What happened to sustainability? … from corporate rallying cry, to quiet embedded reality … and why it matters more than ever

January 5, 2026

There was a moment — not so long ago — when sustainability felt unstoppable.

It was the shining topic on the covers of business magazines, a headline on every CEO’s quotes page, and the go‑to strategy theme for keynote speeches at global forums. Boards asked for ESG reports. Investors interrogated climate risk. Marketers plastered climate pledges on websites. For a time, sustainability looked like the new centrepiece of business purpose — a narrative that business and society could rally around.

Yet today, if you tune into the corporate discourse, something feels different. Renewed questions are emerging: Has sustainability lost its way? Was it just a fad? Have politicians and sceptics pulled the pendulum back? Does it still matter? Or is it quietly becoming business as usual — less hyped, but more embedded?

The short answer is this: sustainability has evolved, not faded.

Its early years were about visibility and aspiration. What’s happening now is deeper and harder: integration, strategy, systemic transformation, and measurable impact. And in a world increasingly shaped by climate extremes, resource scarcity and social divides, sustainability matters not less, but more than ever.

Sustainability, beyond the hype

To see sustainability as a transient trend is to misunderstand its nature. Sustainability was never about buzzwords or marketing soliloquies. It was — and remains — a response to biophysical realities that are measurable, accelerating and economically material.

Climate change

Global average temperatures have risen by more than 1.2°C above pre‑industrial levels — a threshold scientists warned was perilously close to severe climate disruption. The Intergovernmental Panel on Climate Change (IPCC) projects a world of increasingly frequent and severe weather events: heatwaves, floods, storms, wildfires and droughts that disrupt communities, supply chains and economies.

In 2022 alone, insured losses from climate‑related disasters exceeded US$165 billion, underscoring that climate risk is not a distant future — it is economic reality today. For businesses, these risks translate into damaged infrastructure, interrupted operations, higher insurance costs, and volatile supply networks.

Resource depletion

Biodiversity loss is accelerating. The World Wildlife Fund’s Living Planet Report documented an average 60% decline in vertebrate populations since 1970 — a stark indicator of ecosystem stress. This matters for industries from agriculture (pollination services) to fisheries (marine stocks) and pharmaceuticals (natural product discoveries).

Water scarcity now affects nearly half of the global population, with regions from California to China reporting chronic shortages. Industries that rely on water — from textiles to semiconductors — face physical and operational stress that can’t be ignored.

Inequality

In many advanced economies, wealth concentration has risen sharply. Inequality impacts labour markets, consumer demand, public health, and social cohesion — all of which affect business stability and growth. Companies increasingly recognise that social sustainability – fair wages, inclusive workplaces, supply‑chain labour standards – is not “nice to have,” but a core dimension of risk and reputation.

These are not narratives created in boardrooms; they are empirically verifiable, globally observed trends with direct relevance to commercial performance.

Sustainability, made real

The early 2020s were characterised by ambitious language — net‑zero pledges, climate commitments, and ESG scorecards. But the recent phase is about implementation at scale: embedding sustainability into everyday decisions, capital allocation, product design, and organisational architecture.

The transition from aspiration to execution is harder and less glamorous, but also more meaningful.

Consider these companies:

Ørsted … from coal to wind

Once a coal and oil‑heavy utility, Ørsted pivoted its entire business to become a global leader in offshore wind. That transformation meant divesting fossil assets, retraining workers, reconfiguring capital expenditure — a true operational overhaul. The result? Ørsted is now one of the world’s largest developers of offshore wind capacity, positioning itself at the centre of the global energy transition. This wasn’t a PR exercise, it was strategic reinvention that changed how energy is produced and financed.

Neste … from refining to renewables

Neste shifted from conventional oil refining to become one of the world’s largest producers of sustainable aviation fuel and renewable diesel. Sustainable aviation fuel is a critical pathway for decarbonising air transport — arguably one of the hardest sectors to electrify. Neste’s transformation showcases sustainability as a source of competitive advantage in industrial markets, not simply a compliance task.

Schneider Electric … from products to systems

France’s Schneider Electric is not household sustainability brands in the way Patagonia or Tesla might be, yet they are critical enablers of decarbonisation. Once a mere energy equipment manufacturer, it now focuses on energy efficiency, automation, and smart grid infrastructure in sectors ranging from manufacturing to buildings to utilities. This is sustainability at scale — systems level, not token product lines.

ESG metrics are not enough

In recent years, headlines have highlighted scepticism about ESG — environmental, social and governance metrics — with critics calling it a marketing fad, providing inconsistent ratings, or even politicising investment. These critiques are not worthless, but they often miss a core truth: ESG is a dashboard, not a strategy.

