most producers contracted inward. She expanded outward.

Rather than treat instability as a constraint, she treated it as a directional signal: if domestic markets were unreliable, then survival required global imagination.

Her most important breakthrough came through Russia.

Following the Napoleonic wars, Russian aristocracy developed a strong appetite for French luxury goods as symbols of sophistication and cultural alignment with Europe’s elite traditions. Barbe-Nicole moved decisively into this market.

Her champagne became deeply embedded in aristocratic ritual—served at court celebrations, diplomatic gatherings, and elite social occasions. It was not merely exported; it was adopted as a cultural marker.

This was early-stage globalisation executed without modern infrastructure. She built distribution networks, navigated tariffs, managed political uncertainty, and ensured consistent supply in a volatile environment.

In doing so, she accomplished something rare: she turned Champagne from a regional product into an international category.

2. Innovation that made scale possible

Her second breakthrough was technical, but its consequences were strategic.

One of her most significant contributions was the refinement and commercialisation of the “riddling table” (remuage) process. This innovation allowed winemakers to gradually move sediment into the neck of the bottle, enabling clearer champagne after disgorgement.

Before this, champagne was inconsistent, often cloudy, and difficult to standardise. After it, it became reliable, scalable, and exportable.

This matters because luxury without consistency cannot scale.

In modern business terms, she solved the problem of industrial reproducibility in a product that depended on biological variability. This enabled export markets to trust the product across distance and time.

She effectively turned champagne into a manufacturable luxury good—without stripping away its craftsmanship identity.

3. Creating champagne as a global luxury brand

Her third contribution was perhaps the most profound: she did not just sell champagne—she created its meaning.

Before her intervention, champagne was a regional beverage. After her, it became a cultural symbol.

She understood something that modern brand strategists still emphasise: value is not inherent in the product, it is constructed in the mind of the consumer.

She positioned her champagne as a drink of celebration, refinement, and emotional significance. It became associated not with consumption, but with moments of transition and meaning: victory, joy, prestige, and occasion.

In Russia especially, champagne became part of elite identity expression. Her brand became embedded in aristocratic rituals, where opening a bottle signified not just hospitality, but status.

This is the origin of Veuve Clicquot as we know it today: not a beverage, but an emotional signal.

Modern Veuve Clicquot still reflects this legacy. Its branding, packaging, and tone continue to emphasise boldness, confidence, and celebratory modernity. The iconic yellow label is not merely aesthetic, it is semiotic. It signals recognition, prestige, and continuity with a two-century-old idea of luxury.

She created one of the earliest examples of what we would now call experience-based branding: where the product is secondary to the meaning it carries.

(Indeed while Veuve Clicquot translates from French as Widow Clicquot, the brand has reframed Veuve as “verve” meaning energy, confidence and celebration).

4. Execution … discipline, quality, and operational control

Her fourth contribution was executional excellence.

She was famously rigorous about quality control, production standards, and distribution discipline. She understood that luxury brands are not built through aspiration alone, but through relentless consistency.

In an era without modern logistics systems, she ensured that product integrity was preserved across borders and time. She personally oversaw decisions relating to production quality, pricing strategy, and export reliability.

This created something essential: trust.

And trust is the hidden infrastructure of luxury. Without it, branding collapses into marketing. With it, brands become institutions.

Her discipline ensured that every bottle reinforced the same promise: quality, refinement, and celebration.

A competitive landscape: Moët and industry consolidation

It is impossible to understand her achievement without situating it within the broader competitive landscape of Champagne.

One of her most important early competitors was the Möet family, already active in Champagne production during her time. While she was building Veuve Clicquot into a structured export business, Moët was also expanding its own presence.

This parallel evolution matters because it shows that Champagne was not a solitary success story—it was an emerging competitive ecosystem of houses defining different interpretations of luxury.

Over time, these brands evolved through mergers and consolidation. Today, both lineages sit within the same global luxury architecture under LVMH Moët Hennessy Louis Vuitton, one of the world’s largest luxury groups.

In a sense, what began as entrepreneurial competition in the early 19th century has become part of the foundation of modern luxury capitalism.

Madame Clicquot’s legacy therefore sits not only in Veuve Clicquot, but in the entire architecture of Champagne as a global category.

La Grande Dame … a woman ahead of her time

Her achievements become even more remarkable when viewed against the constraints of her era.

She operated in a legal and cultural system where women were rarely permitted to own or control businesses independently. She faced institutional scepticism, financial pressure, and social expectations that did not anticipate female leadership at scale.

