Banking on the Future … DBS in Singapore, Nubank in São Paulo, Revolut in London, WeBank in Shanghai … four very different visions of the next-generation bank

September 28, 2025

The global banking industry is undergoing one of the most profound shifts in its history. After decades defined by regulation, risk management, and branch networks, a new generation of financial institutions is challenging the very foundations of how banks create value, deliver services, and build trust. These organisations—some incumbents, some digital natives—are not simply applying technology to old processes. They are reimagining the architecture, culture, and economics of banking itself.

What is striking about this new wave of innovators is not that they look alike, but that they differ so dramatically. Innovation in banking is no longer a single model; it is a portfolio of radically different strategies shaped by geography, regulation, customer needs, and technological context. The world’s most inventive banks come from Asia, Latin America, Europe, and beyond—each representing a distinct response to the same fundamental question: What is a bank in a digital, data-driven world?

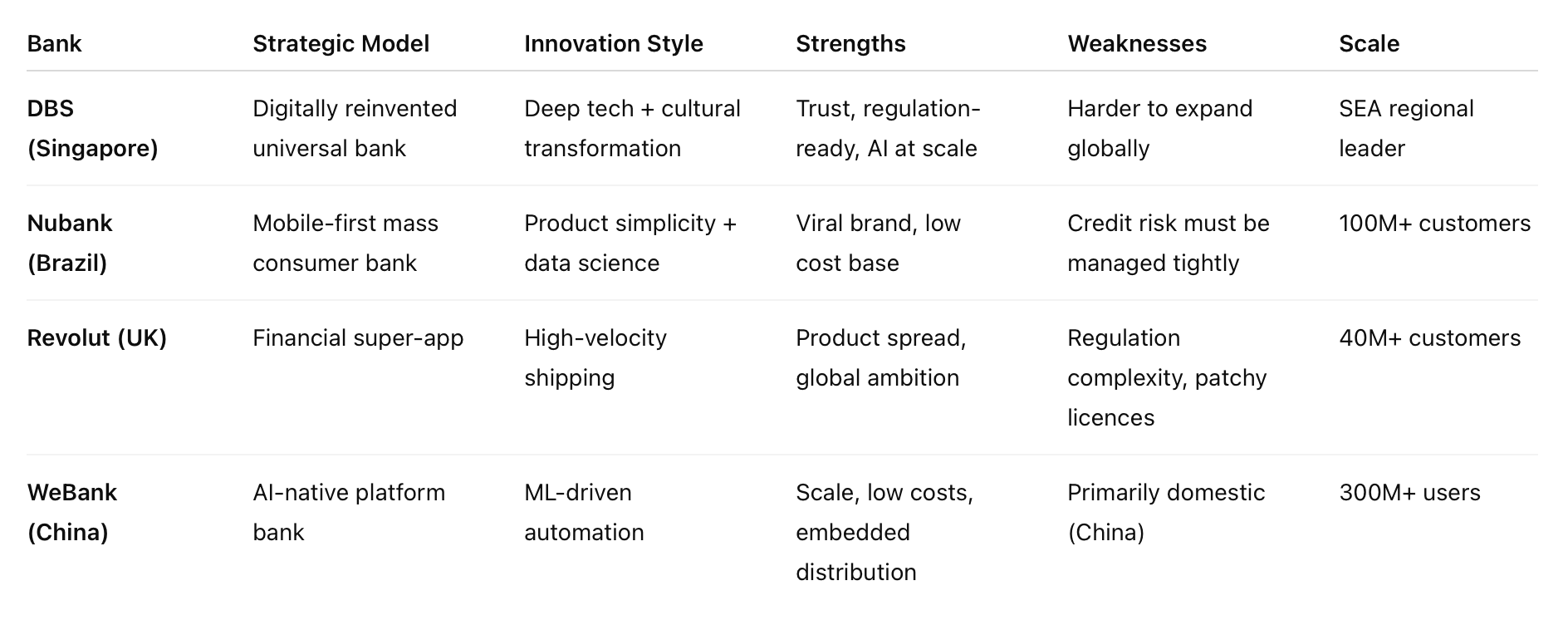

DBS in Singapore demonstrates that a traditional institution can transform itself into a digital powerhouse, combining the strengths of an incumbent with the agility of a startup. It is proof that reinvention from within is not only possible but can outperform fintech challengers. Nubank in Brazil shows the power of simplicity, technology, and emotion to attract tens of millions of customers who were previously underserved or excluded from the financial system. It is a fintech with scale and purpose, building trust in markets where banks were often viewed with frustration or suspicion.

Revolut, headquartered in London but operating almost everywhere, embodies the ambition of a financial super-app: a platform that merges banking with travel, crypto, investing, and lifestyle features. It represents the horizontal expansion model—using software velocity and global reach to make money borderless and banking more consumer-centric. And WeBank in China, part of the Tencent ecosystem, illustrates what banking looks like when built natively on artificial intelligence, cloud infrastructure, and embedded distribution. It is the closest thing the world has to fully automated, invisible banking.