ESG is not a strategy

ESG ratings aggregators score companies on dozens of indicators — from board diversity to carbon intensity. But a high ESG score doesn’t inherently describe strategic reinvention. A company might have strong governance policies, impressive board diversity and robust social practices — but still be fundamentally misaligned with a low‑carbon, resource‑constrained future if its core business model depends on fossil fuels or unsustainable inputs.

ESG ratings are inconsistent

Different ESG ratings often produce divergent assessments for the same company, underscoring the limits of current methodologies. This reveals not that sustainability is irrelevant, but that measurement frameworks need evolution — towards transparency, standardisation and outcomes‑focused reporting.

ESG doesn’t tell you what to do next

A sustainability score doesn’t inherently suggest how to transform your business model. That requires strategy, innovation, capital allocation shifts and disciplined execution. This is why companies that go beyond ESG — embedding sustainability into the core of their business strategies — are the ones that drive commercial performance while managing risk.

New consumer expectations

Consumer behaviour offers another lens on sustainability’s evolution.

In the early 2020s, surveys repeatedly showed that consumers said they wanted sustainable products. Yet purchase behaviour sometimes told a different story: price, convenience and brand familiarity often dominated decisions.

But consumer orientation has shifted — not through slogans, but through lived experience, information access, and cultural change.

Sustainable purchasing is a baseline expection

What was once aspirational is increasingly expected:

-

Fast fashion’s reckoning: Brands like H&M and Zara were early to adopt “sustainable collections,” but they still operate high‑volume, low‑margin models that generate massive waste. As consumers become more educated, criticisms of fast fashion are not just about individual garments but about business models that rely on overconsumption. This tension has fuelled growth in clothing resale marketplaces, rental platforms (like Vestiaire Collective) and repair services.

-

Plant‑based and alternative proteins: Companies like Beyond Meat and Oatly helped pioneer the alternative‑protein movement. Once niche, plant‑based options are now mainstream in grocery aisles and on menus globally. Traditional meat producers are adapting too — diversifying portfolios with plant‑based alternatives, reflecting shifting demand patterns.

-

Home energy choices: With rising energy costs and increasing climate awareness, many households are adopting rooftop solar, heat pumps, EVs, and smart home energy systems. These are not symbolic choices — they reflect real capital allocation decisions that reshape energy demand patterns.

Consumers are no longer merely signalling sustainability preferences; they are acting on them. And that behavioural change is cumulative, not ephemeral.

Investor risk and opportunity

Investor attitudes reveal another vital evolution.

Early excitement about ESG often had elements of hype — with some asset managers marketing “sustainable portfolios” that looked a lot like traditional ones with a green label. But as markets have matured, so has investor sophistication.

What investors increasingly recognise is this: climate and sustainability are financial imperatives, not optional preferences.

Climate risk is financial risk

Physical risks (floods, fires, droughts) and transition risks (policy shifts, carbon pricing, stranded assets) directly affect company valuations and debt pricing. Ignoring these risks is not just irresponsible — it is financially imprudent.

Asset managers, pension funds, insurers and sovereign wealth funds are integrating climate risk into portfolio construction because they see that companies unprepared for the transition are more likely to face:

- Higher capital costs

- Stranded assets

- Market share erosion

- Regulatory penalties

Capital flows are shifting

While political pushback has surfaced in some markets — particularly in debates around prioritising short‑term economic objectives over climate goals — many institutional investors remain committed to integrating sustainability into risk assessments because the data supports it.

Examples include:

-

BlackRock, the world’s largest asset manager, continues to factor climate risk into investment analysis and calls for improved disclosure because its clients demand resilience and long‑term returns — not greenwashing.

-

European institutional investors often reference both regulatory requirements and performance data showing that decarbonised portfolios outperform peers over long horizons, particularly as energy transitions reshape entire sectors.

The criticism of ESG has, in many ways, triggered a necessary evolution: from checklist metrics to integrated, decision‑centric analysis. Quality matters. Transparency matters. Standardisation matters. And investors are demanding all three.

Sustainability driving innovation and growth

Here is where the myth of sustainability’s “decline” collapses under the weight of real evidence: companies that embed sustainability deeply into their strategy are not merely surviving — many are thriving commercially.

Below are examples from diverse sectors proving this point.

Microsoft … sustainability as innovation engine

Microsoft committed to becoming carbon negative by 2030 and to removing all historical emissions by 2050 — a bold standard that goes beyond net zero. But beyond commitment, Microsoft has integrated sustainability into its core offerings.

The company has developed cloud‑based tools that help customers track and reduce emissions, and its sustainability solutions are now a critical differentiator in enterprise sales. What was once “corporate responsibility” has become a growth vector for revenue through new product suites.

Unilever … sustainable living drives growth

Unilever’s “Sustainable Living” Brands — those with strong social and environmental propositions — have consistently outpaced the company’s average growth rate, contributing disproportionate revenue growth, stronger margins, and greater market share.