Yet she did not merely participate in the system, she redefined its possibilities.

She became known as “La Grande Dame of Champagne”, a recognition that reflects both her commercial success and her cultural impact.

Veuve Clicquot, the brand today

Today, Veuve Clicquot stands as one of the most recognisable luxury champagne brands in the world. Its identity – bold, confident, slightly irreverent, but always refined – still reflects her original entrepreneurial DNA.

The brand operates across global luxury markets, from Europe and the United States to Asia, maintaining a positioning that blends heritage with modern cultural relevance. Its events, collaborations, and design language all reinforce a central idea: celebration is not passive, it is intentional.

That idea originates with her.

A legacy of audacity

Madame Clicquot’s legacy is not simply that she built a successful champagne house. It is that she helped invent the architecture of modern luxury branding.

She transformed a fragile inheritance into a global institution. She turned a regional product into a cultural symbol. She built consistency where none existed. And she defined meaning where there was only commodity.

Her life demonstrates four enduring truths

- Global growth is possible even in instability

- Innovation enables scale

- Meaning creates brand power

- Discipline sustains trust

And beneath all of it lies a more human lesson: leadership is not about position, it is about response.

“The world is in perpetual motion. Act with audacity.”

And in doing so, she left behind not just a brand, but a blueprint for how modern businesses create value in a changing world.

In 1993, I was working in Sunnyvale, in the heart of Silicon Valley.

One evening, three guys walked into a local Wendy’s burger restaurant and started talking about gaming, and their frustration with the limits of computing power. Why couldn’t tech companies create better chips? Why did they just serve the average productivity-seeking user, rather than hard-core users like them?

One of those 3 guys was Jensen Huang, a 30 year old mid-career chip engineer. Born in Taiwan, his family had emigrated to the US when he was 9, and he’d grown up in Oregon. They agreed to start their own business, focused on high powered chips. 30 years later, that business became the world’s first $5 trillion company.

The three founders were looking for a name which evoked speed, power, and desirability in graphics computing. They liked the word “invidia” which is Latin for envy. And from that burger, that frustration, emerged the (stylised in capitals) corporate name which now leads the world of technology, NVIDIA.

The Thinking Machine

Stephen Witt’s The Thinking Machine is one of the best narratives to explain the rise of NVIDIA and, more broadly, the transformation of artificial intelligence into the defining industrial system of the 21st century.

While it is structured as a corporate biography of Jensen Huang and NVIDIA’s evolution, its deeper purpose is to explain something far larger: how computing moved from being a tool of software companies into becoming the foundational infrastructure of the global economy.

At its core, the book is not really about chips. It is about the emergence of a new industrial stack, one in which compute power becomes the scarce resource that determines which companies, countries, and technologies can progress. In Witt’s framing, NVIDIA is not just a successful hardware company. It is the builder of the “thinking machine”: the distributed computational substrate that enables modern AI systems to exist at all.

The result is a story that sits at the intersection of entrepreneurship, semiconductor engineering, platform economics, and geopolitical strategy.

NVIDIA’s central idea: compute becomes intelligence infrastructure

Witt’s most important argument is that artificial intelligence did not emerge simply because of breakthroughs in algorithms or data availability. It emerged because of a parallel revolution in hardware—specifically, the GPU.

Originally designed for video game graphics, GPUs turned out to be uniquely suited for the kind of parallel computation required for deep learning. This accidental alignment between gaming hardware and neural networks created the conditions for the modern AI boom.

But Witt pushes the argument further. He suggests that once AI models began scaling, compute itself became the limiting factor of intelligence. The ability to train and run large models depends not just on clever software, but on access to vast, highly specialised computational infrastructure. From this perspective, NVIDIA did not just “win” a technology cycle. It became the gatekeeper of cognitive capacity at scale.

For CEOs, this reframes AI entirely. It is not a software category. It is an infrastructure dependency—similar to electricity in the industrial age or oil in the 20th century.

Jensen Huang and the philosophy of long-cycle thinking

A significant portion of the book is devoted to Jensen Huang, who has remained over three decades as the company’s long-serving CEO. Witt portrays Huang not as a conventional Silicon Valley entrepreneur, but as a leader shaped by long time horizons, technical obsession, and extreme resilience.

Unlike many tech founders who pivot frequently or chase market trends, Huang is characterised by consistency. NVIDIA’s strategy over decades has been remarkably stable: invest heavily in parallel computing architectures long before their commercial payoff is obvious.

