OXXO Future Makers: Moonshots, Dual Thinking, and Courage

March 18, 2026 at Online Webinar

- Future Makers by Peter Fisk

- Megatrends 2035 by Peter Fisk

- Reinventing Strategy by Peter Fisk

- The Dual OS of Business by Peter Fisk

OXXO is Mexico’s largest convenience store chain and a cornerstone of Fomento Económico Mexicano (FEMSA). Founded in 1978 in Monterrey, it pioneered the modern small-format, high-frequency retail model, often referred to locally as tiendas de proximidad. Today, OXXO operates over 24,000 stores across Mexico and Latin America, serving millions of daily customers with food, beverages, essentials, and services.

Business Model and Core Strategy

OXXO’s success rests on three pillars: convenience, scale, and accessibility. Stores are strategically located near homes, workplaces, transit points, and high-traffic areas. The product mix is broad, spanning snacks, beverages, daily essentials, and prepared foods designed to meet multiple trip motivations—from quick purchases to routine shopping. Beyond retail goods, OXXO provides bill payments, phone recharges, deposits, and remittances through partner financial services, effectively turning its stores into community touchpoints.

FEMSA leverages OXXO’s size as a competitive advantage, combining extensive geographic coverage with data-driven decisions on store openings, closures, and inventory management. Its direct distribution network allows tight control over stock, localized offers, and logistical efficiency, creating a formidable moat against competitors.

Growth and Innovation

OXXO continues to expand both physically and digitally. FEMSA has committed substantial investments to the Proximity division, aiming to add over a thousand new stores and explore alternative formats, including campuses and industrial sites. These locations target high-footfall, niche markets to complement OXXO’s existing footprint.

Digital transformation is central to OXXO’s strategy. Advanced merchandising, forecasting, and supply-chain systems enhance inventory management and demand planning. Artificial intelligence and customer data tools are used to personalize marketing, optimize product placement, and improve loyalty programs. Store experience innovation includes digital signage, self-checkout kiosks, automated pricing, and modern coffee services, all designed to deliver faster, more engaging experiences.

Financial services also play a key role. OXXO integrates payment solutions through platforms like OXXO PAY, enabling cash payments for online transactions, while partnerships with digital banks facilitate deposits and withdrawals. This approach positions OXXO not just as a retailer but as a local financial hub.

Changing Consumers and Trends

OXXO’s consumer base is evolving rapidly. Young, urban customers increasingly prioritize speed, convenience, and digital integration. Expanding middle-class spending and busier lifestyles drive more frequent, small-basket purchases rather than traditional weekly trips, favoring convenience formats. The majority of OXXO’s shoppers fall within the 15–35 age bracket, highlighting its appeal among younger, digitally engaged populations.

Competitive Landscape

OXXO operates in a highly competitive retail environment. Direct rivals include international convenience chains such as 7-Eleven and Circle K, as well as regional chains like Tiendas D1, Ara, OK Market, and Tambo Mas. Broader competition comes from supermarkets and hypermarkets including Walmart, H-E-B, Chedraui, and Soriana, as well as digital platforms offering quick food and beverage delivery. OXXO has also begun entering the U.S. market, competing with local chains in select regions.

Future Opportunities

Beyond its current plans, OXXO has significant opportunities to expand its ecosystem, reach new audiences, and diversify services:

Evolving into a Full Ecosystem

OXXO could leverage its unparalleled store network and data to move beyond traditional convenience retail into a multi-service ecosystem combining retail, financial services, logistics, and digital engagement:

-

Digital wallet and super-app: Integrating OXXO PAY with loyalty, microloans, and subscription services could turn stores into digital commerce hubs.

-

Data-driven personalization: AI-powered insights could enable tailored offers, bundles, and promotions to increase basket size and retention.

-

Marketplace partnerships: Stores could act as offline pick-up and drop-off points for e-commerce platforms and smaller local merchants.

Global inspiration: Japan’s 7-Eleven integrates logistics, bill payments, and online order collection. In China, Alibaba’s Hema stores combine offline and digital ecosystems for food, delivery, and loyalty.

New Formats and Hybrid Models

-

Urban micro-stores: Automated kiosks or modular units in dense areas could operate 24/7 with robotics and self-checkout.

-

Community hubs: Larger “experience stores” could combine groceries, coffee, co-working, and digital services to attract young professionals.

-

Pop-up or seasonal stores: Temporary locations at events, universities, or office complexes could reach new audiences.