This is not anecdotal. Unilever publishes evidence showing that brands with demonstrable sustainability credentials drive both consumer demand and financial performance.

Patagonia … authenticity as competitive advantage

Patagonia’s mission — “We’re in business to save our home planet” — is not marketing fluff. The company invests in environmental activism, promotes product repairs over disposables, and even turned down sales during economic downturns to prioritise values.

The result? Unusually high customer loyalty, premium pricing power, and profitability that has outpaced many peers in outdoor apparel — all anchored in authenticity.

IKEA … circularity and operational resilience

IKEA’s goal to become climate positive by 2030 — meaning it will reduce more greenhouse gas emissions than its entire value chain emits — is ambitious. It has invested billions in renewables, developed circular products designed for reuse, and incorporated sustainability into its supply chain.

Strategically, this boosts operational resilience (lower energy costs, stable raw‑material sourcing) and brand strength, especially among consumers who prioritise values as a purchasing criterion.

L’Oréal … beauty meets sustainability

L’Oréal’s “L’Oréal for the Future” programme integrates carbon, water, biodiversity and equality goals, tying sustainability performance to executive compensation. Its brands with strong environmental credentials — particularly in clean and premium beauty segments — have outperformed category averages, revealing that sustainability can be a differentiator in consumer markets where choice and values matter.

Schneider Electric and Siemens … infrastructure at scale

These industrial giants embed energy efficiency, electrification, and smart automation into their offerings. Their products are not labelled “sustainable” in a marketing sense; they are sustainability leverage points for entire industries. Demand for smart grids, digital infrastructure and decarbonised systems continues to grow — and these companies are the backbone of that transition.

NextEra Energy & Vestas … renewable capital

NextEra Energy — a major clean energy producer — and Vestas — a leading wind turbine maker — demonstrate that capital markets are willing to reward companies aligned with the energy transition with higher valuations relative to legacy fossil fuel peers. Investors increasingly price future earnings potential tied to renewable growth, rather than historical carbon intensity.

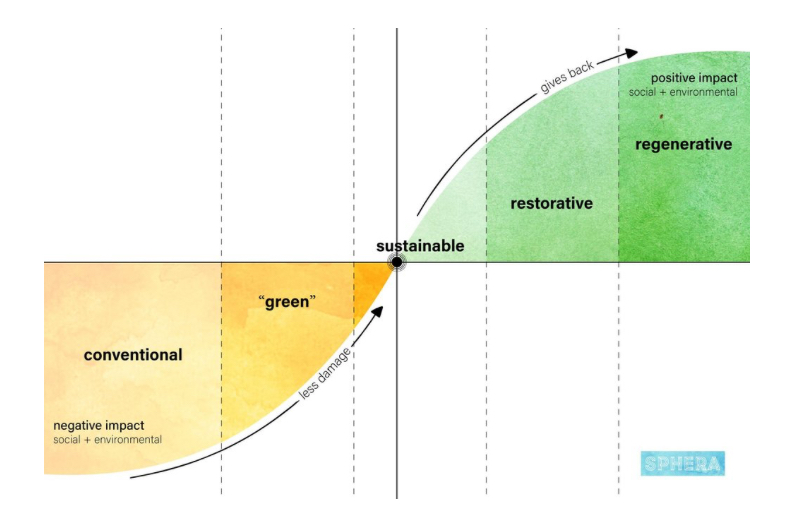

Beyond net zero … net positive and regenerative

The evolution of sustainability language — from net zero to net positive and regenerative models — signals deeper ambition.

-

Net Zero focuses on balancing emissions through reduction and removals. It is necessary but defensive.

-

Net Positive aims to create more societal and environmental value than is consumed — a shift from harm minimisation to benefit maximisation.

-

Regenerative business models aim to restore ecosystems and communities — not just sustain them.

Leading companies are experimenting with regenerative agriculture, circular product systems, community‑centric supply chains, and equity‑driven talent systems. These moves are strategic because they build resilience, social licence, and future market relevance.

Sustainability’s real story

If sustainability sometimes feels less hyped than it once did, that is because it has moved from visibility to infrastructure.The early era was about ambition and awareness. The current era demands integration, strategy, and measurable outcomes.

The companies that are thriving today — Microsoft, Unilever, Patagonia, IKEA, L’Oréal, Schneider Electric, Siemens, NextEra Energy, and others — are proving that sustainability, when embedded deeply, is not a cost centre or a marketing slogan. It is a source of resilience, competitive advantage, innovation and growth.

Sustainability is no longer optional. It is a framework for managing risk, driving opportunity, building trust, and creating long‑term value. And in a world shaped by climate extremes, resource constraints, and social uncertainty, the companies that treat sustainability as infrastructure — not ornamentation — are the ones that will thrive.

Sustainability didn’t lose its way. It found its real work.

More from the blog