Witt highlights a key leadership pattern: Huang repeatedly commits to architectures and platforms that take years—sometimes decades—to become fully realised markets. This includes the shift from gaming GPUs to general-purpose compute, and later to AI-specific architectures.

The strategic implication is profound. NVIDIA’s success is not the result of reacting quickly to AI. It is the result of anticipating a world in which parallel computation becomes the basis of intelligence itself.

For CEOs, Huang’s leadership model suggests that in deep technology industries, advantage accrues not to the fastest adapters, but to the most persistent system-builders.

The GPU revolution: from graphics to general intelligence

One of the most important narrative threads in The Thinking Machine is the transformation of the GPU from a niche gaming component into the central engine of AI.

Initially, GPUs were designed to render images for video games by processing thousands of small calculations in parallel. This architecture was ideal for graphical rendering, where many pixels must be processed simultaneously. However, researchers in machine learning discovered that neural networks also rely on parallel computation—specifically matrix multiplications across large datasets. This unexpected alignment meant that GPUs could accelerate AI training by orders of magnitude compared to traditional CPUs.

Witt emphasises that this was not a planned transition. It was a convergence of separate technological trajectories: gaming demand on one side, academic machine learning research on the other.

Once this convergence was recognised, NVIDIA began investing heavily in software ecosystems (particularly CUDA) to lock developers into its platform. CUDA effectively transformed GPUs from hardware products into programmable intelligence infrastructure. This shift is critical. It means NVIDIA is not just selling chips—it is selling a full-stack computational environment that defines how AI is built.

CUDA: the hidden moat

One of the most strategically important sections of the book concerns CUDA, NVIDIA’s proprietary software layer that allows developers to write programs for GPUs.

While hardware competitors can theoretically build similar chips, CUDA created a deep ecosystem lock-in. Over time, thousands of AI researchers and engineers built workflows, libraries, and systems around NVIDIA’s architecture. Witt describes this as one of the most powerful “invisible moats” in modern technology. It is not just technical superiority, it is ecosystem dependency.

For organisations trying to compete with NVIDIA, the challenge is not simply building better chips. It is recreating an entire developer ecosystem, which took more than a decade to mature.

For CEOs, this illustrates a broader principle of platform power: control of developer experience becomes control of the market.

The scaling laws and the AI demand explosion

Witt also situates NVIDIA’s rise within the emergence of scaling laws in AI research—the empirical observation that model performance improves predictably with increases in data, compute, and model size.

This insight transformed AI from a research domain into an industrial scaling problem. If performance improves with scale, then competitive advantage goes to the organisations that can deploy the most compute. This created an exponential demand curve for GPUs. Companies like OpenAI, Google, Meta, Amazon, and countless startups began competing for access to NVIDIA’s hardware.

Witt highlights a key structural shift: AI stopped being a marginal research activity and became a compute-hungry industrial process. This fundamentally changed NVIDIA’s position in the value chain. It moved from being a component supplier to being the central enabler of frontier AI.

The new industrial stack: chips, systems, and intelligence

One of the most important conceptual contributions of the book is its implicit mapping of the new AI industrial stack.

At the bottom layer are semiconductor fabrication processes, where physical constraints determine what is possible. Above that are chip designers like NVIDIA. Above that are system integrators building data centres. Above that are cloud providers. And finally, at the top layer, are AI model developers and applications.

Witt’s argument is that NVIDIA sits unusually close to the foundation of this stack, giving it disproportionate influence over everything built above it. This structure mirrors earlier industrial revolutions. Just as control of steel, oil, or electricity determined economic power in previous eras, control of compute infrastructure now determines AI capability.

For executives, this implies that competitive advantage in AI is not only about models or data, but about access to and control of computational infrastructure.

Supply chains and physical constraints

A major theme in the book is the physical reality behind digital intelligence. Despite AI often being framed as an abstract software domain, Witt repeatedly emphasises that it is grounded in extremely tangible constraints: fabrication plants, lithography machines, energy consumption, and global supply chains.

NVIDIA does not manufacture its own chips. Instead, it relies on TSMC in Taiwan, ASML in Europe, and a complex global network of suppliers. This introduces geopolitical fragility into the AI ecosystem. The entire global AI boom depends on a small number of highly specialised manufacturing nodes.

Witt uses this to highlight a paradox: AI is often described as dematerialised intelligence, but it is in fact one of the most materially constrained technologies in existence.

Nvidia as a platform company, not a hardware company

One of the most important reinterpretations in the book is that NVIDIA should not be understood as a semiconductor company in the traditional sense.