Together, these four institutions offer a unique lens on the future of the industry. DBS shows how incumbents can reinvent. Nubank demonstrates the potential of low-cost digital inclusion. Revolut represents the rise of global fintech super-platforms. And WeBank is the purest example of AI-native, ecosystem-embedded banking. Each succeeds not by copying the others, but by embracing a distinctive strategy grounded in local realities and technological capability.

Their stories matter because they show how finance is shifting from a physical, product-led sector to a digital, experience-led, data-driven system. In doing so, they highlight the new sources of competitive advantage: platform economics, customer obsession, cultural adaptability, real-time data, artificial intelligence, and the ability to build trust in new ways.

These four banks, diverse in origin and design, illustrate the many futures of banking emerging around the world. And in their success, they reveal not just where finance is heading—but what every bank must learn if it is to remain relevant in the next decade.

DBS Bank … reinventing an institution in Asia

DBS is widely regarded as the world’s most successful example of a traditional bank reinvented for the digital age. Based in Singapore, DBS began its transformation in the early 2010s after recognising that customer expectations were shifting faster than the institution. Under CEO Piyush Gupta, the bank adopted a bold vision: to become “the world’s best digital bank” by redesigning culture, technology, and customer experience. This was not digital as a channel but digital as an operating model—a 27,000-person startup.

DBS invested deeply in cloud, data, and artificial intelligence, but its real breakthrough was cultural. The bank embraced agile delivery, empowered teams, and applied human-centred design to simplify services. It pioneered digital ecosystems, embedding financial services into everyday journeys—cars, homes, travel, and sustainability. The result is a bank that feels more like a modern technology company: fast, frictionless, customer-obsessed.

Today, DBS consistently ranks among the world’s most innovative banks. It has achieved industry-leading cost efficiency, improved risk performance through AI, and significantly increased digital engagement. Most importantly, its transformation demonstrates that incumbents can not only compete with but surpass fintech challengers—if they reinvent the organisation from the inside out.

Strategic Positioning

-

Traditional bank transformed into a digital-first powerhouse.

- Strategy built around “Making Banking Invisible” embedded in everyday services from partners

-

Known for “Making Banking Joyful”—frictionless CX, agile culture, GovTech-like engineering mindset.

-

Uses technology as a lever to reinvent the full bank, not just the front end.

Model

-

Full-service universal bank with digital capabilities woven throughout.

-

Emphasis on ecosystem platforms (cars, property, sustainability marketplaces).

-

Deep investments in AI, data, cloud, and 24/7 digital processes.

Innovation Strengths

-

Industry-leading transformation culture (Becoming a 27,000-person startup).

-

Strong ESG and sustainability-linked banking products.

-

Uses AI for risk, personalization, fraud, and operational efficiency.

Economics

-

High profitability, low cost-to-income ratio, strong capital base.

-

Digital customers deliver significantly higher ROE.

Why it’s important

- DBS shows how an incumbent can reinvent itself faster than fintechs.

Nubank … digital challenger conquering Latin America

Nubank is the world’s largest independent digital bank and one of the most transformative financial institutions of the decade. Founded in Brazil in 2013, Nubank emerged in a market dominated by expensive, bureaucratic incumbents, where millions of people had limited access to fair financial services. Its proposition was radical in its simplicity: a beautiful mobile experience, transparent pricing, and customer service that treated people with respect. The purple card quickly became a symbol of empowerment.

Nubank built a hyper-efficient digital model with a fraction of the cost base of traditional banks. This allowed it to offer free accounts, low fees, and accessible credit—democratising finance in a region where consumers often paid some of the world’s highest banking charges. Its viral growth was driven by trust, word-of-mouth, and the emotional connection it built with young, underserved customers.

Underpinned by advanced data science, Nubank has excelled in underwriting thin-file and first-time borrowers—turning inclusion into a profitable model. It now serves more than 100 million customers across Brazil, Mexico, and Colombia, expanding with a disciplined focus on simplicity and delight. Nubank is proof that fintech at scale can be both socially transformative and commercially successful.

Strategic Positioning

-

The world’s largest independent digital bank by customers.

-

Mission: make finance simple, fair, and accessible in an underserved region.

Model

-

Hyper-lean mobile-first bank with a simple, highly trusted brand.

-

Freemium model: free account + paid credit products + growing cross-sell.

-

Uses data science and machine learning to underwrite thin-file customers.

Innovation Strengths

-

Lightning-fast product cycles.

-

Extremely efficient customer service powered by data.

-

Viral growth: product and brand loved by younger, overlooked customers.

-

Expanding into Mexico and Colombia with similar playbook.

Economics

-

Very low-cost operations → allows free pricing and fast growth.

-

Rising profitability due to scale and credit discipline.

Why it’s important

- Nubank demonstrates fintech at massive scale—banking the unbanked with simplicity and emotion.