-

Mobility hubs: Hybrid gas-and-retail stations with EV charging and micromobility services.

Global inspiration: Amazon Go and Tesco Express experiment with micro-format stores, automation, and hybrid services. Circle K in Europe combines retail with EV charging.

Adjacent Services Beyond Retail

-

Health and wellness: Pharmacies, telemedicine kiosks, or healthy food options could attract health-conscious or aging populations.

-

Financial services: Expansion of microloans, insurance products, and remittance services could deepen engagement with urban and rural populations.

-

Education and government services: Stores could act as access points for online education, government registrations, and other digital services.

Global inspiration: India’s Paytm Partner Stores integrate payments, bill collection, and financial services into convenience networks. Brazilian fintechs collaborate with retail chains to reach underserved populations.

New Audiences

-

Generation Z and Gen Alpha: Hyper-connected youth may respond to gamified shopping, social commerce, and app-integrated loyalty.

-

Rural and suburban populations: Mobile or modular stores could reach underserved areas, combining retail and essential services.

-

Travelers and tourists: Strategic airport, transit, or hospitality locations could leverage OXXO’s brand while delivering region-specific convenience.

Technology-Driven Experiences

-

AI and robotics: Automated inventory, smart shelves, and cashierless experiences to reduce costs and improve speed.

-

Augmented reality (AR): Gamified promotions or interactive product information.

-

Smart logistics: Predictive analytics, drone delivery, or micro-fulfillment centers integrated with stores.

Global inspiration: JD.com in China uses autonomous deliveries and AI-powered stocking for micro-stores. Amazon Fresh experiments with AR in concept stores.

Sustainability and Green Retail

-

Circular economy services: Package returns, recycling points, or refill stations.

-

EV charging hubs: Pairing retail with sustainable mobility.

-

Sustainable products: Eco-friendly SKUs, local sourcing, or zero-waste initiatives.

Global inspiration: 7-Eleven Japan and Circle K Europe test green retail models with sustainability and convenience combined.

Strategic Outlook

OXXO’s future innovation could transform it from a convenience store network into a retail + services ecosystem. By integrating new store formats, hybrid models, adjacent services, digital platforms, and sustainability initiatives, OXXO can:

-

Engage new demographics including younger, urban, and underserved populations.

-

Monetize its massive footprint and customer data in innovative ways.

-

Maintain a competitive edge against both global and local players through ecosystem-driven customer relationships.

Ultimately, OXXO has the potential to become a centralized, hyper-localized, digitally integrated service hub, combining retail, financial, and community services. By drawing inspiration from global leaders in convenience and digital ecosystems while tailoring solutions for Mexican and Latin American markets, OXXO could redefine the future of convenience retail in the region.

Proximity store trends

“Proximity retail” refers to small, local stores positioned close to where people live and work — often within walking distance — and deeply integrated into daily routines. These aren’t just “corner shops”; they are bridging physical and digital channels and evolving to serve multiple consumer needs beyond traditional convenience purchases.

Convenience + Speed + Relevance = Growth:

-

Shorter shopping missions and frequent visits translate to higher unit sales.

-

Digital integration captures customers across channels.

-

Local fulfilment capabilities differentiate them from traditional retail or pure ecommerce.

-

Service expansion (food, healthcare, pickups, EV charging, parcel logistics) creates multiple revenue streams.

This trend mirrors broader societal shifts toward 15‑minute cities, where essential services are easily accessible without long travel. Retailers are adapting by opening compact urban formats in neighbourhoods, campuses, transit hubs and mixed‑use developments, betting on foot traffic and frequent visits.