Instead, Witt frames it as a platform company for computational intelligence. This distinction matters. Traditional hardware companies compete on price, performance, and manufacturing efficiency. Platform companies compete on ecosystem control, developer lock-in, and network effects.

NVIDIA’s dominance is therefore not just technological. It is structural. The company has created a self-reinforcing ecosystem in which:

- developers build on CUDA

- researchers optimise for NVIDIA architectures

- cloud providers standardise NVIDIA hardware

- AI labs depend on NVIDIA GPUs for training

This creates a compounding advantage that is extremely difficult to dislodge.

The geopolitical dimension

Although not always framed explicitly as a geopolitical book, The Thinking Machine inevitably becomes one. NVIDIA sits at the centre of global competition between the United States and China over AI capability.

Access to advanced chips has become a strategic lever. Export controls, supply chain restrictions, and national AI strategies all reflect the recognition that compute is now a strategic resource.

Witt shows that NVIDIA’s position is unusual: it is simultaneously a private company, a global infrastructure provider, and a geopolitical chokepoint.

For CEOs, this raises a fundamental question: in strategically important industries, where does corporate strategy end and geopolitical exposure begin?

The economics of scarcity

A recurring insight in the book is that AI is defined not by abundance but by scarcity—specifically scarcity of compute.

Despite rapid innovation, demand for GPUs consistently exceeds supply. This creates pricing power, long waiting lists, and strategic allocation decisions by NVIDIA.

Witt highlights how this scarcity has reshaped the economics of AI development. Companies are forced to make trade-offs between model size, training time, and deployment scale based on compute availability rather than purely technical ambition.

This reinforces NVIDIA’s central position: it effectively controls the bottleneck of modern intelligence production.

The emergence of AI as industrialisation

Perhaps the deepest argument in The Thinking Machine is that AI represents not just a technological shift, but a new phase of industrialisation.

In earlier industrial revolutions, societies learned to harness energy (steam, electricity, oil) to amplify physical labour. In the AI era, societies are learning to harness compute to amplify cognitive labour. NVIDIA sits at the centre of this transition, providing the infrastructure for machine intelligence at scale.

Witt suggests that we are still at the early stages of this transformation. Just as electricity took decades to reshape economies, AI infrastructure will gradually reshape every industry—from finance and healthcare to manufacturing and logistics.

Strategic implications for CEOs

Although The Thinking Machine is not written as a business strategy manual, its implications for executives are clear. There are 5 takeaways which I would suggest are key for business leaders:

- AI should be treated as infrastructure investment, not software adoption. Competitive advantage will depend on access to compute, not just algorithms.

- Platform dependencies matter. Organisations building AI systems are increasingly dependent on a small number of infrastructure providers, creating concentration risk.

- Supply chain resilience is now part of AI strategy. Semiconductor geopolitics, energy availability, and hardware access are strategic variables.

- Long-cycle thinking is essential. NVIDIA’s success illustrates the value of sustained investment in foundational technologies long before they become obvious winners.

- AI should be understood as an industrial system rather than a tool. It requires rethinking organisational design, capital allocation, and operating models.

The machine beneath the intelligence revolution

The Thinking Machine ultimately reframes the entire AI revolution. It shifts attention away from applications and models and toward the underlying infrastructure that makes intelligence at scale possible.

Stephen Witt’s central contribution is to show that NVIDIA is not merely a successful company riding an AI wave. It is the builder of the wave’s physical substrate—the compute layer that enables modern artificial intelligence to exist.

The book’s lasting insight is simple but profound: every intelligence system has an industrial base. In the case of AI, that base is compute, and NVIDIA is its dominant architect.

For CEOs, the message is clear. Understanding AI requires understanding not just what it does, but what it is built on. And what it is built on is increasingly the most strategically important resource in the global economy.

Yesterday, SpaceX became a public company. In the largest IPO in history, it raised $75 billion at a $1.77 trillion valuation. By the close, investors had pushed it beyond $2 trillion. It now ranks among the world’s most valuable firms, larger than most industrial giants and many national economies.

But the real story is not valuation. It is what SpaceX signals about the future of business.

For two decades, strategy favoured asset-light models. Companies owned brands, software and data, while outsourcing manufacturing and infrastructure to ecosystems. Airbnb to Uber, McDonald’s to Nike.

SpaceX reverses that logic. It designs, builds, launches and operates its rockets, satellites and communications networks. Instead of relying on partners, it integrates almost every layer of its stack.

This challenges the belief that ecosystems always win. In fast-moving technologies, control and speed of learning can outweigh coordination efficiency. Vertical integration becomes a strategic advantage.