Revolut … global financial super-app

Revolut is the most ambitious financial super-app to emerge from Europe. Founded in London in 2015, it began as a low-cost foreign exchange card but rapidly expanded into a multi-product platform powered by relentless engineering and product velocity. Revolut aims not simply to be a bank but a global operating system for money—combining accounts, payments, travel, crypto, trading, budgeting tools, and merchant services into a single modular app.

The company’s innovation strength lies in its speed. Product teams ship new features at a pace unmatched in Western banking, enabling Revolut to enter new verticals quickly and iterate based on usage data. Its business model blends subscription tiers, interchange, trading revenue, FX, and lending—making it one of the most diversified fintechs in the world.

Revolut operates with a mix of e-money and bank licences, expanding country by country with a global mindset. It resonates especially strongly with younger, international, mobile-first customers who value control, transparency, and flexibility. Though regulatory complexity remains a challenge, Revolut’s super-app strategy positions it uniquely at the intersection of finance, technology, and lifestyle—an approach that could define a new category of global digital banking.

Strategic Positioning

-

Aims to build a global super-app for money: banking, investing, crypto, travel, commerce.

-

Growth driven by product breadth, not deep credit relationships.

Model

-

Multi-product: accounts, FX, crypto, stocks, travel, merchant features.

-

Operates with a mix of e-money licences + full bank licences in selected markets.

-

Revenue mix diversified: interchange, subscriptions, trading fees, FX/crypto, lending.

Innovation Strengths

-

Highest velocity of product releases among fintechs.

-

Ultra-strong engineering culture and global talent density.

-

UX built for speed, personal control, and financial empowerment.

Economics

-

Moving towards profitability, but with large reinvestment into expansion.

-

High product cross-sell but lower credit depth than traditional banks.

Why it’s important

- Revolut is the closest version of a Western “super-app” for money, blending finance, lifestyle, and commerce.

WeBank … the AI-native bank from China

WeBank is China’s—and arguably the world’s—most advanced AI-native bank. Launched in 2014 as China’s first digital-only institution, it is backed by Tencent and deeply integrated into the WeChat ecosystem. This gives WeBank a distribution model no traditional bank can match: embedded, invisible financial services delivered at population scale.

What distinguishes WeBank is its extreme automation. It operates with no branches, a cloud-native architecture, and end-to-end artificial intelligence across onboarding, credit scoring, fraud detection, and servicing. Its micro-loan products are approved in seconds using machine learning models trained on diverse behavioural and transactional data. WeBank is also a global leader in federated learning and privacy-preserving AI, enabling high-quality risk models without compromising user data security.

Its economics are exceptional: one of the lowest cost-to-income ratios in global banking, high profitability, and near-zero marginal cost per additional customer. By focusing on individuals and SMEs often ignored by traditional lenders, WeBank delivers inclusive finance while maintaining strong risk discipline.

WeBank represents the purest expression of the next generation of banking—instant, embedded, algorithmic, and almost entirely automated. It offers a glimpse of what the financial system could look like when AI becomes the core engine rather than a supporting tool.

Strategic Positioning

-

China’s first digital-only bank; part-owned by Tencent.

-

Focuses on AI-driven inclusive finance for consumers and SMEs.

Model

-

100% digital, no branches, fully cloud-native.

-

Uses WeChat ecosystem for distribution—embedded, invisible banking.

-

Micro-loans and SME lending driven almost entirely by ML-based risk engines.

Innovation Strengths

-

End-to-end AI automation (KYC, underwriting, servicing).

-

Near-zero marginal cost per extra customer.

-

Pioneers in federated learning, explainable AI, and privacy-preserving analytics.

-

Ultra-fast processes: loans approved in seconds.

Economics

-

Exceptionally low cost-to-income ratio (among the lowest globally).

-

High volume, low-ticket lending with disciplined risk modelling.

Why it’s important

- WeBank shows what banking looks like when built natively on AI + ecosystems, not branches.

The future of banking

Taken together, DBS, Nubank, Revolut, and WeBank offer a powerful glimpse into the multiple futures now unfolding across global finance. Their differences are as instructive as their achievements. Each has chosen a distinct strategic path—incumbent reinvention, mass-scale digital inclusion, global super-app expansion, and AI-native, ecosystem-embedded banking. Yet all four illustrate the same underlying truth: the institutions that will define the next decade are those that treat technology not as an add-on but as the organising principle of the entire business.

Their success also highlights a broader shift in the industry. Banking is no longer defined by products, branches, or balance sheets alone, but by experiences, intelligence, and participation in wider digital ecosystems. The leaders of tomorrow will be those that build trust through transparency, leverage data to deliver relevance at scale, and operate with the speed and creativity of modern software companies. They will be more open, more automated, and more integrated into daily life—often invisible, yet more impactful than ever.

These four organisations remind us that the future of banking will not be shaped by one model, but by a diversity of innovations emerging globally. They challenge every bank to reinvent itself, embrace possibility, and design a financial system fit for a digital world.

More from the blog