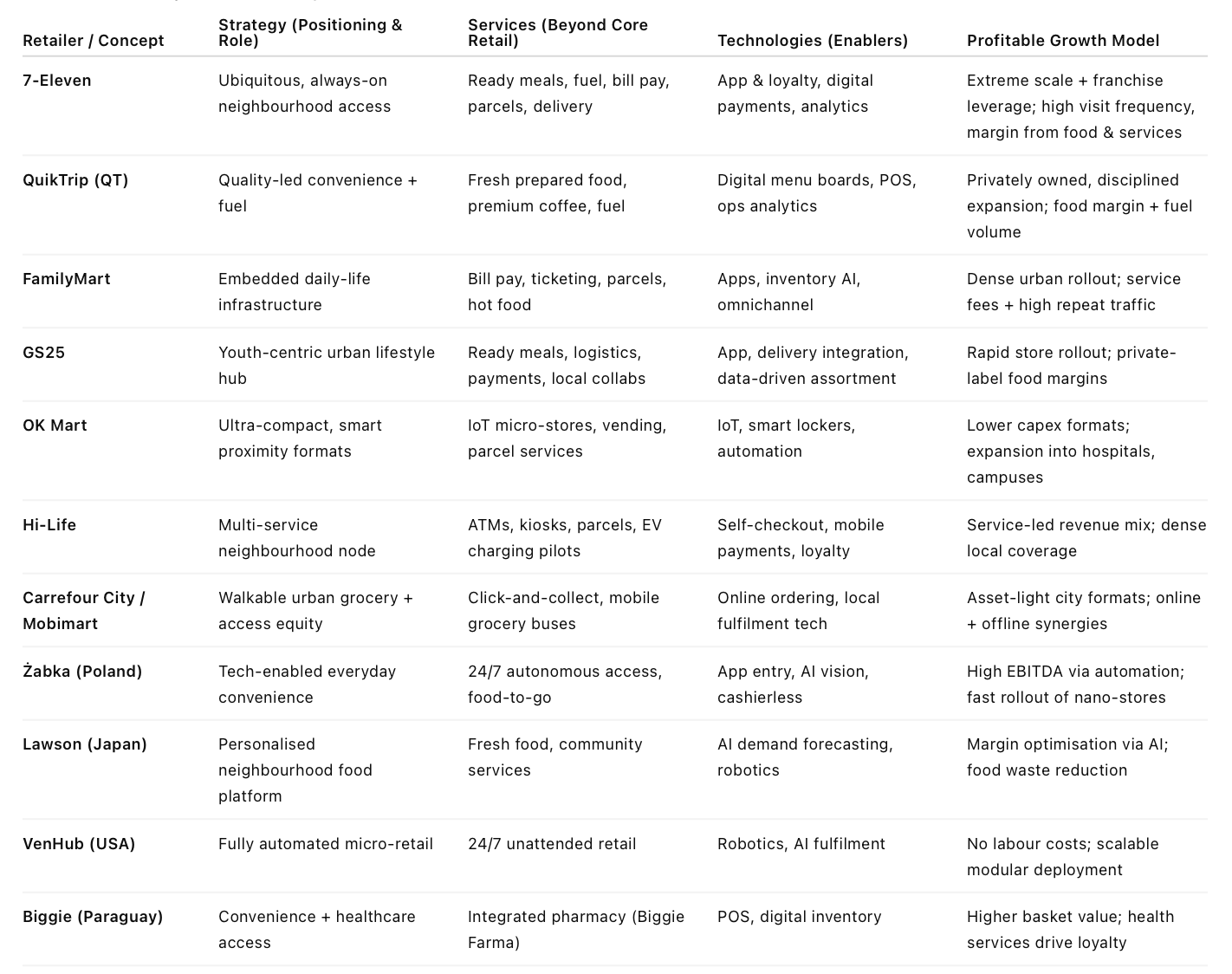

A great example are the Taiwanese “konbini ecosystem” (7‑Eleven, FamilyMart, OK Mart). These convenience stores have evolved far beyond snacks — offering bill payments, ticketing, government services, parcel services, and even gyms in some outlets, making them civic and lifestyle hubs in dense urban areas. Chains also test mobile convenience stores and cashless vending networks.

1. Omnichannel Integration

Modern proximity stores are deeply linked with online platforms. Customers can:

-

Order online and use click‑and‑collect / BOPIS.

-

Get home delivery or express delivery from nearby inventory.

-

See real‑time stock online before heading to store.

This seamless digital‑physical experience boosts loyalty and sales by meeting shoppers where they are.

2. Stores as Fulfilment Hubs

Rather than just selling in‑store, proximity stores increasingly serve as micro fulfilment and logistics nodes:

-

Filling online orders locally rather than from distant warehouses.

-

Reducing delivery times (often to minutes) and last‑mile costs.

-

Using local inventory to balance online and in‑store demand.

This “store‑as‑hub” model boosts efficiency and increases overall traffic.

3. Elevated Food and Services

Foodservice and meal solutions now anchor many proximity formats:

-

Fresh, ready‑to‑eat meals and quality coffee can rival quick‑service restaurants.

-

Stores become places where people eat, meet, and linger, not just grab items.