It also marks the return of physical infrastructure as the core driver of value creation. AI, like space, is brutally physical. It depends on chips, energy, data centres and massive compute infrastructure. The next wave of value will be built on atoms, not just algorithms.

Already, tech giants are pouring hundreds of billions into energy and computing capacity. The direction is clear: intangible software alone is no longer enough.

SpaceX sits at the intersection of space and AI.

Today’s data centres consume vast land, power and water. But within a decade, some may move into orbit—powered by constant solar energy and cooled by the vacuum of space. Computing itself could become space infrastructure.

In that world, SpaceX becomes more than a launch company. It becomes the infrastructure backbone of the intelligence economy. Launch systems enable satellites. Satellites enable networks. Networks enable computing. Computing enables AI.

The significance of SpaceX’s IPO is therefore not financial alone. It marks a shift in business thinking—from owning platforms to owning the infrastructure of the future. The next winners may not rent the world. They will build it.

Exor … from Fiat’s industrial roots to a platform for influence

On the surface, Exor looks like a classic European holding company with deep industrial roots. Its history is inseparable from Fiat, founded in 1899 by Giovanni Agnelli in Turin. For much of the twentieth century, the Agnelli family’s influence was anchored in manufacturing scale, automotive engineering, and national industrial identity.

But over the past two decades, Exor has quietly undergone a profound transformation. It has moved away from being a controlling industrial shareholder toward becoming something more fluid and contemporary: a long-term investment platform designed to allocate capital, shape strategy, and connect businesses without necessarily controlling them.

Today, Exor’s portfolio includes globally significant companies such as Ferrari and Stellantis (including Fiat and Jeep), Iveco trucks to Philips healthcare, fashion brands like Christian Louboutin and Shang Xia, and even the Economist . Yet what is striking is not just the diversity of assets, but the deliberate absence of tight operational integration between them.

Exor does not behave like a traditional conglomerate. It does not attempt to impose a unified operating model or extract centralised synergies. Ferrari is not structurally integrated with Philips. The Economist is not managed alongside Stellantis. Instead, each company operates independently, with its own governance, leadership, and strategy.

The central question, therefore, is how Exor creates value at all.

The answer lies in a subtle but powerful shift. Exor operates less as an owner and more as a system of influence. It creates value through time horizon alignment, capital discipline, reputation, and carefully cultivated relationships between companies that would otherwise have little reason to interact.

Inside the Exor system … how influence replaces integration

The Exor model works because it is deliberately selective about where connection matters and where it does not. It does not try to force integration across incompatible business models. Instead, it allows collaboration to emerge where intellectual or strategic spillovers are possible.

Within this ecosystem, value creation happens through four reinforcing mechanisms.

First, there is a shared investment philosophy. Across the portfolio, companies are encouraged to think in decades rather than quarters. This long-term orientation shapes decisions on innovation, capital allocation, and resilience. It is not imposed through operational control, but reinforced through governance expectations and repeated interaction.

Second, there is relational proximity. Leaders of portfolio companies interact through formal and informal channels, building familiarity and trust over time. These interactions rarely produce direct joint ventures, but they often lead to shared insights on strategy, risk, and transformation.

Third, there is reputational coherence. The Agnelli name still carries significant weight in global business. This reputation acts as a soft governance mechanism: companies benefit from being associated with a credible, long-term oriented investment steward, which in turn reinforces alignment.

Fourth, there is cognitive cross-pollination. Ideas travel between sectors not because systems are integrated, but because leaders are exposed to one another’s thinking.

However, Exor is also disciplined about where collaboration does not work.

Where collaboration works well in Exor-style ecosystems

These are areas where ideas and frameworks travel easily:

- Leadership philosophy and governance models

- Capital allocation discipline and long-term investment thinking

- Sustainability frameworks and ESG approaches

- Brand strategy and reputation building

- Innovation mindset and experimentation culture

- Executive networking and talent development

Where collaboration tends to fail or add limited value

These domains resist ecosystem integration because they are too context-specific:

- Core sales execution and go-to-market systems

- Operational IT and legacy infrastructure

- Supply chain and logistics design

- Product engineering and technical architecture

- Customer data systems and regulatory environments

This distinction is critical. Exor does not succeed by forcing integration—it succeeds by understanding where integration is structurally valuable and where autonomy is essential.

Exor is not an isolated case. It is part of a broader shift in global capitalism, where holding companies, sovereign investors, and brand platforms are increasingly moving away from control-based structures toward influence-based systems.

