The Innovator’s Dilemma … Clay Christensen’s classic book is still an important lesson for every business obsessed by creating the bright new things

May 1, 2023

Tech is the shiny new thing.

In most executive teams, AI is talked about in hushed tones. We all know it matters, not entirely how. Marketers will arrive with grand plans for their brand metaverses, or super-apps, while chatbots and more apps are seen as the answer to customer service woes. Add in a few ventures, and we can change the world.

Tech is certainly a driving force of change. But beware of the shiny new thing!

Most innovation in recent years has come by thinking differently, in particular by reengineering business models in response to changing customer agendas, or new emerging segments. Think about the low-cost airlines, in many cases trumping the full service giants. Love or hate it, Ryanair is now the most valuable airline in the world.

The latest tech is exciting. But do customers really want it? Is it too soon? What’s the real problem to solve?

The Innovator’s Dilemma by the late, great, Harvard Business School professor Clayton Christensen, is one of the classic business books of our time. He wrote the bestselling text in 1997, but it it is still valuable today.

The book explains how successful companies that dominate their industries fail in the face of disruptive innovation. It’s a message of caution for leadership teams at these companies, but also a message of encouragement for competitors venturing against these goliaths.

Here’s a great 4 min video which summarises the book.

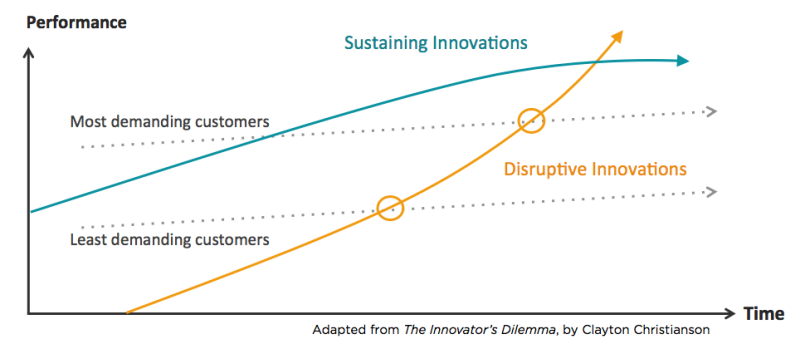

First, it distinguishes between sustaining and disruptive innovation. Then, it discusses why it’s difficult for most companies to adopt disruptive technologies. And finally, it considers what does it all mean for both large companies and startups.

In all of this, there is one important term that needs to be clarified. Christensen famously coined the word “disruption” which deserves some prior explanation due to its overuse in the media.

Here is an excerpt from the book to hopefully clear things up:

“Most new technologies foster improved product performance. I call these sustaining technologies. Some sustaining technologies can be discontinuous or radical in character, while others are of an incremental nature.

What all sustaining technologies have in common is that they improve the performance of established products, along the dimensions of performance that mainstream customers in major markets have historically valued.

Most technological advances in a given industry are sustaining in character. An important finding revealed in this book is that rarely have even the most radically difficult sustaining technologies precipitated the failure of leading firms.

Occasionally, however, disruptive technologies emerge: technologies that result in worse product performance, at least in the near-term. Ironically, in each of the instances studied in this book, it was disruptive technology that precipitated the leading firms’ failure.

Products based on disruptive technologies are typically cheaper, simpler, smaller, and, frequently, more convenient to use. There are many examples in addition to the personal desktop computer and discount retailing examples cited above. Small off-road motorcycles introduced in North America and Europe by Honda, Kawasaki, and Yamaha were disruptive technologies relative to the powerful, over-the-road cycles made by Harley-Davidson and BMW. Transistors were disruptive technologies relative to vacuum tubes. Health maintenance organizations were disruptive technologies to conventional health insurers. In the near future, “internet appliances” may become disruptive technologies to suppliers of personal computer hardware and software.”

It’s also important to understand the difference between radical sustained innovation and disruptive innovation as explained above. Often, the media will be quick to incorrectly dub a case of sustained innovation as being disruptive. The key difference is that the value network of a disruptive technology is distinct to the market offering at the time.

The innovator’s dilemma is that in every company there is a disincentive to go after new markets. Competent managers in established companies are faced with the question: “Should we make better products to make better profits or make worse profits for people that are not our customers that eat into our own margins?”. Paradoxically, this will doom companies in the long run.

Evidence shows that the longevity of companies is decreasing as the pace of technological advances increases.

Here’s Clay Christensen in 2016, (he sadly died in 2020), taking his ideas further:

More from the blog