Some neighbourhood shops even add community services like parcel collection, pharmacy counters, or seating spaces, enhancing local relevance.

4. Tech‑Enabled Efficiency

Retailers are using tech to elevate performance and convenience:

-

Cashierless checkout, mobile POS, and self‑checkout to cut friction.

-

Real‑time inventory systems and AI forecasting to reduce waste and stockouts.

-

Digital signage, apps, and loyalty integration for personalised experiences.

What’s Next?

5. Personalisation at the Edge

Use local data and apps to tailor offers, promotions and stock mixes specific to neighbourhood needs.

6. Micro‑Service Hubs

Add services like telehealth kiosks, community lockers, charging stations, coworking nooks, laundromats or bike repair points, deepening daily relevance.

7. Sustainability and Community

Offer bulk/local goods, refill stations, green delivery options, and waste‑reduction programmes to connect with values‑driven consumers.

8. Partner‑Driven Ecosystems

Integrate with last‑mile couriers, local producers, food brands and logistics partners to expand reach and reduce costs.

Established convenience stores

7‑Eleven – Founded in 1927 in Dallas, Texas, as the Southland Ice Company, 7‑Eleven pioneered extended‑hours retail, renaming itself in 1946 to reflect 7 am–11 pm opening times. It expanded via franchising and international licensing, becoming the world’s largest convenience-store chain with over 85,000 locations in more than 20 countries. Its strategy centers on ubiquitous, quick access to grab‑and‑go foods, beverages, and services such as fuel and bill payment. 7‑Eleven has innovated with fresh food, Slurpee drinks, mobile apps, and delivery services. Growth has been driven by both acquisitions and organic expansion, though profitability varies regionally.

QuikTrip (QT) – Founded in 1958 in Tulsa, Oklahoma, by Burt Holmes and Chester Cadieux, QuikTrip was inspired by early 7‑Eleven stores. QT combines convenience retail with high-quality prepared foods, coffee, fuel, and strong customer service. The brand emphasizes clean, spacious stores and fresh offerings, earning loyal customers. Growth has been consistent, with the company remaining privately held by the Cadieux family and reporting revenues around US $14 billion, reflecting strong regional penetration and operational efficiency.

Constructor – Founded in 2015 in San Francisco by Eli Finkelshteyn and Dan McCormick, Constructor is an ecommerce technology company specialising in AI-powered product search and discovery. Its strategy enhances online retail by personalising search, recommendations, and discovery experiences to drive higher conversions for clients. Innovations include AI shopping assistants and advanced product discovery tools. Constructor has grown rapidly, doubling revenue consecutively and scaling client interactions globally, establishing itself as a profitable, fast-growing ecommerce tech leader.

GS25 – GS25 is a South Korean convenience store chain operated by GS Retail, founded in 1990 (initially as LG25) and later rebranded. Headquartered in Seoul, it has thousands of outlets nationwide. Its strategy focuses on dense local coverage and a broad mix of ready-to-eat meals, beverages, and everyday items tailored to Korean tastes. GS25 innovates with local snack and beverage offerings and loyalty programmes. Expansion into Vietnam and Mongolia complements its domestic dominance, contributing to the parent company’s strong retail profitability.

Freshippo (Hema Fresh) – Launched in 2015 by Alibaba in China, Freshippo integrates online and offline grocery retail. It blends digital ordering with physical supermarkets, offering rapid 30-minute delivery within local zones. Its strategy focuses on fresh foods, app-driven shopping, and real-time inventory. Innovations include data-driven fulfilment, mobile payments, and stores serving both walk-in and online customers. Its hyper-local, technology-driven model has fueled rapid expansion in Chinese cities and strong profitability tied to fresh produce and delivery services.

Spar – Founded in the Netherlands in 1932 by Adriaan van Well, Spar started as a cooperative of independent retailers and expanded internationally. Its strategy combines neighbourhood convenience with a flexible franchise/licence model, allowing local shops to operate under the SPAR brand while benefiting from shared supply and logistics. Innovations include integrated fresh offerings and multi-format retail such as SPAR Express. With nearly 14,000 outlets worldwide and €43.5 billion in sales, SPAR continues to grow through licensing, partnerships, and local market adaptation.