This shift can be understood as the emergence of ecosystem capitalism—a model in which value is created not just by what a firm owns, but by what it enables across a network of semi-independent actors.

Several organisations illustrate different versions of this model, each with a distinct coordination mechanism.

Singapore’s Temasek Holdings, for example, represents a more structured version of ecosystem capitalism. Rather than relying on brand or heritage, Temasek acts as a convenor of intelligence. It brings leaders from across its portfolio together to share insights on AI, sustainability, digital transformation, and macroeconomic trends.

The emphasis is not on forcing collaboration, but on accelerating learning.

Tata … culture as the hidden architecture of collaboration

The Tata Group represents one of the most powerful examples of cultural rather than ownership-based coherence.

Unlike Exor, Tata is not primarily a financial platform. It is a deeply embedded institutional ecosystem, historically shaped by the Tata family and now governed through complex trust structures. Its influence does not rely on tight operational integration or centralised ownership control.

Instead, it is held together by what is often called the “Tata Way”—a shared philosophy emphasising integrity, nation-building, long-term value creation, and social responsibility.

This creates a different form of ecosystem logic. Tata companies such as Tata Consultancy Services, Tata Motors, Tata Steel, and Tata Consumer Products operate independently in very different industries. Yet they remain connected through shared values, leadership pipelines, and institutional memory.

Where collaboration works well in Tata

Tata’s ecosystem strength is most visible in areas where culture and scale matter:

- Brand trust and reputation (especially in domestic and emerging markets)

- Leadership development and succession systems

- Sustainability and social impact initiatives

- Digital transformation frameworks and capability building

- Selective procurement and shared sourcing advantages

- Crisis response and institutional coordination

Where collaboration is limited

But like all ecosystem models, Tata also has clear boundaries:

- Business model design (each company operates in structurally different industries)

- Customer-facing sales and distribution systems

- Product innovation pipelines and R&D

- Data systems and technology architectures

Tata demonstrates an important truth: cultural unity does not require operational integration. In fact, attempting to over-integrate would likely destroy the autonomy that makes each business competitive in its own market.

Virgin … brand as a coordination system without ownership depth

A very different model is found in Virgin Group.

Here, the coordination mechanism is not ownership or culture, but brand. Virgin has historically expanded across aviation, telecoms, financial services, hospitality, and space exploration through partnerships, licensing agreements, and joint ventures rather than majority control.

The Virgin brand acts as a permission system. It signals a set of expectations—customer obsession, disruption, simplicity, and challenger behaviour—that allow independently owned businesses to align around a shared identity.

Where collaboration works in Virgin-style ecosystems

- Brand positioning and customer experience design

- Marketing narrative and identity creation

- Entrepreneurial culture and innovation mindset

- Customer service philosophy and tone of voice

- Strategic storytelling and market entry framing

Where it does not work well

- Operational integration across businesses

- Shared IT systems or infrastructure

- Supply chain coordination

- Financial systems alignment

Virgin shows that identity can sometimes substitute for integration—but only in specific domains where meaning matters more than machinery.

The pattern … what actually works in collaboration ecosystems

Across the above companies, a consistent pattern emerges. Collaboration is highly valuable, but only in specific domains where knowledge can be transferred without operational integration.

High-value collaboration domains

- Leadership philosophy and governance

- Strategic thinking and capital allocation

- Brand and reputation systems

- Sustainability and ESG frameworks

- Talent development and executive networks

- Innovation mindset and experimentation approaches

- Macroeconomic and geopolitical insight

Low-value or high-friction collaboration domains

- Core operations and supply chains

- Product engineering and technical design

- Customer-facing sales execution

- Data systems and analytics infrastructure

- Regulatory and compliance environments

The boundary between these two categories is the most important strategic insight in ecosystem capitalism. The strongest holding companies are not those that maximise integration, but those that are precise about where integration creates value and where it destroys it.

From ownership to orchestration

What Exor and its peers reveal is a fundamental shift in the nature of corporate power. The most sophisticated holding companies are no longer defined by what they own, but by what they orchestrate.

They succeed not by centralising control, but by designing environments in which independent companies choose to collaborate. Influence replaces authority. Trust replaces hierarchy. Networks replace structure.

In this emerging model, the role of the holding company is no longer to act as an operator of assets, but as an architect of ecosystems—carefully shaping the conditions under which value can emerge across boundaries that ownership alone can no longer define.

I have spent more than two decades writing books.

From Marketing Genius in 2004, to the award-winning Gamechangers, and most recently Business Recoded, translated into more than 35 languages, books have shaped my career, my thinking, and much of my life.

I know intimately the emotional and intellectual investment that goes into writing a serious book. A good business book is not simply assembled. It is researched obsessively, argued internally, tested through conversations, refined through experience, and then painstakingly written, rewritten, and rewritten again.

Typically, it takes me two years to complete a book (I’ve written 10 of them, so far!). Somewhere between 60,000 and 80,000 carefully chosen words emerge from that process. Every paragraph matters. Every idea is shaped over many hours of thinking. Every story has a purpose. Like many authors, I feel deeply protective of those words because they represent not just content, but years of accumulated experience, curiosity, failures, travels, conversations, inspiration and conviction.

And yet, despite all of that, I am also an enthusiastic advocate for AI.

Not reluctantly. Not cautiously. Enthusiastically.

That may surprise some people in publishing circles today, where the prevailing mood often swings between anxiety and outrage. Much of the debate about AI and publishing has quickly become polarized. On one side sit the technology evangelists proclaiming the end of traditional publishing and the limitless possibilities of generative AI. On the other sit authors, publishers, and creatives warning, often rightly, about copyright abuse, stolen intellectual property, collapsing business models, and the erosion of human creativity.

This month’s Fortune cover article about David Shelley, CEO of Hachette Book Group and Hachette UK, captures this tension powerfully. He argues passionately that publishers must defend authors against AI companies training models on copyrighted works without permission. He calls the current approach by some technology firms “parasitic” and warns that without sustainable economics for creators, society risks starving itself of future stories, ideas, and art.

He is right to raise the alarm. But I also believe there is another equally important conversation we need to have, one that moves beyond fear, beyond legal trench warfare, and beyond simply trying to preserve the publishing industry exactly as it is today.

Because while copyright matters enormously, readers matter too.

And readers are changing faster than publishing.

Publishing’s resistance to change

For decades, publishing has largely resisted radical reinvention. Yes, we have ebooks. Yes, we have audiobooks. But let us be honest: most digital publishing innovations have essentially reproduced the same linear content in slightly different formats. The core model remains remarkably unchanged. An author writes a long manuscript. A publisher packages it. A reader buys it. The reader consumes it sequentially from beginning to end.

That model worked brilliantly in a slower, less connected, less information-saturated world.

But today’s world is fundamentally different. Business leaders no longer consume knowledge in the same way. Nor do students. Nor do entrepreneurs. Nor do consumers generally. People increasingly seek modular knowledge, contextual insight, adaptive learning, real-time relevance, personalized recommendations, conversational exploration, multimedia engagement, and practical application.

In other words, people increasingly want knowledge to behave more like a living system than a static product.

The uncomfortable truth for publishing is that a 70,000-word book can often be an extraordinarily inefficient way to access a specific idea.

Imagine a CEO facing a strategic challenge in Indonesia next Tuesday morning. Does she really want to read an entire 300-page business book cover to cover to extract the three ideas most relevant to her immediate context? Or would she prefer a dynamic, adaptive knowledge experience that understands her market, her company, her industry pressures, and her preferred learning style?

That is not a threat to ideas. It is an evolution in how ideas travel.

This is why I believe AI, used wisely and ethically, could become one of the most important opportunities publishing has seen in generations. Not because AI should replace authors, but because AI could dramatically amplify the reach, usefulness, accessibility, and impact of human ideas.

The real question is not how to stop AI

As co-founder and host of the Future Book Forum held in Munich, where I engage every year with around 300 publishers from across the world, I see firsthand how deeply the industry cares about books. And rightly so. Books are beautiful objects. They carry emotional significance. They slow us down. They demand immersion. They reward contemplation. In a fragmented digital world, the physical book retains extraordinary cultural power.

But sentimentality alone is not a strategy.

Every industry today is being reshaped by changing technologies and changing human behaviour. Retail, banking, healthcare, automotive, media, education, hospitality — none can survive merely by protecting legacy formats. The winners are those who reimagine how they create value for people.

Publishing will be no different.

The key question is therefore not: “How do we stop AI?”

The key question is: “How do we reinvent knowledge?”

That distinction matters enormously. Because if we approach AI purely defensively, publishing risks becoming trapped in a nostalgic battle to preserve an increasingly outdated delivery model. But if we approach AI creatively, strategically, and humanistically, publishing could enter a remarkable new era.

From static books to living knowledge

Consider what becomes possible.