Jio / JioMart – Launched in India in 2019 by Reliance Retail, JioMart is an ecommerce and quick-commerce platform rather than a traditional convenience store. Its strategy leverages Reliance’s physical network and digital brand to provide fast delivery of groceries and essentials, competing with established grocery retailers. Innovations include hyper-local delivery through “dark stores” and integration with telecom and digital infrastructure. JioMart has grown rapidly across thousands of Indian pin codes, achieving strong order volumes and establishing itself as a high-velocity digital convenience solution.

Innovative proximity stores

FamilyMart (Global – Japan/Asia) FamilyMart began in 1973 in Japan and has grown into one of the world’s largest convenience chains with thousands of stores across Asia. Its proximity strategy focuses on dense urban and residential locations with fresh food, ready meals, premium coffee, and everyday essentials targeted at busy neighbourhoods. In Thailand and other markets it’s trialling in‑building micro stores (e.g., in condos) to embed itself in daily life. FamilyMart also experiments with experiential formats blending lifestyle and community elements with retail offerings. This localised, convenience‑plus concept drives both footfall and loyalty across markets.

OK Mart (Taiwan) – Founded in 1988 in Taipei, OK Mart has expanded to hundreds of locations across Taiwan. Its strategy blends traditional convenience retail with smart, compact formats (OKmini) that use IoT and vending technology for places like hospitals, schools or transit hubs. OK Mart emphasises hot food, local snacks, and logistics partnerships (e.g., with Shopee) to drive foot traffic and deliveries, positioning stores as mini‑community nodes with lower rents and strong neighbourhood penetration.

Hi‑Life (Taiwan) – Hi‑Life started in 1988 in Taipei and has grown to over 1,500 stores by 2025. While rooted in food, drinks, and daily essentials, Hi‑Life innovates with digital kiosks, mobile payments, service integrations (like ATM and EV charging), and online shopping features. Its flagship stores offer multiple services beyond groceries, including digital retail options and partnerships, turning each site into a multi‑purpose local hub.

Carrefour City (Europe/MENA) – Launched by Carrefour Group in 2009, Carrefour City has nearly 9,000 small‑format urban stores in Europe and the UAE, focusing on walkable neighbourhood convenience with fresh foods and meal solutions. While predominantly food retail, the concept also serves as a local delivery and fulfilment node for online orders and trialled mobile grocery buses (Mobimart) to underserved neighbourhoods, reinforcing its local anchor role.

Biggie (Paraguay) – Founded in 2013 in Paraguay as a 24‑hour convenience store chain, Biggie now operates 260+ stores and has introduced Biggie Farma, a combined pharmacy‑convenience format. Its strategy centres on extended hours, community accessibility, and pharmacy integration, providing both everyday purchases and health‑oriented services in neighbourhood contexts. This diversification strengthens its relevance as a daily destination.

ExtraMile (USA) – Launched in 2018 as a Chevron‑linked convenience franchise, ExtraMile has grown to over 1,100 locations in the U.S. West and Southwest. While fuel remains a core traffic driver, the brand emphasises fresh food, quick meals, and expanded in‑store services, and is planning further expansion to strengthen its neighbourhood footprint. Its growth is tied to leveraging branded fuel sites for broader retail and convenience offerings.

CU (South Korea) – CU is transforming stores into community lifestyle hubs with enhanced food‑to‑go counters, self‑order kiosks, café‑style seating, and zones for local specialities. This shifts proximity stores into all‑day multi‑occasion destinations beyond quick purchases.

Żabka (Poland) – Żabka has rolled out autonomous micro‑stores that operate 24/7, letting customers enter and check out via mobile app or cards with AI‑enabled systems, blending staffed daytime retail with automated night access.

Carrefour City & Mobimart (France/MENA) – Carrefour’s City format standardises local urban convenience stores in dense city centres. Its Mobimart concept — a moving grocery bus — brings fresh food to underserved areas, pushing proximity retail into mobile neighbourhood services.

VenHub (USA) – A fully automated, robotic‑managed convenience store network where AI‑driven systems pick and deliver products without staff. These walkable, 24/7 units are designed for high‑traffic neighbourhood settings and app‑driven ordering.

Robomart (USA, Concept) – Robomart isn’t a store chain per se, but a fleet of autonomous smart shops that can be deployed by retailers to bring products directly to neighbourhood streets or gated communities. It’s a white‑label platform for micro‑retail at lower real‑estate cost.

Lawson (Japan) – Lawson is innovating with AI systems that tailor ordering and inventory to weather, local demand and customer behaviour, and trials semi‑automated cooking kitchens and robot assistants to streamline operations and expand warm‑food offerings.