Imagine business books transformed into intelligent advisory systems that adapt insights dynamically for different industries, cultures, or business sizes. Imagine cookbooks that become interactive culinary companions, adapting recipes to dietary preferences, available ingredients, health goals, and skill levels. Imagine fitness books evolving into adaptive coaching systems that respond to age, injuries, schedules, biometric feedback, and motivation patterns.

The core intellectual property remains human. The ideas remain human. The expertise remains human.

But AI allows those ideas to become more useful.

This is not hypothetical. Consumers already expect personalization everywhere else. Netflix personalizes entertainment. Spotify personalizes music. TikTok personalizes discovery. Amazon personalizes commerce. Increasingly, people expect knowledge itself to become adaptive.

And frankly, they are right to expect it.

One of the great ironies of publishing is that we have often celebrated the democratization of knowledge while simultaneously clinging to highly inflexible formats for delivering it.

Books are magnificent containers for ideas. But they are still containers. AI potentially allows ideas to escape the container.

That should excite us.

Protecting authors while expanding impact

Of course, legitimate concerns remain.

Copyright absolutely matters. Consent matters. Attribution matters. Compensation matters. Transparency matters. If AI companies simply scrape authors’ work without permission or remuneration, then authors are right to object. Human creativity requires sustainable economics.

As David Shelley argues in the Fortune article, if creators cannot make a living, eventually the entire creative ecosystem weakens. But there is also a danger that the publishing world frames the debate too narrowly around ownership instead of usefulness.

The deeper opportunity is not simply to protect content. It is to expand impact.

As authors, surely our ultimate ambition is not merely to defend pages. It is to help people.

When I write about innovation, leadership, reinvention, strategy, or future business models, my real goal is not that somebody finishes Chapter 7. My goal is that they transform their business, challenge assumptions, create opportunities, inspire teams, and build a better future.

If AI helps those ideas reach more people more effectively, then I am interested.

Throughout history, publishing has always evolved through technological shifts. The printing press itself was once controversial. Paperbacks were dismissed as inferior. Radio threatened books. Television threatened reading. The internet threatened everything. Yet every technological wave ultimately expanded access to ideas.

AI will do the same — but only if the industry chooses reinvention over resistance.

Why human creativity matters more than ever

Importantly, embracing AI does not mean surrendering human creativity.

In fact, paradoxically, AI may increase the value of authentic human insight. As generative content floods the world, originality becomes more valuable, not less. Trust becomes more valuable. Experience becomes more valuable. Perspective becomes more valuable.

In a world of infinite synthetic content, people will increasingly seek what some are already calling the “human premium.”

That is actually good news for serious authors.

Because the best books are never simply information products. They are expressions of lived perspective. They connect ideas in unexpected ways. They challenge assumptions emotionally and intellectually. They capture nuance, contradiction, ambiguity, aspiration, and imagination.

AI can synthesize patterns. Humans create meaning.

The future therefore is unlikely to be humans versus AI. It is far more likely to be humans amplified by AI.

And publishers have an extraordinary opportunity to lead that future.

Reinventing the role of the publisher

Imagine publishers evolving from distributors of static products into orchestrators of dynamic knowledge ecosystems. Imagine subscription-based intelligence platforms built around authors. Imagine AI companions trained ethically and transparently on licensed author content. Imagine publishers monetizing not just book sales, but adaptive learning experiences, expert networks, real-time insights, simulations, coaching systems, and community engagement.

That is not the destruction of publishing.

That is the expansion of publishing.

Some publishers already understand this. The smartest conversations I hear at Future Book Forum are no longer about defending old formats. They are about reimagining the role of publishers in a world where knowledge flows differently.

Publishers still have enormous strengths — trust, curation, editorial quality, brand reputation, author relationships, discovery, distribution, communities, and intellectual rigor. But those strengths need to be applied to future models, not merely legacy ones.

Technology companies also need to engage differently. The current conflict between publishers and AI firms is understandable but unsustainable. Endless litigation may establish important legal precedents, but it will not create the future alone. Ultimately, publishers and technology companies will need each other.

The more enlightened path is partnership.

Transparent licensing models. Revenue-sharing systems. Author-controlled permissions. Attribution frameworks. Ethical training protocols. Consumer transparency. Shared innovation labs. New monetization architectures.

This is solvable.

And there are encouraging signs already emerging. Some AI companies are beginning to negotiate licensing agreements with publishers and media organizations. Others are exploring attribution systems. The legal framework will evolve. Business models will evolve. Consumer expectations will evolve.

They always do.

The bigger risk is irrelevance